Saturday, May 21, 2016

Weekly Indicators for May 16 - 20 at XE.com

- by New Deal democrat

My Weekly Indicator post is up at XE.com.

Probably largely due to renewed hawkish comments fro the Fed, the ghosts of 2015 have made a new apparition.

Friday, May 20, 2016

Bonddad Friday Linkfest: Energy Inflation and the Fed's Dove-Hawk Scale

The Consumer Price Index for energy declined 8.9 percent over the year ended in April, driven by a 13.8-percent decrease in gasoline prices. Prices for natural gas (-6.5 percent) and electricity (-2.1 percent) also contributed to the decline. Prices for other motor fuels, fuel oil, and propane, kerosene, and firewood were also down for the year, but together only make up 3.2 percent of the broader energy index.

Thursday, May 19, 2016

Kroger, On A Hiring Binge, Is A Buy

This idea involves risk. Talk to your financial adviser before doing anything. Also, I could be wrong about this.

The current rally – which started in 1Q09 -- is getting a bit long in the tooth. Not only is technical analysis arguing against purchasing equities, so is the current earnings environment, where overall corporate profits have declined in 4 of the last 5 quarters. Finally, recent economic numbers, such as last months’ below estimate 160,000 job gains or the weak 1Q GDP print – add to the concern. While recession calls are premature, the macro-environment is weak.

At minimum, stock analysts should look for companies in economic sectors with steady growth profiles such as the food and beverage sectors:

In the last 20 years, there are only two periods of contraction, each lasting less than a year. These sales are the backbone of the consumer staples sector, represented by the XLP ETF. Below are three charts that show this ETF’s technical picture:

Although both the daily chart (top chart) and weekly chart (middle chart) recently printed negative candles, they remain in uptrends. The ETF’s advance/decline line (bottom chart) is rising.

The Kroger Company is the largest grocery store by market capitalization; it is slightly over 3 times the size of its nearest competitor Whole Foods. Kroger’s growth is consistent: their 5-year average revenue growth rate is 6%-7%, while the 10-year average is a solid 6%. Due to razor thin net margins that average between 1%-1.5%, the company needs to aggressively manage its operations. Thankfully, their cash conversion cycle dropped from 10.75 days in 2010 to 7.28 in 2015, their inventory turnover ratio has been a consistent 14-15 for the last 4 years and the days of inventory on hand has been a steady 24.2-25.2 since 2012. These numbers show a strong organization-wide discipline, which the company’s thin margins and hyper-competitive sector require.

A stock trading near a 52-week low needs a buying catalyst. Thankfully, the company just provided one:

Supermarket chain Kroger is going on a huge hiring spree. Its family of stores is slated to hire people for 14,000 full-time positions, the company announced Tuesday.

Kroger said it will hold interviews across the U.S. on May 14 to fill the positions. Interested candidates can apply online and then show up at a location on Saturday for the interview.

“We have openings across the country for friendly, hard-working associates to join our team,” Tim Massa, Kroger’s group vice president of human resources and labor relations, said in a statement.

“We are looking for people who are passionate about making a difference for customers and communities—and want to do it in a fun, team environment with great benefits and advancement

opportunities.”

Next to COGS, labor is the company’s biggest expense. The only reason they would increase their workforce at this pace is if they already had the sales reported or strongly believed they were coming. This is especially true in an environment where a larger number of states and municipalities are increasing the minimum wage. There’s no other explanation for a hiring wave of this magnitude.

Let’s face it: groceries stores lack the sizzle of the next “big thing.” They are boring, stodgy businesses that perform a basic function for their communities. But Kroger is a dependable performer that has an impressive control over their operations. Their current price level is attractive and their recent hiring announcement indicates sales growth is probably on the way.

Why hasn't increased household formation led to increased housing construction?

- by New Deal democrat

Tim Taylor has an interesting article about "What was different about housing this time?" Specifically, why has housing in both building terms and as a share of GDP risen so slowly since 2009.

