- by New Deal democrat

No important economic news today. Yesterday existing home sales were released, but their economic impact isn’t all that important, except as it can confirm what has been happening with new houses under construction. And confirmation is what it gave us.

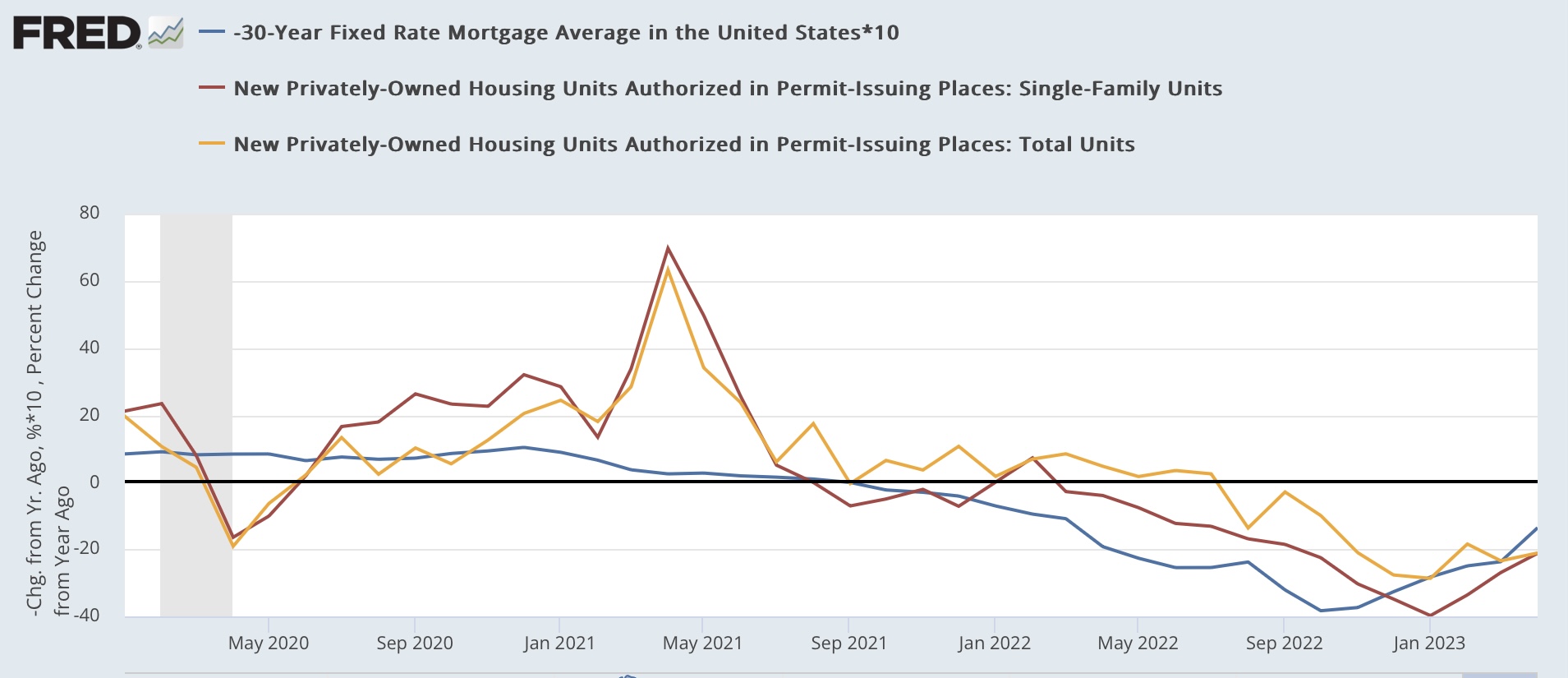

First, *sales* of houses have bottomed, following the peak in mortgage rates over 7% at the end of last October.

