Of the Districts reporting on hiring, most indicated a slight increase. Boston, New York, Cleveland, Richmond, St. Louis, and Minneapolis reported increased hiring in manufacturing, and contacts in Philadelphia and Kansas City anticipate future hiring in the sector. Several businesses in the Atlanta District also reported plans to increase payrolls. Philadelphia, Kansas City, and Dallas noted increased hiring among auto dealers. Contacts in Boston, Cleveland, Richmond, Chicago, Kansas City, and Dallas were having difficulties finding skilled or specialized workers in a variety of industries. In contrast, Boston manufacturing contacts reported fewer complaints about being unable to find qualified workers. Chicago noted that hiring remains selective and long-term unemployment elevated, while San Francisco noted limited demand for new workers. Staffing firms in Boston noted that the hiring cycle remains "elongated" despite stronger demand. Staffing firms in Dallas also noted high demand, while a major employment agency in New York indicated flat hiring.Let's look at some macro level data (which does not include the latest employment report):

Among Districts commenting on wages, upward pressures appeared limited. Boston noted limited pay rises in retail and manufacturing. Richmond reported some upward wage pressures in the service sector and manufacturing. Dallas and San Francisco reported minimal wage pressures, although upward pressure for certain specialized positions was reported in both Districts. Similarly, wage pressures remained largely subdued in Kansas City except for high-tech and energy positions. Wage pressures were modest or largely contained in Cleveland and Dallas, while Philadelphia noted flat wages and Minneapolis reported modest wage increases. New York noted that Wall Street compensation remains under downward pressure.

{kind=link}

Initial jobless claims have been below the 400,000 level for a few months now. Notice the overall trend; claims dropped sharply right after the official end of the recession. They leveled out at two levels -- first between 440,000 and 480,000 for the first 2/3 of 2020 and then between 400,000 and 440,000 for most of last year.

Total establishment jobs have been steadily moving upwards since about the middle of 2010. While there is still a great deal of progress to be made, things are definitely on the right track.

The unemployment rate, which at its highest point was at 10%, is still far too high, but is moving in the right direction.

Let's break the establishment picture down into goods producing, service and government jobs:

Good producing jobs have increased over the last two years, but not by much. This is part of the longer-trend issue of manufacturing becoming far more automated over the last twenty years.

{kind=link}

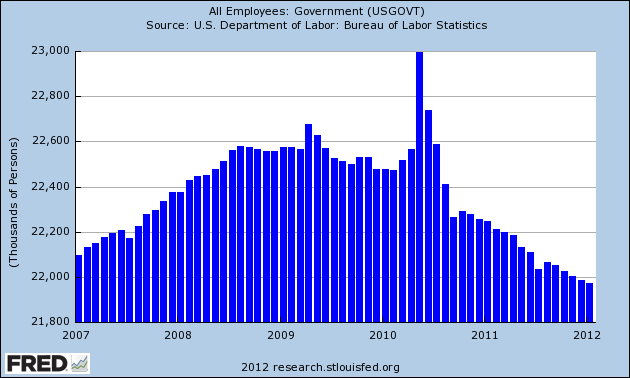

Note that government jobs continue to decline. As I've stated before, I think this is the main reason for initial claims being at high levels for an extended period of time.

Now, onto the BLS report:

Nonfarm payroll employment rose by 227,000 in February, and the unemployment rate was unchanged at 8.3 percent, the U.S. Bureau of Labor Statistics reported today. Employment rose in professional and businesses services, health care and social assistance, leisure and hospitality, manufacturing, and mining.

First, overall these are good numbers. We're over 200,000 in job growth and we're seeing broad based job growth.

The overall unemployment rate is clearly moving lower. I've blocked off the establishment job growth chart into three areas. At the end of 2010 and beginning of 2011 we see four of seven months increasing by over 200,000. Then we see the rest of last year with sub-par growth. This was caused by two events: Europe and high gas prices. Over the last three months, we're back to where we were at the end of 2010/beginning of 2011. The good news is Europe is less of an issue (at least for now). Gas remains the wild card.

Let's turn to the household survey.

The number of unemployed persons, at 12.8 million, was essentially unchanged in February. The unemployment rate held at 8.3 percent, 0.8 percentage point below the August 2011 rate. (See table A-1.)

.....

The number of long-term unemployed (those jobless for 27 weeks and over) was little changed at 5.4 million in February. These individuals accounted for 42.6 percent of the unemployed. (See table A-12.)

Both the labor force and employment rose in February. The civilian labor force participation rate, at 63.9 percent, and the employment-population ratio, at 58.6 percent, edged up over the month. (See table A-1.)