To cut to the chase, he writes that while prices have been increasing:

There are two possible categories of reasons for the very low level of residential building since 2009. On the supply side, it may not seem profitable to build, given what was already built back before 2008 and the lower prices. On the demand side, ... the demand for housing is tied up with the rate of "household formation"--that is, the number of people who are starting new households..... The level of household formation was low for years after 2009 ........

Together, the declines in household formation and homeownership contributed to the decline in residential expenditures as a share of GDP.

As an initial matter, I again note that it is important not to overlook the surge in all-cash purchases of large houses by foreigners - who are hedging their bets and/or shielding financial assets - since 2009.

But what caught my eye was Taylor's graph showing household formation:

It certainly *was* low after 2009 - until 2015, when it rose sharply, to an annualized rate of 1.750 million.

And now look at housing starts for the last 10 years:

Household formation and housing starts tracked reasonably closely from 2009 through 2014, but the relationship completely broke down in 2015, with about 600,000 more households formed than new houses being built.

It strikes me that this may be an important part of the spike in median asking rents since the beginning of 2015:

To say that it is puzzling that home builders have not addressed this surge in demand for starter housing is an understatement. It is probably one of the two biggest imbalances in the entire economy (along with stagnant wages vs. record profits). This isn't just an academic concern: increasing rents may have been vacuuming up nearly all of consumer gas savings for 1/3 of the populatioin. and their impact on inflation may be leading the Fed to an important policy mistake which could bring on the next recession.

Bonddad Thursday Linkfest; Low Productivity, No Recession (yet);

On Thursday, May 26, we'll be hosting our regular monthly wrap-up of economic and market events. You can sign up at this link.

So why aren’t we seeing another productivity boom? The difference between now and the last tech boom is that, in the mid-1990s, businesses throughout the economy used those new technologies to change how and what they produced. They became much more efficient and spread their reach. In the more recent tech boom, a lot of the innovation and new products are directed at our leisure time, which may enrich our lives, but doesn’t have the same groundbreaking effect on how businesses operate.

US economic growth remains sluggish, hinting at the possibility that a new recession may be near. But the numbers don’t align with a pessimistic intuition. The probability is extremely low that April marked the start of an NBER-defined downturn, based on published reports to date. Projecting a broad set of indicators into the near-term future suggests that the US will continue to sidestep a macro slump. Yes, the outlook could deteriorate if the incoming numbers stumble. But for the moment, recession risk remains low.

In fact, the prospects look encouraging for a modest rebound in economic activity in the second quarter, based on the Atlanta Fed’s latest nowcast. Although yesterday’s GDPNow estimate ticked down to a projected 2.5% increase for Q2 (as of May 17), that’s still a solid bounce higher from Q1’s tepid 0.5% advance. Forecasts aren’t written in stone, but the current forecast offers support for expecting some degree of improvement in output after a disappointing Q1.

Foreign risks

Inflation

Employment

Brexit

Market Expectations

Wednesday, May 18, 2016

Aside from a shortage in starter housing for Millennials,there is NOinflation

Yesterday's CPI report seems to be read as potentially justifying an interest rate increase in June. For example, here's Professor Tim Duy, on Fed hawks:

Inflation rose on the back of higher gas prices. Headline CPI gained 0.4 percent, although core rose a more modest 0.2 percent. Core CPI inflation is hovering just above 2 per cent....Fed hawks will be nervous that rising gas prices will quickly filter through to core inflation; doves will remind them that the Fed's target is PCE inflation, which remains well below 2 percent.

As to his own opinion, he says:

I don't think June is a go; the data isn't quite there yet.

And here is Yian Mui of the Washington Post:

The solid [consumer inflation] data helps bolster the case for the Federal Reserve to raise binterest rates at its next meeting in June.....Fed officials have long said that they expect inflation to pick up once the effects of the stronger dollar and low oil prices dissipate. Although the central bank relies on separate data to calculate price increases, Wednesday’s report on consumer costs appears to support the central bank’s claim.

Whether or not the Fed is listening, the fact is that yesterday's inflation data does no such thing.

Consumer prices less shelter are only up +0.1%. Not month owner month, but Year over Year! This is one of the lowest rates in the entire 75 year history of the series:

Here's a close-up of the last two years just to drive home the point:

If housing really were "hot," if people were buying houses with reckless abandon no matter what the price increase (like 12 years ago), yes there would be a basis for raising rates. But that is not what is happening at all.

