NDD has had a brutal week at work and simply ran out of time this week. As his attorney or record, I've counseled him to consumer a large quantity of adult beverages in quick succession.

Weekly indicators will return next week.

Saturday, January 14, 2012

Friday, January 13, 2012

Stephen Colbert: The Presidential Candidate of the Bonddad Blog

If ever anyone -- and I mean anyone -- could make me have hope in the current electoral situation, it is Jon Stewart and Stephen Colbert. Unfortunately, Jon is not running. However, Stephen is at least forming an exploratory committee. There, I, Bonddad of the Bonddad Blog, do hereby formally announce my endorsement of Stephen Colbert for President of the United States of South Carolina.

Seriously -- if anyone can demonstrate how completely screwed up our current political fundraising system is, it's Colbert and Stewart. And the clips below are gold -- they're funny, but they're not, but they are, but they're not. These guys make the 24 hour news cycle bearable. The clips below explain why.

Seriously -- if anyone can demonstrate how completely screwed up our current political fundraising system is, it's Colbert and Stewart. And the clips below are gold -- they're funny, but they're not, but they are, but they're not. These guys make the 24 hour news cycle bearable. The clips below explain why.

The Colbert Report

Get More: Colbert Report Full Episodes,Political Humor & Satire Blog,Video Archive

Get More: Colbert Report Full Episodes,Political Humor & Satire Blog,Video Archive

The Colbert Report

Get More: Colbert Report Full Episodes,Political Humor & Satire Blog,Video Archive

Get More: Colbert Report Full Episodes,Political Humor & Satire Blog,Video Archive

1952 PCE's

The above chart shows the percentage contribution that personal consumption expenditures (PCEs) made to GDP in 1952, along with the contribution of the subparts of the PCE statistic. The second and fourth quarter were the big months for PCEs, with the second quarter's growth being drive by non-durable goods while the fourth quarter's growth was driven by durable goods purchases. The first quarters contributions were incredibly weak, with an actual contraction in non-durables being the reason for the contraction. Also note the drop in durable purchases in the third quarter.

The reason for the large drop in durable goods purchases in the third quarter was a large steel strike, which shutdown auto manufacturing. With the strike ended in the fourth quarter, auto production ramped back up, leading to higher production and, therefore, more durable goods.

Regarding the expansion and increased use of consumer debt, consider the following from the 1953 economic report to the president:

{kind=link}

1952: A Look At GDP and Its Subparts

This post is part of the Bonddad Economic History Project.

Above is a graph of the percentage change in GDP and the contributions of various subparts. The data tells us the following:

1.) There were two quarters of very good growth -- the first and fourth quarter. The second quarter the economy was very close to 0% while the second quarter's growth was fair.

2.) PCEs provided a lot of firepower in the second and fourth quarter, while they added some in the third.

3.) Gross private investment was very strong in the third and fourth quarter. It was a primary reason for the drag on growth in the second quarter.

4.) Net exports subtracted from growth in each quarter of the year.

5.) Government spending (from the Korean War) was the primary driver of growth in the first and second quarter. It contributed in the third and added remarkably little in the fourth.

Above is a graph of the percentage change in GDP and the contributions of various subparts. The data tells us the following:

1.) There were two quarters of very good growth -- the first and fourth quarter. The second quarter the economy was very close to 0% while the second quarter's growth was fair.

2.) PCEs provided a lot of firepower in the second and fourth quarter, while they added some in the third.

3.) Gross private investment was very strong in the third and fourth quarter. It was a primary reason for the drag on growth in the second quarter.

4.) Net exports subtracted from growth in each quarter of the year.

5.) Government spending (from the Korean War) was the primary driver of growth in the first and second quarter. It contributed in the third and added remarkably little in the fourth.

Morning Market

Remember that I'm looking for the following events to "like" the market rally: an increase in copper, better intra-day stats in the equity markets, a continued rally in the dollar and a sell-off in the treasury market.

Yesterday, copper popped higher on very high volume. While it printed a small bar, which I really don't like, the upward gap is impressive. Plus, the gap has come at a technically important time.

The dollar is right at important technical levels -- highs from early October. The EMAs are still strong, but the A/D and CMF are weakening, which is concerning.

