Saturday, May 10, 2014

Weekly Indicators for May 5-9 at XE.com

- by New Deal democrat

This was another week of nearly uniformly positive contemporaneous economic data. The "Spring spring" has continued into May.

Friday, May 9, 2014

A third long leading indicator probably turned negative in Q1 2014

- by New Deal democrat

Corporate profits deflated by unit labor costs. This post is up over at XE.com.

Thursday, May 8, 2014

In which I am a semi-wet blanket about that 401(k) story

By now you've probably all read at a bunch of blogs about how IRS data shows that Americans increased their borrowing from or cashed out their 401(k)'s in recent years, all of which feature these graphs:

A truthful headline for these graphs would be "During and right after the Great Recession, Americans increasingly tapped their 401(k)'s." While the original Bloomberg piece was fairly careful, some of the later iterations have sloppily or ambiguously used the present tense (see, e.g., Barry Ritholtz, “Tapping your 401(k)?”).

Which is simply not correct. This data is in no way contemporaneous data. The most recent reading is THREE YEARS OLD. And the most recent, three-year-old, data, shows a significant improvement from the four-year- old data.

It’s also worth pointing out that the series isn’t population adjusted, which is a non-trvial difference, and the 38% increase in the number of IRS returns incurring the penatly is faiirly consistent to the ~60% increase in the unemployment rate from 6% to 10%.

What the graphs show is that those borrowing from or cashing out their 401(k)'s went up as unemployment went up, peaked about when unemployment peaked, and came down in 2011 as unemployment started to recede. We have absolutely no idea what has happened in the last 3 years, and furthermore it is a reasonable bet that 401(k)’s were raided less and less as the unemployment rate continued to go down.

All of this seems non-contoversial to me. Which leads me to my next question: would the alarm be the same if we still had a well functioning pension system for most people? 401(k)’s are basically “rainy day” funds where the target rainy day is retirement. Obviously we should expect that people who have emergencies are going to tap their rainy day funds. Is that by itself really a problem? – Or only because 401(k)’s have largely replaced rather than supplemented traditional pensions?

In my opinion the alarm shouldn’t be that people tapped into their 401(k)’s as the unemployment situation worsened. The alarm should be that 401(k)’s are a dismal (and to some extent intentional) failure as a replacement for the traditional pension. No company should be allowed to offer a 401(k) that does not include a substantial company match, or is in lieu of or bigger than its traditional or defined contribution pension, or is not as generous percentage-wise as its stock option or other incentive program for senior executives.

That, it seems to me, is the disgrace. Not that people cashed out or borrowed from 401(k)’s more in 2008-11 than they did in 2002-06.

The Failure of Austerity: Spain

This is over at XE.com

http://community.xe.com/forum/xe-market-analysis/failure-austerity-spain

http://community.xe.com/forum/xe-market-analysis/failure-austerity-spain

Wednesday, May 7, 2014

Real median wages for occupational employment decline -0.6% in 2013*

- by New Deal democrat

Most of the measures of real wages that I have tracked bottomed either in the beginning of 2013 or in late 2012, so this one comes as a bit of nasty surprise. With an asterisk.

Every year in May, the BLS, in cooperation with state workforce bureaus, compiles a list of median wages for hundreds of occupations. In the last few years, these have shown that jobs in the 4th quintile, i.e., the lower middle class or working poor, have taken the biggest hit.

Like other measures of real wages, they reached a peak at the end of the last recession when gas prices were under $1.50 a gallon and thus mild nominal increase in wages were paired with about a -1% deflation in overall prices.

With gas prices stabilizing in the last 3 years, I certainly expected even small nominal wage increases to lead to an increase in this measure of wages as well.

Not so. As of May 2013, the median wage in the US was $16.87. In 2012 it had been $16.71, but adjusting for inflation, that becomes $16.98, which means that real wages were down -0.6%.

Now here is why there is an asterisk. The result is likely due to the way the BLS conducts the survey, as explained in this technical note: the 2013 results are due to results obtained over 6 surveys from November 2010 through May 2013. That means the survey period coincided almost perfectly with the trough in other wage measures.

If we treat the survey as an average of wages from late 2010 through early 2013, then the continued decline makes sense. Unfortunately we won't have a comparison until one year from now.

Unit labor costs up YoY, gain in first quarter

- by New Deal democrat

I have a new post up at XE.com reporting on unit labor costs, which were just reported for the first quarter.

Last year, you may remember, I teed off on reporter David Cay Johnston, who did some sloppy Doomish reporting on 1Q 2013's number.