Despite the fact that there are now or will shortly be more Millennials age 18-35 than Boomers:

The entry level housing that they need (red in the graph below) is not being built enough:

This is confirmed by the relative lack of housing inventory on the market:

and the near record low vacancy rates for apartments:

and the soaring rents:

Since rental prices are up sharply due to low vacancies and a dearth of new entry level construction, there is simply no excuse for the Fed to raise rates. In fact, raising rates will only make the multi-unit housing shortage - and the spike in rents - more acute, as the below graph of YoY changes in the Fed funds rate (blue, inverted so that an increase shows as a downward move) compared with the YoY% changes in housing starts (red) shows:

Quiite simply, an increase in interest rates has historically led to a decrease in housing construction:

Except for the housing supply shortage, there IS NO INFLATION. One of the two most likely causes for the next recession will be if the Fed perversely raises interest rates despite these facts.

Update: Here is one important reason for outsized median home price appreciation, and why builders find it more lucrative to focus on the high end market. Chinese all-cash buyers:

Chinese nationals have become the largest foreign buyers of US property after pouring billions into the market in search of safe offshore assets, according to a study.A huge surge in Chinese buying of both residential and commercial real estate last year took their five-year investment total to more than $110bn, according to the study from the Asia Society and Rosen Consulting Group.

Bonddad Wednesday Linkfest: Minimum Wage Edition

On Thursday, May 26, we'll be hosting our regular monthly wrap-up of economic and market events. You can sign up at this link.

When the burger chain reported an increase in comparable sales for the third straight quarter late last month, CEO Steve Easterbrook said that the positive growth was in part linked to better employee benefits and higher wages.

Easterbrook said lower employee turnover and higher customer satisfaction were linked to employee compensation package improvements.

"The improvements we made to our compensation and benefits package to employees in U.S.-company operated restaurants, along with expanding [the tuition assistance program] Archways to Opportunity ... have resulted in lower crew turnover and higher customer satisfaction scores," Easterbrook said in a call to Wall Street analysts, Fortune Reported.

It is here in which the empirical research has been largely consistent, as summarized by economists Dale Belman and Paul Wolfson in a recent prize-winning summary of the reams of analysis of minimum wage increases:

[Moderate] increases in the minimum wage raise the hourly wage and earnings of workers in the lower part of the wage distribution and have very modest or no effects on employment, hours, and other labor market outcomes. The minimum wage can then, as originally intended, be used to improve the conditions of those working in the least remunerative sectors of the labor market. While not a full solution to the issues of low-wage work, it is a useful instrument of policy that has low social costs and clear benefits.

Here’s how Alan Krueger, an economist whose path-breaking work on minimum wages has deeply influenced economists and policy makers, put it in a recent piece:

When I started studying the minimum wage 25 years ago, like most economists at that time I expected that the wage floor reduced employment for some groups of workers. But research that I and others have conducted convinced me that if the minimum wage is set at a moderate level it does not necessarily reduce employment. While some employers cut jobs in response to a minimum-wage increase, others find that a higher wage floor enables them to fill their vacancies and reduce turnover, which raises employment, even though it eats into their profits. The net effect of all this, as has been found in most studies of the minimum wage over the last quarter-century, is that when it is set at a moderate level, the minimum wage has little or no effect on employment.

Alan goes on to point out that “…a $15-an-hour national minimum wage would put us in uncharted waters, and risk undesirable and unintended consequences.”

Wendy’s (WEN) said that self-service ordering kiosks will be made available across its 6,000-plus restaurants in the second half of the year as minimum wage hikes and a tight labor market push up wages.

It will be up to franchisees whether to deploy the labor-saving technology, but Wendy’s President Todd Penegor did note that some franchise locations have been raising prices to offset wage hikes.

McDonald’s (MCD) has been testing self-service kiosks. But Wendy’s, which has been vocal about embracing labor-saving technology, is launching the biggest potential expansion.