The dollar has been moving sideways for the last six days, using the late and mid-December high points as technical support. We need to see the dollar move through the 23 price level.

The treasury market is consolidating and not selling off -- at least not yet.

The above two charts of the IWMs and SPYs illustrate my continued concerns with the equity markets. The IWMs stayed in a tight range for about a week and a half before drifting higher over the last three sessions. The SPYs have traded in two tight ranges for the last week and a half, but there hasn't been a lot of strong intra-day action.

The QQQs are the best looking average, with a clear uptrend, but also have the same issue -- trading in ranges, popping a bit, and then trading sideways. The fact that only one average has a good chart is also concerning.

Yesterday, copper popped higher on very high volume. While it printed a small bar, which I really don't like, the upward gap is impressive. Plus, the gap has come at a technically important time.

The dollar is right at important technical levels -- highs from early October. The EMAs are still strong, but the A/D and CMF are weakening, which is concerning.

The dollar has been moving sideways for the last six days, using the late and mid-December high points as technical support. We need to see the dollar move through the 23 price level.

The treasury market is consolidating and not selling off -- at least not yet.

The above two charts of the IWMs and SPYs illustrate my continued concerns with the equity markets. The IWMs stayed in a tight range for about a week and a half before drifting higher over the last three sessions. The SPYs have traded in two tight ranges for the last week and a half, but there hasn't been a lot of strong intra-day action.

The QQQs are the best looking average, with a clear uptrend, but also have the same issue -- trading in ranges, popping a bit, and then trading sideways. The fact that only one average has a good chart is also concerning.

Thursday, January 12, 2012

Bonddad Linkfest

- UK industrial production sags (FT)

- ECB keeps rates at 1% (FT)

- China's inflation drops to 4.1% YOY (FT)

- Spain and Italy and successful bond auctions (FT)

- German inflation cools (BB)

- Indian industrial production increases more than forecast (BB)

- The Beige Book

- Census retail sales report

- DOL's initial unemployment report

- Reducing the US' petroleum consumption from transportation

Will Food Prices Reassert Themselves?

Three stories over the past week caught my eye:

First, we have a dry spell in South America:

While food prices only comprise 14.79% of CPI calculations transportation prices only comprise 17.3%. Yet, large oil spikes (and subsequent gas spikes) can have a disproportionate effect on consumer sentiment and spending. And while the chart above does not conclusively state that high YOY percentage changes always proceed a recession, it does say that high high prices can be a precursor to recession. So, it behooves us to keep an eye on this situation.

I always look at the grains charts as a proxy for food prices, largely because corn, wheat and soybeans are the foundations of the US food system. To that end, consider these charts of grains:

The weekly grains chart sold off at the end of last summer and drifted lower through mid-December. Prices rallied strongly at the end of last year and in the first week of January. While the EMA picture is still bearish, prices have rallied into the 20 week EMA. The MACD has given a buy signal as sell, although the A/D and CMF volume indicators are weak.

The daily chart shows that grains have rallied strongly over the last few weeks. Prices have advanced through the 10, 20 and 50 day EMA. These EMAs are also rising, with the 10 now moving through the 50. The MACD is rising and has now turned positive. However, the A/D line is not that exciting, although the CMF shows some positive movement.

In short, food prices may be a problem to keep an eye on this year.

First, we have a dry spell in South America:

Crop prices rose sharply this week on worries that unusually dry weather in South America could cut global supplies. Temperatures rose last week in South America and rains that fell over the weekend were lighter than had been expected. The dryness could leave corn plants there stunted because they are pollinating this time of year.Second, we have a lack of corn seed supply in the US midwest:

According to the Associated Press, traders are worried that lower exports from Brazil and Argentina could reduce world food supplies. Strong demand from livestock producers and ethanol makers has already drawn down global reserves of corn and soybeans.

Crop prices had been falling this winter on expectations that exports from the United Sates could help supply the global market. A hot summer didn't damage the U.S. corn crop as severely as some traders had expected. But gains from the U.S. Farm Belt could be offset by losses in South America if dry weather there leads to lower crop yields.

