Mr$. Bonddad and I were out of town last week, so we had friends watch the house. We left a 12-pack for our nephew, which Sarge knocked off the kitchen island. However -- he sacrificed his paw for the beer. Anything for the beer. He's fine now.

The unemployment rate edged up to 9.8 percent in November, and nonfarm payroll employment was little changed (+39,000), the U.S. Bureau of Labor Statistics reported today. Temporary help services and health care continued to add jobs over the month, while employment fell in retail trade. Employment in most major industries changed little in November.

Reports from the twelve Federal Reserve Districts indicate that the economy continued to improve, on balance, during the reporting period from early/mid-October to mid-November. Economic activity in the Boston, Cleveland, Atlanta, Dallas, and San Francisco Districts increased at a slight to modest pace, while a somewhat stronger pace of economic activity was seen in New York, Richmond, Chicago, Minneapolis, and Kansas City. Philadelphia and St. Louis reported business conditions as mixed.Manufacturing activity continued to expand in almost all Districts, with relatively strong growth seen in metal fabrication and the automotive industries. Reports also showed steady to increasing activity for professional and nonfinancial services. Two Districts noted a decline in demand from government agencies due to budgetary shortfalls. Reports on consumer spending tended to be positive. Nonetheless, several Districts noted that households remain price sensitive and focused on buying necessities. Expectations for the holiday shopping season were generally positive, with several Districts expecting higher sales when compared to year-ago levels. Sales of new cars and light trucks were largely higher than in our last report. Tourism improved in all reporting Districts.

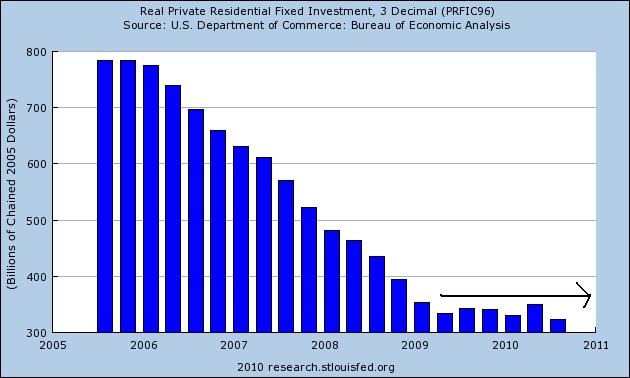

Housing markets remain depressed, with several Districts reporting further weakening during the past six weeks. Conditions in commercial real estate were mixed, and activity stayed at low levels. Agricultural conditions were generally favorable, with several Districts reporting yields nearing historic highs. Agricultural sales to off-shore buyers increased. Overall activity in the energy sector continued to expand.

Lending activity remained stable across most Districts. Credit quality has been steady to improving for most of the Districts that commented on it. Prices for final goods and services were fairly stable, despite rising input costs, especially for agricultural commodities, metals, and fuel. Hiring activity showed some improvement across most Districts. Wage pressures were contained.

... (you probably will start noticing it in the MSM soon, if not this morning), it appears that over the past 18 hours our country's largest bank, Bank of America, may have entered into the final stage(s) of a fairly swift implosion. Obviously, the economic, political and social implications of an event of this nature and magnitude occurring right now--if it does continue along its apparent trajectory even for a few more days--are nothing less than horrific.(my emphasis)

....

Yesterday, MSM and blog stories started surfacing concerning two separate issues ... with either one providing more than sufficient cause to drive the two-trillion-dollar behemoth into receivership, or worse--that place where almost all divine oligarchic institutions have gone of late: taxpayer exponential bailout hell.

DJIA is up 249.76 points today and I've yet to hear anything on this from CNBC. If BoA's in trouble and it hits the MSM, it'll hit the markets hard, unless BoA has one of those special lending facilities sweetheart lines of credit available from Treasury, the Fed and/or the FDIC.

So far, all I'm hearing is market rally cheerleading on CNBC.

BTW, Bob Pisani reports that the market buzz is that all the Bush tax cuts will be extended. So, it looks like the US Chamber of Commerce Brotherhood of Thieves and Pickpockets think they're going to get what they paid for from the GOP and corpradems.

BAC shares went up 0.34 today as well, as did all 30 Dow companies.