Wendy’s Penegor said company-operated stores, only about 10% of the total, are seeing wage inflation of 5% to 6%, driven both by the minimum wage and some by the need to offer a competitive wage “to access good labor.”

Tuesday, May 17, 2016

Good news and bad news in this morning's data

- by New Deal democrat

We got two pieces of good news and two pieces of bad news this morning.

Let's start with the good news: Industrial production jumped +0.7% - only the 4th monthly increase in 18 months (blue in the graph below). While mining continued to decline, manufacturing (red) increased to tie its January record:

Again, adding to the evidence that the shallow industrial recession is bottoming out.

The second piece of good news is that real retail sales, and real retail sales per capita set new records:

Since this is a leading indicator, it eases the concern that a recession might happen this year.

Now the bad news. Consumer inflation ran "hot" in April, with owner's equivalent rent continuing to be the most important driver, although energy prices and medical device prices were an important assist:

Along the same lines, while housing permits and starts increased, they are still below last spring's post-recession highs, even excluding the northeast region (blue below) that includes the NYC distort ions from last spring:

While single family house permits came in only 2,000 below their December post-recession high, multi-unit housing continued to tank. Also, the February new high in single family permits was revised away:

There is a crying need for starter homes, but why should builders build them when there is so much more money in all-cash sales of high-end houses to well-off Chinese buyers?

So, two takeaways from this morning's data:

1. Immediate recession risk is receding.

2. There is absolutely zero reason for the Fed to raise rates in the inflation number, unless punishing prospective young American homebuyers is their objective.

Bonddad Tuesday Linkfest: Industrial Production Needs to Improve, Corporate Profits Lead, Goldman Ups Oil Price Target

On Thursday, May 26, we'll be hosting our regular monthly wrap-up of economic and market events. You can sign up at this link.

Industrial Production Needs to Improve (Price Headley SA)

Industrial Production Needs to Improve (Price Headley SA)

Also this week we'll get last month's industrial productivity and capacity utilization numbers. We desperately need a reversal of the strengthening downtrends from both. The market can shrug off a bit of downside volatility, but this deterioration has reached problematic levels.

Industrial Production Market Sectors

The chart below shows measures of corporate health such as operating surplus, income, profits, and cash flow usually start falling 1 or 2 years before a stock market decline or the start of a recession. According to FactSet, the 1st quarter of 2016 was the fourth quarter of negative profit growth. This article evaluates profits as a leading indicator of the stock market and economy.

Goldman Ups Its Oil Price Target (FT)

Goldman Sachs is getting bullish on oil – sort of.

A supply deficit – driven by disruptions in Nigeria and robust demand – has led the US investment bank to upgrade its short-term outlook for oil, write Mehreen Khan and Neil Hume.

Goldman now expects WTI to average $45 a barrel in the second quarter of 2016, from an earlier March estimate of $35.

Oil Prices Daily

Energy Commodities

XLEs Daily

XLEs/SPYs

Monday, May 16, 2016

Five graphs for 2016: May update

- by New Deal democrat

At the beginning of this year, I identified graphs of 5 aspects of the economy that most bore watching. Now that we have the data for the first 1/3 of the year, let's take a look at each of them.

#5 The Yield Curve

The Fed having embarked on a tightening regimen as of December, the question is, will the yield curve compress or, worse, invert, an inversion being a nearly infallible sign of a recession to come in about 12 months.

Here's what has happened so far:

Rates on 2 year treasuries rose in advance of the Fed's move in November, but have since fallen to their pre-December range, while the 10 year treasury yield has continued to decline at a slow rate (typically long rates only start to fall once the tightening cycle has caused the economy to weaken). At 0.99% as of last Friday, however, the yield curve is still quite positive when seen in a historical perspective.

Rates on 2 year treasuries rose in advance of the Fed's move in November, but have since fallen to their pre-December range, while the 10 year treasury yield has continued to decline at a slow rate (typically long rates only start to fall once the tightening cycle has caused the economy to weaken). At 0.99% as of last Friday, however, the yield curve is still quite positive when seen in a historical perspective.