January soybeans rose 37 cents Tuesday to $12.095 per bushel. March wheat rose 22.75 cents to finish at $6.4475 per bushel. March corn rose 13.75 cents to $6.3325 per bushel

As farmers across the U.S. prepare to plant this year's corn crop, they are running up against an unexpected obstacle: a lack of seed.Third, we have this:

By some estimates, U.S. production of corn seed was down 25% to 50% ahead of this planting season. Output of corn seed, which is grown from specialized plants, was sliced by drought conditions across the Midwest and the Great Plains last year

The shortage of seed threatens to scuttle what some expect to be the biggest planting of corn in the U.S., the world's largest producer, since World War II. Early forecasts have been calling for up to 95 million acres to be sown with corn this spring, a 3.4% increase from 2011.

The problem could mean the second year in a row of tumult for the corn market. Last year, hot weather led to a smaller U.S. crop than traders had expected, fueling a historic rally in corn prices to a record $8 a bushel in late spring.

Hedge funds raised their wagers on higher commodity prices by the most since July 2010 after signs of accelerating U.S. growth bolstered optimism that demand for raw materials will strengthen.That got me thinking about this graph, which shows the YOY percentage change in the food price component of CPI:

Money managers expanded their combined net-long positions across 18 U.S. futures and options by 25 percent to 671,915 contracts (.MMLOSH) in the week ended Jan. 3, Commodity Futures Trading Commission data show. Bullish bets on cotton rose the most since April 2009 and those on coffee doubled. Crude-oil holdings reached a three-week high.

Prices for metals and bulk commodities such as coal rose at least 85 percent of the time since 2004 when global industrial production strengthened, Macquarie Group Ltd. estimates. U.S. unemployment fell to the lowest in almost three years, and it joined China, Australia, Germany, India and the U.K. in reporting manufacturing gains. Almost $253 billion was added to the value of global equities last week on speculation economies will skirt a slump as Europe’s debt crisis deepens.

“You’ve been seeing a risk-on trade across the board, not just in commodities,” said John Bailey, the founder and chief executive officer of Stamford, Connecticut-based Spruce Private Investors LLC, which advises investors holding about $3 billion of assets. “Between a calming in Europe and better-than- expected numbers in the U.S., including employment and housing, that has led to a risk-on attitude among managers.”

While food prices only comprise 14.79% of CPI calculations transportation prices only comprise 17.3%. Yet, large oil spikes (and subsequent gas spikes) can have a disproportionate effect on consumer sentiment and spending. And while the chart above does not conclusively state that high YOY percentage changes always proceed a recession, it does say that high high prices can be a precursor to recession. So, it behooves us to keep an eye on this situation.

I always look at the grains charts as a proxy for food prices, largely because corn, wheat and soybeans are the foundations of the US food system. To that end, consider these charts of grains:

The daily chart shows that grains have rallied strongly over the last few weeks. Prices have advanced through the 10, 20 and 50 day EMA. These EMAs are also rising, with the 10 now moving through the 50. The MACD is rising and has now turned positive. However, the A/D line is not that exciting, although the CMF shows some positive movement.

{kind=link}

In short, food prices may be a problem to keep an eye on this year.

Beta testing the Shadow Weekly Leading Index

- by New Deal democrat

As readers know, I am trying to reverse engineer the ECRI Weekly Leading Index. Prof. Geoffrey Moore recommended 11 elements for this index when he proposed it in 1990. As originally conceived, the weekly index was supposed to anticipate the monthly LEI, which had to rely on late reports like housing permits and durable goods orders. By contrast, the 4 monthly numbers incorporated into the weekly index would all be known within one week of the end of the previous month. The weekly index would be slightly less reliable than the LEI, but by dint of early report, would be very useful.

Ten of the 11 elements are publicly reported (the 11th is Dun and Bradstreet's weekly number of business formations and dissolutions which is not available to the public). Of the remaining 10, six are weekly series and the other 4 are the monthly series noted above. I have already created several preliminary graphs based on only 7 elements which look very close to ECRI's Weekly Index, including its roller coaster ride of the last two years. So it's time to beta-test and make refinements based on the results.