Most measures of real median wages increased in the first quarter of this year. I'll put up a comprehensive post updating all of the data series at some point in the next week.

Tuesday, May 6, 2014

A note for Tuesday: 3 reasons I will vote democrat in 2016

- by New Deal democrat

(Slow day, have items in draft but not completed, so ...)

- Antonin Scalia (78 years old)

- Anthony Kennedy (77 years old)

- Ruth Bader Ginsburg (81 years old)

None of the above three are likely to alive or healthy enough to serve on the Supreme Court by 2020. I have previously pointed out that it typically takes 3 consecutive Presidential terms of same party control to reshape the Court.

Who do you want to name their replacements?

There is no single item, no matter how important, on any economic or social agenda, that will have nearly the impact as the answer to that one question.

Monday, May 5, 2014

Historical recoveries in manufacturing vs. retail jobs

- by New Deal democrat

This is the second installment in my look at how low vs. high paying jobs have recovered in past recessions. My hypothesis is that the typical pattern in recoveries is that low wage jobs recover faster than high wage jobs. Thus, earlier in a recovery it will be the case that the economy seems to be producing only low wage jobs. Since most post-World War 2 recoveries restored all jobs relatively quickly, the pattern was not long-lasting. This recovery, however, is from a much deeper hole and is taking much longer, so the period in which it is producing mainly low wage jobs is taking longer and has been profoundly noticed. In this installment I am comparing high-paying manufacturing jobs with low paying retail jobs.

This comparison is a special challenge, since manufacturing employment reached its peak in 1979, and has trended downward ever since. So, while I can look at recessions through 1974 as I did with construction jobs, measuring the month at which the respective category of jobs exceeded its prior peak of employment, it is impossible to do so for recessions beginning in 1979.

Since there has been an overall declining trend in manufacturing jobs since, what I can do is compare the first derivative of manufacturing job growth/decline against the first derivative of retail job growth/decline. In other words, at what point after the recession did each category have its highest rate of growth. The first derivative information is represented in italics in the chart below:

| Recession year | manufacturing | retail | lag in months |

|---|---|---|---|

| 1948 | 8/1950 | 6/1950 | 2 |

| 1953 | 3/1965 | 2/1955 | 121 |

| 1957 | 9/1964 | 1/1959 | 68 |

| 1960 | 10/1963 | 11/1961 | 23 |

| 1970 | 11/1973 | 9/1970 | 38 |

| 1974 | 5/1978 | 8/1975 | 33 |

| 1979 | 7/1981 | 7/1981 | 0 |

| 1981 | 4/1984 | 11/1984 | -7 |

| 1990 | 4/1994 | 1/1995 | -9 |

| 2001 | 10/2004 | 8/2005 | -10 |

| 2008 | 3/2011 | 12/2013 | -33 |

What we find is that, for every single job recovery since World War 2, up until 1980, retail jobs regained their prior peak before manufacturing jobs, in one case by over a decade! All but one such lag were at least by almost 2 years.

In the later recessions as to which we must measure by the first derivative of YoY growth, in all cases but one, including the current expansion, the rate of manufacturing job growth peaked in advance of that of the rate of retail job growth. As the below graph shows, in 5 of the 7 pre-1980 recessions, the YoY increase in manufacturing jobs also peaked first:

In summary, in manufacturing as with construction, this economic expansion is no different from most other post- World War 2 expansions. And in all cases where we can make a direct absolute measure, low paying retail jobs fully recovered before manufacturing jobs did so.

In summary, in manufacturing as with construction, this economic expansion is no different from most other post- World War 2 expansions. And in all cases where we can make a direct absolute measure, low paying retail jobs fully recovered before manufacturing jobs did so.

The REAL "real unemployment rate" for April 2014

- by New Deal democrat

This morning the New York Times ran an article describing how poor wage growth is the best measure of how fragile this economic expansion has been for average Americans. I agree. Unfortunately in that article, unsourced, they reported that

... [I]n Friday’s jobs report..., the unemployment rate fell entirely because people stopped looking for work, not because they found jobs.What a load of crap. The BLS itself said that the decline in labor force participation in April was mainly because fewer than normal people entered it, rather than people dropping out. But this poor reporting is typical. The EPI wrote that its "missing workers" number (based on estimates from a research paper published 7 years ago) reached a new high in April, despite the fact that the economy has added over 225,000 jobs per month for the last three months -- well above any estimate of what is needed to absorb population growth. Meanwhile the popular blog Naked Capitalism calculates a rate of 12%+ for unemployment with an analysis that begins with an unspoken "assume there was no Baby Boom" and completely ignores the inevitable downward pressure Boomer retirements must place on the labor force participation rate.