Weakness in the economy has put the Fed back on hold, but if the trend in rates were continue, then even as few as two more .25% rate hikes by the Fed could cause the yield curve to invert.

#4 The trade weighted US$

#4 The trade weighted US$

Perhaps the biggest story of 2015 was the damage done by the 15%+ surge in the US$ that began in late 2014 -- which not only harmed exports, but pretty much cancelled out the positive effect on consumers' wallets by lower gas prices.

Here there has been a big change:

Against all currencies, the US$ has recently ben in the range of +3% to +5% YoY - a more typical range. Against major currencies, the US$ has actually declined YoY. This is good news.

Against all currencies, the US$ has recently ben in the range of +3% to +5% YoY - a more typical range. Against major currencies, the US$ has actually declined YoY. This is good news.

#3 The inventory to sales ratio

An elevated ratio of business inventories to sales means that businesses are overstocked. This has frequently but not always been associated with a recession. I have been using the wholesalers invenotry to sales ratio, since it has fewer secular issues. Here the news has not good this year, as the raito increased in January, although it fell ever so slightly in February and March:

This is probably the single worst statistic in the economy right now.

This is probably the single worst statistic in the economy right now.

#2 Discouraged workers

While 2015 saw a big improvement in involuntary part time employment, the number of those so discouraged that they did not even look for work, even though they want a job, went stubbornly sideways until the last quarter of 2015. Although it has not borken through its December low, and is still above its rate in the later part of the 1990s through 2007, in the first 4 months of this year, the trend has clearly been down:

This looks like improvement, but we are still at least 500,000 above a "good" number.

This looks like improvement, but we are still at least 500,000 above a "good" number.

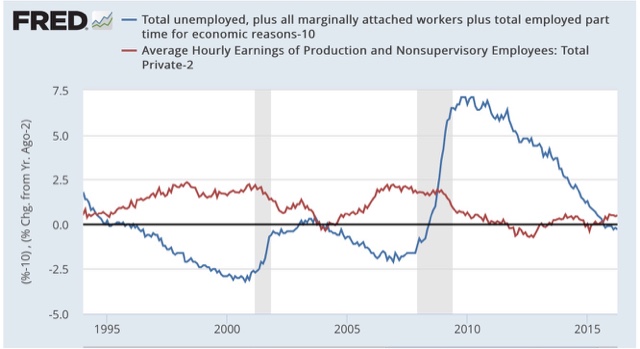

#1 Underemployment and wages

The single worst part of this economic expansion has been its pathetic record for wage increases. Nominal YoY wage increases for nonsupervisory workers were generally about 4% in the 1990s, and even in the latter part of the early 2000s expansion. In this expansion, however, nominal increases have averaged a pitiful 2%, meaning that even a mild uptick in inflation is enough to cause a real decrease in middle and working class purchasing power.

There is increasing consensus that the primary reason for this miserable situation has been the persistent huge percentage of those who are either unemployed or underemployed, such as involuntary part time workers.

The single worst part of this economic expansion has been its pathetic record for wage increases. Nominal YoY wage increases for nonsupervisory workers were generally about 4% in the 1990s, and even in the latter part of the early 2000s expansion. In this expansion, however, nominal increases have averaged a pitiful 2%, meaning that even a mild uptick in inflation is enough to cause a real decrease in middle and working class purchasing power.

There is increasing consensus that the primary reason for this miserable situation has been the persistent huge percentage of those who are either unemployed or underemployed, such as involuntary part time workers.

This expanded "U6" unemployment rate ( minus 10%) is shown in blue in the graph below, toether with YoY nominal wage growth (minus 2%)!:

In the 1990s and 2000s, once the U6 underemployment rate fell under 10%, nominal wage growth started to accelerate. U6 is now 9.7%, and there has been some mild improvement off the bottom. More than anything, the US needs real wage growth for labor, and the present nominal reading of 2.5% still isn't nearly good enough. With the expansion in deceleration mode past mid-cycle, it is not clear at all how much further improvement we are going to get before the next recession hits.