The list below is the changes in those 10 numbers for the last week. The only change I have made is the substitution of credit spreads for real M2, which I have reason to believe was replaced on the list. Another issue is whether ECRI continues to include the early monthly reports, or changed Moore's original concept by only relying on weekly reports. The last issue is whether the report is an unweighted average of the elements or not. I am giving two forecasts for the WLI, one that includes and one that does not include the early monthly reports. The forecast assumes an unweighted index.

The following weekly components changed as follows for the week ending January 6 (YoY change in parenthesis):

DJ Bond Avg -.07 to 114.58, or -0.1% (YoY up from 111.12, or +3.1%)

S&P 500 +20.21 to 1277.81, or +1.6% (YoY up from 1271.50, or +0.5%)

Initial Jobless claims*: +27,000 to 399,000 or -6.8% w/w (YoY -15,000 from 414,000, or +4.8%)

Commodity price changes: +2.47 to 119.81, so +2.1% (YoY -17.05 from 133.65, or -10.4%)

Purchase Mortgage applications: +8.1% w/w (YoY -17.9%)

10 year treasury - BAA credit spread*: +.02 to 3.29%, or -0.6% (YoY up from 2.69%, or -18.2%)

If only weekly series are used, the predicted week over week change is +0.7, and the YoY growth rate is -6.4.

The following early monthly reports changed as follows (YoY change in parenthesis):

Avg manufacturing workweek +.1 to 41.5, or +0.2% (+.2 YoY, or +0.5%)

Unemployment 0-5 weeks*:+159 to 2669, or -6.0% (YoY -32, or +1.2%)

ISM vendor performance flat at 49.9, or 0.0 (YoY -6.8, or -12%)

ISM inventory change -1.2 to 47.1, or -2.5% (YoY -4.7 or -9.1%)

If the early monthly reports are included, the unweighted predicted weekly change is -0.4 and the YoY growth rate is -5.8.

[*Note: these are inverse relationships, so the higher the number, the lower the growth score]

We'll have an answer tomorrow. I anticipate refining the forecast as I am able to determine better how ECRI constructs their Index.

As readers know, I am trying to reverse engineer the ECRI Weekly Leading Index. Prof. Geoffrey Moore recommended 11 elements for this index when he proposed it in 1990. As originally conceived, the weekly index was supposed to anticipate the monthly LEI, which had to rely on late reports like housing permits and durable goods orders. By contrast, the 4 monthly numbers incorporated into the weekly index would all be known within one week of the end of the previous month. The weekly index would be slightly less reliable than the LEI, but by dint of early report, would be very useful.

Ten of the 11 elements are publicly reported (the 11th is Dun and Bradstreet's weekly number of business formations and dissolutions which is not available to the public). Of the remaining 10, six are weekly series and the other 4 are the monthly series noted above. I have already created several preliminary graphs based on only 7 elements which look very close to ECRI's Weekly Index, including its roller coaster ride of the last two years. So it's time to beta-test and make refinements based on the results.

The list below is the changes in those 10 numbers for the last week. The only change I have made is the substitution of credit spreads for real M2, which I have reason to believe was replaced on the list. Another issue is whether ECRI continues to include the early monthly reports, or changed Moore's original concept by only relying on weekly reports. The last issue is whether the report is an unweighted average of the elements or not. I am giving two forecasts for the WLI, one that includes and one that does not include the early monthly reports. The forecast assumes an unweighted index.

The following weekly components changed as follows for the week ending January 6 (YoY change in parenthesis):

DJ Bond Avg -.07 to 114.58, or -0.1% (YoY up from 111.12, or +3.1%)

S&P 500 +20.21 to 1277.81, or +1.6% (YoY up from 1271.50, or +0.5%)

Initial Jobless claims*: +27,000 to 399,000 or -6.8% w/w (YoY -15,000 from 414,000, or +4.8%)

Commodity price changes: +2.47 to 119.81, so +2.1% (YoY -17.05 from 133.65, or -10.4%)

Purchase Mortgage applications: +8.1% w/w (YoY -17.9%)

10 year treasury - BAA credit spread*: +.02 to 3.29%, or -0.6% (YoY up from 2.69%, or -18.2%)

If only weekly series are used, the predicted week over week change is +0.7, and the YoY growth rate is -6.4.