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) was essentially unchanged at 8.1 million in February. These individuals were working part time because their hours had been cut back or because they were unable to find a full-time job. (See table A-8.)

In February, 2.6 million persons were marginally attached to the labor force, essentially unchanged from a year earlier. (The data are not seasonally adjusted.) These individuals were not in the labor force, wanted and were available for work, and had looked for a job sometime in the prior 12 months. They were not counted as unemployed because they had not searched for work in the 4 weeks preceding the survey. (See table A-16.)

Overall, these are also good numbers. First, note the rate of labor under-utilization is steady. That's means that, at minimum, we're not getting any worse. The LPR increased (much to the consternation of right wing "economic" commentators) as did the number of employed. In fact, the household survey's employment numbers have been incredibly strong over the last few months. showing very strong gains.

Let's turn to the establishment survey:

Professional and business services added 82,000 jobs in February. Just over half of the increase occurred in temporary help services (+45,000). Job gains also occurred in computer systems design (+10,000) and in management and technical consulting services (+7,000). Employment in professional and business services has grown by 1.4 million since a recent low point in September 2009.

Health care and social assistance employment rose by 61,000 over the month. Within health care, ambulatory care services added 28,000 jobs, and hospital employment increased by 15,000. Over the past 12 months, health care employment has risen by 360,000. In February, social assistance employment edged up (+12,000).

In February, employment in leisure and hospitality increased by 44,000, with nearly all of the increase in food services and drinking places (+41,000). Since a recent low in February 2010, food services has added 531,000 jobs.

Manufacturing employment rose by 31,000 in February. All of the increase occurred in durable goods manufacturing, with job gains in fabricated metal products (+11,000), transportation equipment (+8,000), machinery (+5,000), and furniture and related products (+3,000). Durable goods manufacturing has added 444,000 jobs since a recent trough in January 2010.

In February, mining added 7,000 jobs, with most of the gain in support activities for mining (+5,000). Since a recent low in October 2009, mining employment has increased by 180,000.

Construction employment changed little in February, after 2 consecutive months of job gains.

Over the month, employment fell by 14,000 in nonresidential specialty trade contractors.

Overall, employment in retail trade changed little in February. A large job loss in general merchandise stores (-35,000) more than offset an increase in January (+23,000). Employment in motor vehicle and parts dealers continued to trend up in February.

Government employment was essentially unchanged in January and February. In 2011, government lost an average of 22,000 jobs per month.

Again -- we see broad based gains.

Finally, we go to wages and hours worked:

The average workweek for all employees on private nonfarm payrolls was unchanged at 34.5 hours in February. The manufacturing workweek edged up by 0.1 hour to 41.0 hours, and factory overtime was unchanged at 3.4 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls edged up by 0.1 hour to 33.8 hours. (See tables B-2 and B-7.)

In February, average hourly earnings for all employees on private nonfarm payrolls rose by 3 cents, or 0.1 percent, to $23.31. Over the past 12 months, average hourly earnings have increased by 1.9 percent. In February, average hourly earnings of private-sector production and nonsupervisory employees rose by 3 cents, or 0.2 percent, to $19.64. (See tables B-3 and B-8.)

Here, we'd like to see more improvement. However, with a high unemployment rate, we're not going to get a lot of supply side related issues on wages or hours.

Overall, 8 out of 10. Good report.

==========================

NDD here with a few additional observations:

1. Like everybody else, I'm impressed with the upward revisions to December and January. You don't get upward revisions like this in a weakening economy. I suspect today's number will be upwardly revised as well.

2. The manufacturing workweek, a leading indicator, ticked up another 0.1 to 41.0 hours. Factory workers are working more hours than at any time in more than a decade. This is a white hot number.

3. The index of aggregate hours worked increased from 95.5 to 95.7. Aggregate hours continue to outpace payroll reports, but are probably already beginning to be translated into a faster pace of increased jobs.

4. The labor participation rate increased, even with more people entering the workforce. This number is no longer bouncing along the bottom, but has significantly improved over the last half year or so.

But the most signficant overlooked number, in my opinion, is in the household report:

4. The number of jobs added per the household report was 428,000. Since this number is more volatile than the establishment survey number, it rarely gets reported. But even after accounting for the population adjustment in January, according to this survey 2,448,000 new jobs have been created in the last 8 months! That's over 300,000 a month. Since the household survey typically leads the establishment survey at inflection points, this is an extremely bullish development and argues for further upward revisions in the establishment survey. In short, the household survey number shows that we are finally really making progress on the jobs lost ruding the recession.