- by New Deal democrat

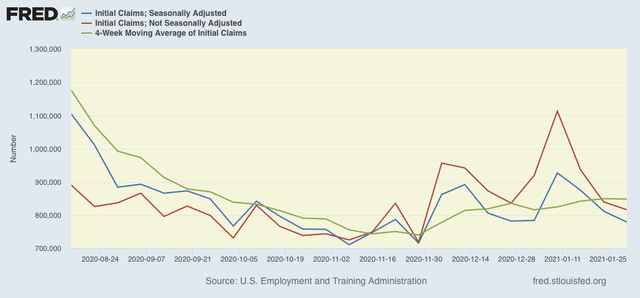

On a unadjusted basis, new jobless claims declined by 23,525 to 816,247. Seasonally adjusted claims declined by 33,000 to 779,000. The 4 week moving average also declined by 1,250 to 848,250.

Here is the close up since the end of July (these numbers were in the range of 5 to 7 million at their worst in early April):

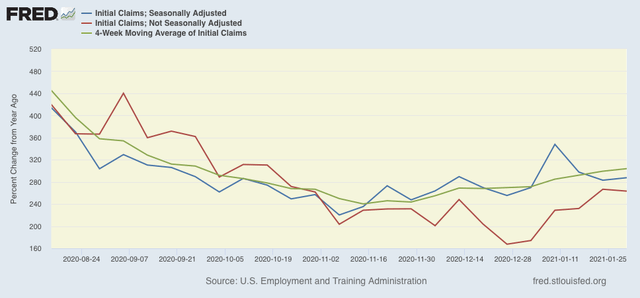

Because of the huge swings caused by the scale of the pandemic - typically claims only vary by 20,000 or less from week to week, but since the start of the pandemic, swings of 50,000 or 100,000 per week have happened as often as not, I have been posting the YoY% change in the numbers as well, since they will be much less affected by scale. As a result, there is less noise in the numbers, and the trend can be seen more clearly:

Here’s what that looks like:

The recent elevation in new claims compared with their November lows is clear. Whether the last several weeks’ declines in new claims, which were over 900,000 only 3 weeks ago, means the upward trend has peaked, will have to await several more weeks’ data.

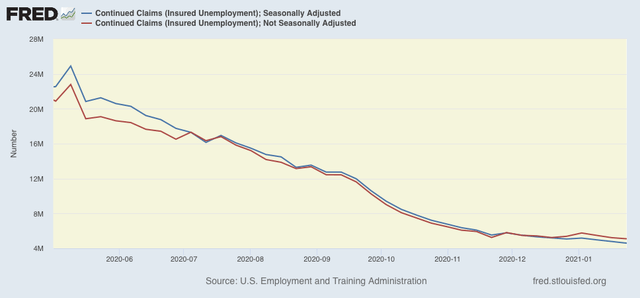

Meanwhile continuing claims, which historically lag initial claims typically by a few weeks to several months, made still more new pandemic lows this week. Seasonally adjusted continuing claims declined by 193,000 to 4,592,000, while the unadjusted number declined by 127,726 to 5,094,605:

Although I had suspected that we would see an upward reversal, obviously that hasn’t happened.

As I usually note, a reminder that both initial and continued claims remain at or above their worst levels from the Great Recession.

Finally, tomorrow we will get the January employment report. For the relevant set of weeks, January claims averaged about 20,000 higher than December. Last week, when the average was 40,000, I wrote that it appeared more likely than not that we will see another slightly negative jobs report. We still might, but with the revisions a small gain is equally possible.

Because of the much more coherent, comprehensive, and forceful approach to the pandemic from the new Biden Administration, and the simple fact that the weather will begin to warm up in a month, I am expecting the trend in claims to peak and to reverse again by the beginning of April - hopefully for good.