The following early monthly reports changed as follows (YoY change in parenthesis):

Avg manufacturing workweek +.1 to 41.5, or +0.2% (+.2 YoY, or +0.5%)

Unemployment 0-5 weeks*:+159 to 2669, or -6.0% (YoY -32, or +1.2%)

ISM vendor performance flat at 49.9, or 0.0 (YoY -6.8, or -12%)

ISM inventory change -1.2 to 47.1, or -2.5% (YoY -4.7 or -9.1%)

If the early monthly reports are included, the unweighted predicted weekly change is -0.4 and the YoY growth rate is -5.8.

[*Note: these are inverse relationships, so the higher the number, the lower the growth score]

We'll have an answer tomorrow. I anticipate refining the forecast as I am able to determine better how ECRI constructs their Index.

Morning Market

Yesterday, commenter I Will Not Accept the Terms of Service (great name, BTW) asked the following question:

These charts of been going up for 2 weeks And you still arent impressed? ;-)

We followed with a few exchanges, which ended with this (from him): At the same time, if stocks rise and bonds haven't yet started falling, that means there's still a lot of money sitting outside the equity market wondering if it should come back. I guess maybe you really just want to see it take off first before committing... which is okay I guess.

This gives me a good set-up to the way I look at the markets.

I'm a huge fan of inter-market analysis. Put another way, one market's price action does not happen in a vacuum. Other markets and the economy also have to act/react in certain ways. We also have to consider the fundamental economic situation to see if that information jibes with the markets. For more on this, I would suggest reading John Murphy's Intermarket Analysis, or Martin Pring's The All Season Investor.

Yesterday, I posted an article titled, "What Will It Take For Me to Be Impressed With the Markets?" where I outlined other technical developments that I need to see. First, it's not important to me that the markets are rising, but how they are rising. To me, the equity price charts are very weak -- the candles are small, intra-day action is weak and volume is low. In addition, we haven't seen other markets either sell-off (the treasury market) or rally (copper). If the stock market were really in a strong upswing we'd see money come out of the safety bid (treasuries) and more money move into industrial commodities (copper). Also consider that as of the end of last year the best performing market for a year was the treasury market -- which is not a harbinger of a strong equity market. Finally, while the US' fundamental situation is improving, Europe is on (or at the beginning of) a recession and Asia is slowing. Can the US realistically de-couple from these markets and not have it effect growth? I have my doubts on that.

Finally, let me add this: I could be wrong. The markets like to make an ass out of all analysis (myself included) on a regular basis. So, I would recommend that you also read the writings of a more bullish analyst as well because they could be seeing things correctly.

All that being said, something I forget to add to my "What Will It Take For Me to Be Impressed With the Markets" article was the dollar. For the last 6-9 months, the dollar has been the beneficiary of a safety bid, largely caused by the declining euro. However, there has been talk in the currency markets that the dollar may now be benefiting from the "risk on" trade. This means that as the US economy improves, more international investors want to invest here, which increases the dollar's value.

The dollar spent the last quarter of the year in a symmetrical consolidation pattern. Prices broke out mid-December and have drifted higher since. However, notice the weakening position in the A/D and CMF; both are indicating that the volume inflow is declining. In addition, the MACD is even and not showing much momentum. For the dollar, the big question is, "is this now rising because of increased confidence in the US economy, or is it a safety trade because of a declining euro?" I think it's a bit of both right now, meaning a continued move higher in the dollar would be a net positive.

In addition

Yesterday, copper had a nice pop and is now right at upside resistance. Which we're not out of the woods yet, we are closer.

In addition, industrial metals (which includes copper) have moved through resistance and are now approaching resistance. While the MACD has given a buy signal, the EMA picture is still weak and the CMF/A/D picture is muted.

The treasury market is the biggest stick in the mud. The daily chart shows prices are rising and the weekly chart shows prices are still above the long-term trend line.

So, the short version is the conditions are improving; the dollar is rising (some of which is a risk on trade) and copper specifically and industrial metals generally are improving. But the treasury market is still strong, which is not equity positive and which ultimately gives me great pause.