So herewith, let me update the "real real unemployment rate.

In order to be counted among the unemployed for purposes of the monthly jobs survey, a person must have actively looked for a job during the reference period. But what about people who are so discouraged that they have completely stopped looking for work and have simply dropped out of the labor force?

The monthly household jobs survey measures exactly this in a statistic called "not in labor force, want a job now." Here's what that metric shows for the last 20 years:

The number of discouraged workers rose by nearly 2,000,000 in the wake of the great recession, but has declined by about 1/3 of that number in the last two years.

In order to find out what the "real" unemployment rate is, including such discouraged workers, we simply add the number of people shown above to both the numerator (unemployed) and denominator (civilian labor force, which excludes those adults not interested in jobs, like retirees) of the statistics used for the unemployment rate. Here's what that shows:

The usually reported unemployment rate (U3, in red) is currently 6.3%. The "real" unemployment rate including those who want a job but haven't looked (blue) is 9.8%.

While this is by no means good, it is important to compare apples to apples. Note that the current rate is equivalent to that of late 1994, and even at the height of the late 1990's tech boom, the best economy the US has seen since the 1960's, this rate was 6.7%.

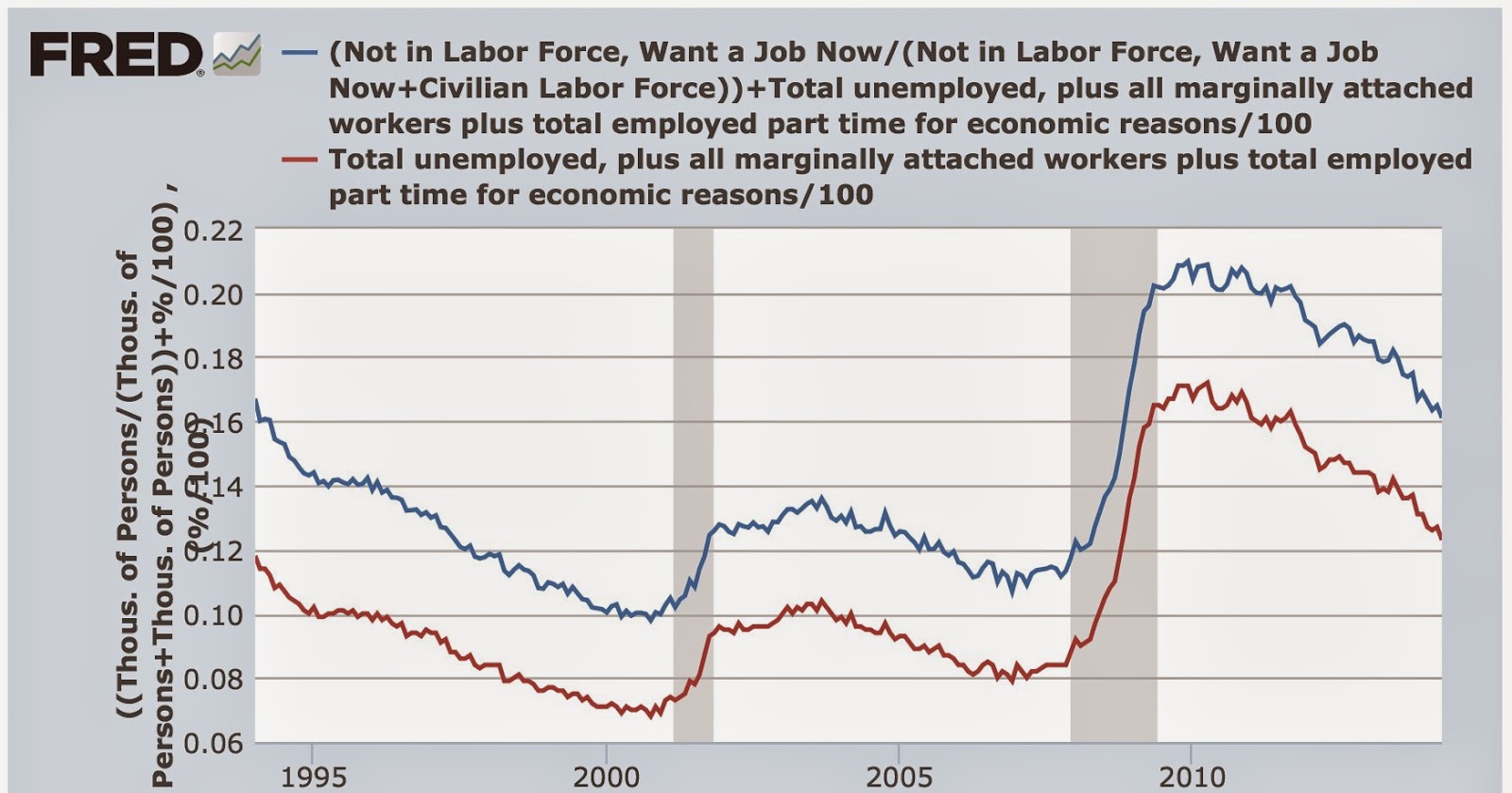

We can perform a similar calculation to get the "real underemployment rate," i.e., which adds those who are working part time for economic reasons or are otherwise marginally attached to the workforce:

The "real" underemployment rate is 16.1% (blue) vs. 12.3% (red). Again, note that even in the 1990's tech boom, this rate never got below 9.9%.

The calculation above is in accord with recent papers by the Atlanta Fed , researchers at the IMF, and Shigeru Fujita of the Philadelphia Fed that, while most of the increase in the "missing workers" initially was due to discouragement, in the several years there has been a relative increase in the number of retiring Boomers, thus reducing the number of those who are "not in the labor force, [but] want a job now."

Sunday, May 4, 2014

John Hinderaker: Still Economically Clueless

To quote Hawkeye Pierce from MASH, "there's so little that Hinderaker knows about economics, it's difficult to keep up with what he doesn't know." Really, it's amazing to me that a person who supposedly has an impressive resume can be so wrong on economics on such a regular basis.

In his latest attempt to prove economic relevance, Hinderaker compares the current expansion to the Reagan's expansion. As usual, he fails. Completely.

As people who regularly read this blog know, there is a big fundamental difference that makes this comparison moot. Reagan's recession was caused by the Federal Reserve increasing interest rates to slow inflation. As a result, we see the following chart of the effective federal funds rate:

And, we have the following chart of the discount rate:

Because the Fed was the primary cause of the slowdown (fulfilling its job of "taking away the punch bowl") the recovery that started afterward could gain traction quickly.

In contrast, the latest expansion is a "credit default recovery," a vastly different economic event. Here, the economy experiences a massive asset bubble caused by the expansion of credit. But as the asset bubble bursts, those who are in debt begin selling assets to cover their loans. Eventually, the pace of selling leads to two things: a collapsing bubble and a large number of people who owe more than they own. This means thy greatly slowdown the pace of their purchases, slowing overall economic activity. We know this to be the current case from looking at monetary velocity numbers:

You can read about this concept in Irving Fisher's essay, The Debt Deflation Theory of Great Depressions.

At this point, I don't expect Hinderaker to actually say anything insightful about economics; he's been consistently wrong on the topic for the better part of 10 years. But, people actually read his work and (terrifyingly enough) take him seriously. And that is dangerous, especially when his analysis is so fundamentally flawed.

In his latest attempt to prove economic relevance, Hinderaker compares the current expansion to the Reagan's expansion. As usual, he fails. Completely.

As people who regularly read this blog know, there is a big fundamental difference that makes this comparison moot. Reagan's recession was caused by the Federal Reserve increasing interest rates to slow inflation. As a result, we see the following chart of the effective federal funds rate:

And, we have the following chart of the discount rate:

Because the Fed was the primary cause of the slowdown (fulfilling its job of "taking away the punch bowl") the recovery that started afterward could gain traction quickly.

In contrast, the latest expansion is a "credit default recovery," a vastly different economic event. Here, the economy experiences a massive asset bubble caused by the expansion of credit. But as the asset bubble bursts, those who are in debt begin selling assets to cover their loans. Eventually, the pace of selling leads to two things: a collapsing bubble and a large number of people who owe more than they own. This means thy greatly slowdown the pace of their purchases, slowing overall economic activity. We know this to be the current case from looking at monetary velocity numbers:

You can read about this concept in Irving Fisher's essay, The Debt Deflation Theory of Great Depressions.

At this point, I don't expect Hinderaker to actually say anything insightful about economics; he's been consistently wrong on the topic for the better part of 10 years. But, people actually read his work and (terrifyingly enough) take him seriously. And that is dangerous, especially when his analysis is so fundamentally flawed.

Subscribe to:

Posts (Atom)