In the 1990s and 2000s, once the U6 underemployment rate fell under 10%, nominal wage growth started to accelerate. U6 is now 9.7%, and there has been some mild improvement off the bottom. More than anything, the US needs real wage growth for labor, and the present nominal reading of 2.5% still isn't nearly good enough. With the expansion in deceleration mode past mid-cycle, it is not clear at all how much further improvement we are going to get before the next recession hits.

Bonddad Monday Linkfest; Americans Miss Unions, Renewable Energy Investments and Secular Stagnation

On Thursday, May 26, we'll be hosting our regular monthly wrap-up of economic and market events. You can sign up at this link.

Americans Miss Unions, Not Manufacturing Jobs (538)

Americans Miss Unions, Not Manufacturing Jobs (538)

On average, manufacturing jobs still pay better than most jobs available to people without a college degree. The median manufacturing worker without a bachelor’s degree earned $15 an hour in 2015, a dollar more than similarly educated workers in other industries.1 But those averages obscure a great deal of variation beneath the surface. Average manufacturing wages are inflated by high-earning veterans; newly created jobs tend to pay less. And there are substantial regional variations. The average manufacturing production worker in Michigan earns $20.80 an hour, vs.$18.86 in South Carolina, according to data from the Bureau of Labor Statistics.

Why do factory workers make more in Michigan? In a word: unions. The Midwest was, at least until recently, a bastion of union strength. Southern states, by contrast, are mostly “right-to-work” states where unions never gained a strong foothold. Private-sector unions have been shrinking across the country for decades, but they are stronger in the Midwest than in most other parts of the country. In Michigan, 23 percent of manufacturing production workers were union members in 2015; in South Carolina, less than 2 percent were.2

Total Manufacturing Jobs Since the 1940s

Y/Y Percentage Change in Average Hourly Earings of Manufacturing Employees Since the 1940s

Chart Showing Productivity Growth and Wage Growth Since 1980

Exxon Mobil Corp. is partnering with a company to capture carbon-dioxide emissions from power plants. Total SA, the French oil supermajor, announced a $1.1 billion deal Monday to buy the battery maker Saft Groupe SA, complementing its 2011 purchase of a majority stake in the solar-panel maker SunPower Corp. And the Canadian pipeline company Enbridge Inc. announced Tuesday it will pay $218 million for stakes in offshore wind farms as it attempts to double its low-carbon generating capacity.

While fossil fuel companies have been dabbling in clean energy for years, they typically stayed close to their roots by focusing on ethanol and other biofuels. This round of investments takes them into the heart of the clean-energy industry. As crude prices struggle to recover and growth projections for renewables soar, oil companies see a chance to diversify.

“The supermajors recognize there is going to be tremendous growth in low-carbon sources of energy,” said Jason Bordoff, director of the Center on Global Energy Policy at Columbia University. “To thrive in the long term, they need a mix in their portfolio.”

Solar ETF Daily Chart

Alternate Energy ETF Daily Chart

Energy Sector ETF

Energy Sector/SPY

Summers’s deeper argument is that world growth is stuck in a rut because there’s a chronic shortage of demand for goods and services and a concomitant excess of desired savings. The U.S. and other industrialized nations tend to save more as their populations age, he says. Meanwhile, growing inequality puts a bigger share of the world’s income in the pockets of rich people; they can’t spend everything they make, so they save it. The investment that would ordinarily soak up those savings is falling short. That’s partly because the new economy is asset-lite: Companies such as Uber and Airbnb prosper by exploiting assets (cars and houses) that already exist. Software, which is pure information and doesn’t require the construction of factories, accounts for a bigger share of the economy. Slow growth in output and productivity reduces investment as executives lose faith in the payoff from capital spending.

Exhibit No. 1 in Summers’s case: Interest rates have been trending down for 30 years, even after taking into account the decline in inflation. The interest rate, like any price, reflects supply and demand. It’s fallen because the demand for loans is weak and the supply of loans from savers, who have extra cash to deploy, is strong. It used to be thought that interest rates couldn’t go below zero, but the Bank of Japan and the European Central Bank, among others, are so desperate to kindle growth that they’ve pushed some rates below what used to be called the “zero lower bound” into negative territory.

Subscribe to:

Posts (Atom)