These charts of been going up for 2 weeks And you still arent impressed? ;-)

We followed with a few exchanges, which ended with this (from him): At the same time, if stocks rise and bonds haven't yet started falling, that means there's still a lot of money sitting outside the equity market wondering if it should come back. I guess maybe you really just want to see it take off first before committing... which is okay I guess.

This gives me a good set-up to the way I look at the markets.

I'm a huge fan of inter-market analysis. Put another way, one market's price action does not happen in a vacuum. Other markets and the economy also have to act/react in certain ways. We also have to consider the fundamental economic situation to see if that information jibes with the markets. For more on this, I would suggest reading John Murphy's Intermarket Analysis, or Martin Pring's The All Season Investor.

Yesterday, I posted an article titled, "What Will It Take For Me to Be Impressed With the Markets?" where I outlined other technical developments that I need to see. First, it's not important to me that the markets are rising, but how they are rising. To me, the equity price charts are very weak -- the candles are small, intra-day action is weak and volume is low. In addition, we haven't seen other markets either sell-off (the treasury market) or rally (copper). If the stock market were really in a strong upswing we'd see money come out of the safety bid (treasuries) and more money move into industrial commodities (copper). Also consider that as of the end of last year the best performing market for a year was the treasury market -- which is not a harbinger of a strong equity market. Finally, while the US' fundamental situation is improving, Europe is on (or at the beginning of) a recession and Asia is slowing. Can the US realistically de-couple from these markets and not have it effect growth? I have my doubts on that.

Finally, let me add this: I could be wrong. The markets like to make an ass out of all analysis (myself included) on a regular basis. So, I would recommend that you also read the writings of a more bullish analyst as well because they could be seeing things correctly.

All that being said, something I forget to add to my "What Will It Take For Me to Be Impressed With the Markets" article was the dollar. For the last 6-9 months, the dollar has been the beneficiary of a safety bid, largely caused by the declining euro. However, there has been talk in the currency markets that the dollar may now be benefiting from the "risk on" trade. This means that as the US economy improves, more international investors want to invest here, which increases the dollar's value.

The dollar spent the last quarter of the year in a symmetrical consolidation pattern. Prices broke out mid-December and have drifted higher since. However, notice the weakening position in the A/D and CMF; both are indicating that the volume inflow is declining. In addition, the MACD is even and not showing much momentum. For the dollar, the big question is, "is this now rising because of increased confidence in the US economy, or is it a safety trade because of a declining euro?" I think it's a bit of both right now, meaning a continued move higher in the dollar would be a net positive.

In addition

Yesterday, copper had a nice pop and is now right at upside resistance. Which we're not out of the woods yet, we are closer.

In addition, industrial metals (which includes copper) have moved through resistance and are now approaching resistance. While the MACD has given a buy signal, the EMA picture is still weak and the CMF/A/D picture is muted.

The treasury market is the biggest stick in the mud. The daily chart shows prices are rising and the weekly chart shows prices are still above the long-term trend line.

So, the short version is the conditions are improving; the dollar is rising (some of which is a risk on trade) and copper specifically and industrial metals generally are improving. But the treasury market is still strong, which is not equity positive and which ultimately gives me great pause.

Wednesday, January 11, 2012

Bonddad Linkfest?

- Euro drops on Fitch statement (BB)

- US farmers probably planted the most wheat in three years (BB)

- Treasury sees record bid for latest 3-year auction (BB)

- Germany on brink of recession (BB)

- EU banks hoarding cash (BB)

- EU businesses welcome the declining euro (FT)

- Why Best Buy is going out of business gradually (Forbes)

- The people v. Best Buy, Round 2 (Forbes)

- US Homebuilders surge (FT)

- Will South Carolina be different for Romney? (TPM)

What's Holding the Economy Back?

For the last year and half, the US economy has not been able to get to "escape velocity" -- a rate of growth over 3%. There are several reasons for this with the biggest one being the lower level of consumer spending. Consider this chart of the seasonally adjusted annual rate of change of personal consumption expenditure growth:

For the latest expansion, we've seen growth rates right around 2.5%. However, this rate is low when compared to the last two expansions. Consumers are spending; just not in the same amounts as before. As such, we are seeing lower growth. Because consumers make-up 70% of GDP growth, this is a very important issue. In addition,

austerity is hurting growth. The above chart shows the impact of government spending on overall economic growth. Over the last 8 quarters, government spending has subtracted from growth. In other words, a contractionary policy is, well, contractionary.