You guys should take advantage by shorting BoA stock. It's not just rich fat cats that are "investors", normal people are as well, and you can be too. And if you guys are so sure that BoA is going to tank, you'd be a bunch of saps not to take advantage.

To me, this diary smells like wishful thinking in the guise of objective analysis, but for those of you taking this diary as objective truth, you can make a huge killing.

upcoming six-figure job losses certain to occur throughout the auto industrydue to the presumed liquidation and disappearance of both General Motors and Chrysler.

As Mr. Obama made his comments at the announcement of the pay freeze, the bipartisan commission he established in February to propose ways to reduce the growth of the national debt entered a final two days of negotiations over combinations of spending cuts and revenue increases. In a sign of the struggle to find a compromise that could attract Democratic and Republicans votes, the commission chairmen — Alan K. Simpson, a former Senate Republican leader, and Erskine B. Bowles, a chief of staff to President Bill Clinton — decided to meet privately with members one at a time on Monday and Tuesday instead of convening all 18 members.The Republicans on the panel are generally opposed to raising taxes and the Democrats to big changes in Medicare, Medicaid and Social Security.

The above emboldened words illustrate the stupidity of Washington. Simply put there is no way to balance the budget without two things happening: taxes going up and some kind of compromise on health care spending. There is just no way for meaningful change to happen without both parties compromising on their key issues. So, expect the problem to continue.

November and December are the crucial months for state sales tax collections, which make up a third of state revenues.Although the Rockefeller Institute has yet to report on third quarter state tax revenues (not just sales tax, but personal and corporate income taxes, and other miscellaneous taxes), the following report by Stateline (a nonprofit, nonpartisan online news site funded by the Pew Foundation that reports on state issues) suggests that the improvement in state tax revenues won't be able to make up for continuing shortfalls even next summer:

[S]tate officials are reporting steady although modest gains in monthly tax collections, a sign that the nascent economic recovery is gaining strength after three years of plunging sales tax revenues that decimated state budgets.In other words, if Stateline's report is correct, it appears that the combination of the total expiration of federal government assistance (a given at this point), mounting costs, and the ending of one-off tax gimmicks mean that the states (and in particular California) are likely to need to make further cuts next summer, a very depressing prospect, even if the level of those cuts are nowhere near what has been necessary in the last year.

In recent days, officials in 27 states have said that year-over-year monthly revenues are increasing and some are forecasting a rise in tax receipts in state budgets for the fiscal year that begins July 1.... Improved sales tax receipts are leading the revenue recovery in most states.... Corporate tax revenue also is up in many states, consistent with the rise in business profits nationally. ...

Still, there is a flip side to [states'] recovering revenue picture that puts the situation in all states in perspective. [States] may appear to have ... extra cash next year, but most of that will be needed to make up for the loss of federal stimulus money and mounting Medicaid and public pension costs....

Most states do not have surplus revenues, which means they will have to cut spending, raise taxes, borrow or tap reserves to balance their budgets for the fiscal year that begins July 1. NCSL is projecting that states will have a total of $72 billion in budget gaps in 2012.... Many states with revenue increases still are confronting huge budget shortfalls that guarantee years of fiscal turmoil. [For example,] California may have escalating sales tax receipts, but its budget shortfall will exceed $25 billion for the fiscal year starting July 1....

Tax collections increased by 3.9 percent in the third quarter of 2010, compared to the same period a year earlier, based on data from 48 states. Of states reporting, 42 showed gains in overall tax revenues. Collections improved for the two largest revenue sources — personal income and sales taxes — while corporate income tax revenues declined slightly.

The growth in overall collections is partly driven by new tax laws in several states, but is also due to a slowly recovering economy, according to report authors Lucy Dadayan and Donald Boyd. Yet they cautioned that difficult times for states’ fiscal conditions have not ended.

“The state tax revenue picture in the first three quarters of calendar year 2010 represented significant improvement from the collapse of the preceding quarters,” they write. “Still, the immediate outlook is for revenue collections significantly below prerecession levels, and growing spending pressures. The overall picture remains: States will face continued, significant budget challenges in fiscal 2011 and beyond.”