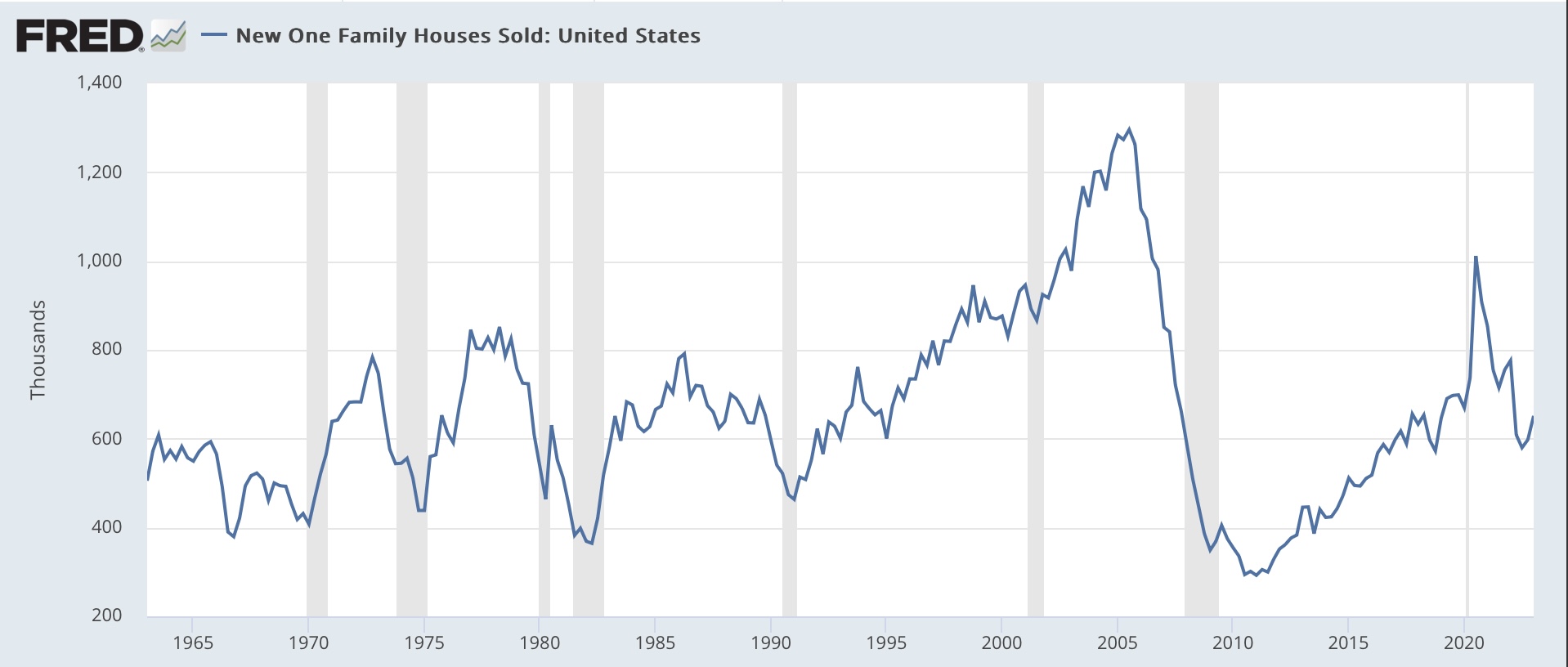

New home sales (which will be released for April on Monday) as is often the case, were the first to turn, having bottomed last July:

Existing home sales yesterday remained above their January bottom by a substantial margin:

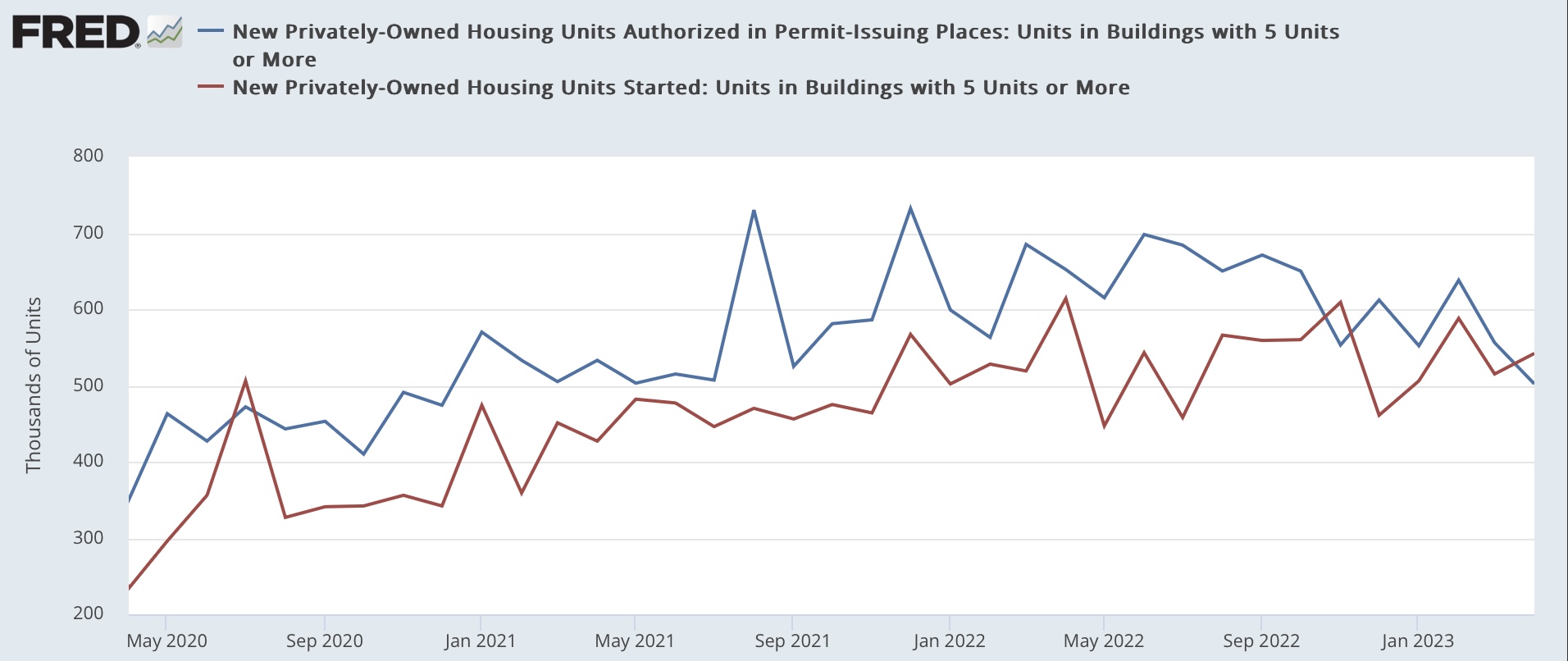

With one exception, housing permits and starts, as reported earlier this week, also bottomed in January:

As shown above, the big bounce came in single family units. While starts in multi-family units have continued to slowly increase, permits for multi-family units made a new low:

This suggests that multi-family units under construction have a ways to go before they turn down. As indicated the other day, total units under construction have turned down, but not by much:

Turning to prices, we mainly have to measure YoY, since little of the data is seasonally adjusted.

Yesterday prices for existing homes were reported to have declined by -1.7%. The past two months have been the first YoY declines since the end of the housing bust over 10 years ago:

YoY median prices for new homes rose to +3.2%, after a single month of YoY decline in January. The below graph is averaged quarterly to cut down on noise:

Here the number is +1.4%.

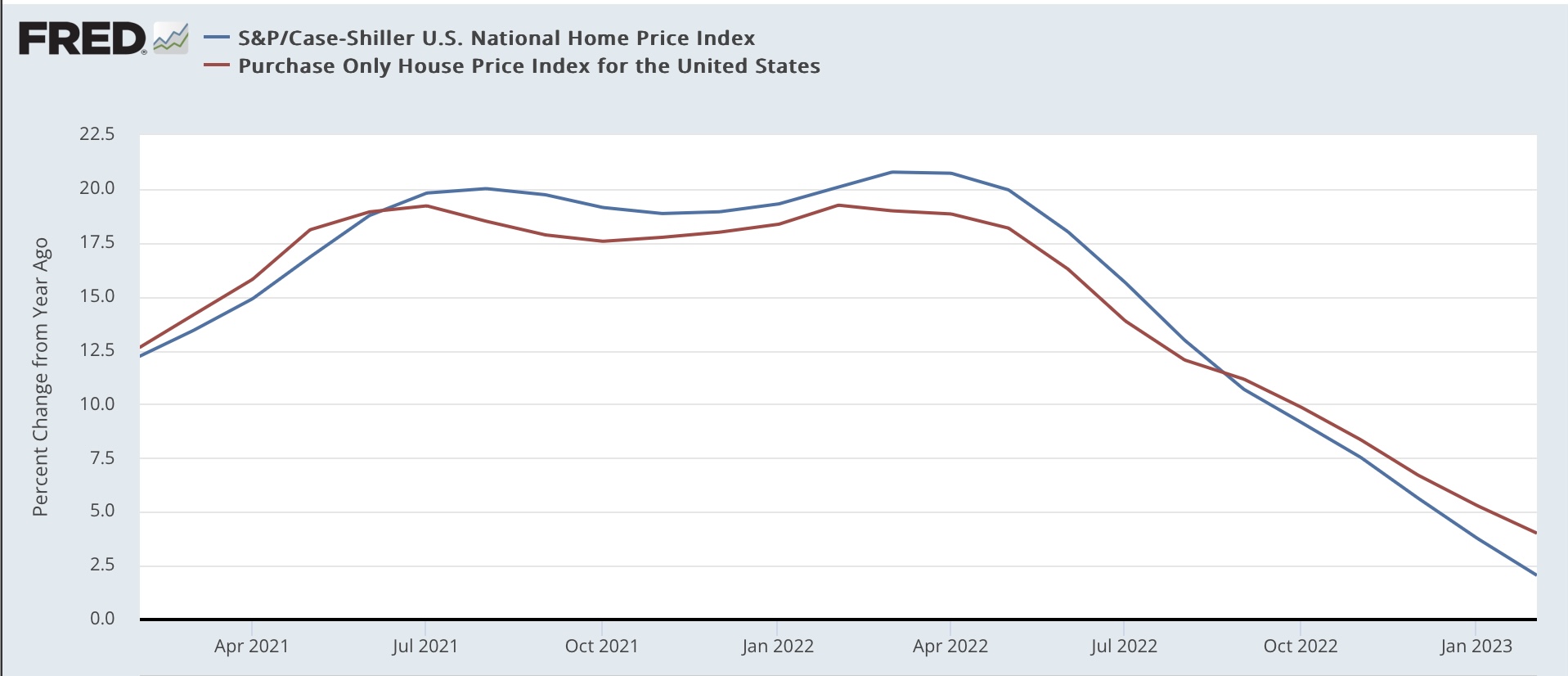

The FHFA and Case-Shiller repeat sales indexes have only been updated through February, and show sharp YoY deceleration, but still increases of 4.0% and 2.0%, respectively:

These two repeat sales indexes are seasonally adjusted, and show very minor declines of less than 1% and less than 3% respectively:

In absolute terms, prices may have bottomed as well.

The repeat sales indexes will be updated for March on May 30.