"The manufacturing sector grew during October, with both new orders and production making significant gains. Since hitting a peak in April, the trend for manufacturing has been toward slower growth. However, this month's report signals a continuation of the recovery that began 15 months ago, and its strength raises expectations for growth in the balance of the quarter. Survey respondents note the recovery in autos, computers and exports as key drivers of this growth. Concerns about inventory growth are lessened by the improvement in new orders during October. With 14 of 18 industries reporting growth in October, manufacturing continues to outperform the other sectors of the economy."The durable goods new orders numbers have been near stagnant for the last 4-6 months:

The Empire State Manufacturing Survey indicates that conditions deteriorated in November for New York State manufacturers. For the first time since mid-2009, the general business conditions index fell below zero, declining 27 points to -11.1. The new orders index plummeted 37 points to -24.4, and the shipments index also fell below zero. The indexes for both prices paid and prices received declined, with the latter falling into negative territory. The index for number of employees remained above zero but was well below its October level, and the average workweek index dropped to -13.0. Future indexes generally climbed, suggesting that conditions were expected to improve in the months ahead, although the capital spending and technology spending indexes inched lower.However, this report was balanced out by the Philly Fed's numbers:

The survey's broadest measure of manufacturing conditions, the diffusion index of current activity, increased from a reading of 1.0 in October to 22.5 in November (see Chart). This is the highest reading in the index since last December. Indexes for new orders and shipments also improved this month, and each index increased 15 points. Indexes for both delivery times and un-filled orders changed from negative to positive this month, suggesting improvement.

In November, the seasonally adjusted composite index of manufacturing activity — our broadest measure of manufacturing — rose four points to 9 from October's reading of 5. Among the index's components, shipments rose four points to 7, new orders edged up two points to finish at 10, and the jobs index increased six points to 10.Other indicators also suggested generally stronger activity. The index for capacity utilization moved up three points to 9, while the backlogs of orders contracted at a much slower pace, gaining nine points to −3. The delivery times index added one point to end at 6, and our gauges for inventories were somewhat higher in November. The finished goods inventory index increased ten points to 16, and the raw materials inventory index advanced five points to finish at 15.

Overall, the Eastern seaboard looks to be in fair shape. This is important, as this geographical area was a problem area in the latest Beige Book. While this region is not out of the woods, it is in a clearly better position than a few months ago.

The Chicago Fed was up slightly in its latest report, but has been printing a horizontal number for the last few months:

Here is the relevant information from the latest report:

The Kansas City Manufacturing index has printed three strong months:

The net percentage of firms reporting month-over-month increases in production in November was 21, up from 10 in October and 14 in September (Tables 1 & 2, Chart). The increase in production occurred among both durable and nondurable goods producing plants, with a sharp rise in machinery, high-tech, printing, and transportation equipment activity partly due to higher export orders. All other month-over-month indicators also improved from the previous month. The shipments, new orders, and order backlog indexes climbed higher, and the employment index reached its highest level since late 2007. The new orders for exports index rose from 0 to 11, and both inventory indexes moved into positive territory.

Texas factory activity increased in October, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, was positive for the second consecutive month and slightly higher than its September reading.

Despite the rise in output, several other manufacturing activity indicators fell again. The new orders and shipments indexes were negative for the fifth consecutive month. The capacity utilization index dipped below zero, with more than one-quarter of respondents reporting a decrease.

Measures of general business conditions improved markedly in October, suggesting the broader economy strengthened. After four months in negative territory, the general business activity index rose sharply from –18 in September to 3 this month. The company outlook index also jumped up, rising from –4 to 13. The advance in the index was largely due to a sharp decline in the share of manufacturers reporting a worsened outlook, falling from 25 percent to 13 percent.

The above numbers show a sector that is slowing as demonstrated by the moderating pace of industrial production growth over the last new months. In addition, capacity utilization is still low and several regional federal reserve manufacturing numbers (New York, Richmond and Texas) show clear signs of slowing. While the durable goods numbers have been near stagnant for the last 4-6 months, this is typical of this particular data series. On the positive side, the ISM number's latest number showed a strong pick-up in the latest report, the overall number has been positive for over a year and the Philly and Kansas City Fed showed strong improvement. In addition, the Chicago Fed manufacturing index is still printing a positive number, although at a moderating pace.

{kind=link}