The above chart shows the percentage contribution to GDP from commercial real estate and the bottom charts shows the percentage contribution from residential construction. The commercial chart is a bit more positive, but it's still very weak. The residential charts is terrible. At least it's been hurting less over the last four quarters.

Both of these charts show that we're not building anything right now which has a tremendous impact on the economy. First, it creates jobs. But the actual building requires raw materials such as wood, copper etc.. which have to be mined. The process involves heavy machinery -- which increases durable goods manufacturing. And once the structure is build, we have to put furniture in it. In short, construction has a very large multiplier effect that we're simply not seeing right now. For more on this topic, see this paper from Edward Leamer.

So, we have the following:

1.) A weaker consumer. Consumer spending comprises 70% of the economy. While the consumer is spending, he's simply not spending as much.

2.) Austerity. Since 1970, federal government spending has accounted for about 20% of overall GDP. As I've shown in the Bonddad Economic History Project, government spending for the Korean War was a tremendous driver of the early 1950s expansion. For 6 of the last 8 quarters, we've seen government spending subtract from overall growth.

3.) A lack of housing participation. Housing -- and it's incredibly important multiplier effect -- are absent from this recovery.

Remember, the GDP equation is

Consumer spending + gross investment + net exports + government spending = GDP.

Elements 1 and 2 are weaker, element 3 has subtracted from growth for the last 10+ years and we've deliberately letting element 4 subtract from growth.

For the latest expansion, we've seen growth rates right around 2.5%. However, this rate is low when compared to the last two expansions. Consumers are spending; just not in the same amounts as before. As such, we are seeing lower growth. Because consumers make-up 70% of GDP growth, this is a very important issue. In addition,

austerity is hurting growth. The above chart shows the impact of government spending on overall economic growth. Over the last 8 quarters, government spending has subtracted from growth. In other words, a contractionary policy is, well, contractionary.

The above chart shows the percentage contribution to GDP from commercial real estate and the bottom charts shows the percentage contribution from residential construction. The commercial chart is a bit more positive, but it's still very weak. The residential charts is terrible. At least it's been hurting less over the last four quarters.

Both of these charts show that we're not building anything right now which has a tremendous impact on the economy. First, it creates jobs. But the actual building requires raw materials such as wood, copper etc.. which have to be mined. The process involves heavy machinery -- which increases durable goods manufacturing. And once the structure is build, we have to put furniture in it. In short, construction has a very large multiplier effect that we're simply not seeing right now. For more on this topic, see this paper from Edward Leamer.

So, we have the following:

1.) A weaker consumer. Consumer spending comprises 70% of the economy. While the consumer is spending, he's simply not spending as much.

2.) Austerity. Since 1970, federal government spending has accounted for about 20% of overall GDP. As I've shown in the Bonddad Economic History Project, government spending for the Korean War was a tremendous driver of the early 1950s expansion. For 6 of the last 8 quarters, we've seen government spending subtract from overall growth.

3.) A lack of housing participation. Housing -- and it's incredibly important multiplier effect -- are absent from this recovery.

Remember, the GDP equation is

Consumer spending + gross investment + net exports + government spending = GDP.

Elements 1 and 2 are weaker, element 3 has subtracted from growth for the last 10+ years and we've deliberately letting element 4 subtract from growth.

What Will It Take For Me To Be Impressed With the Markets?

Since the beginning of the year, I've been complaining about the market rally. While it technically looks like it's rallying, the rally is very weak. Frankly, I don't think it's a rally that has any legs. However, here are the conditions I need to see to be impressed.

1.) Print some strong bars: We've seen a lot of very weak candles on the daily chart. What we really need to see is strong, intra-day price action. In fact, we need to see several days of strong, intra-day price action -- say, 1%+ for 2-3 days on really good volume. Having the trading end on the highs of the day on a volume spike would be great. And having the intra-day rally move higher would be stellar. Instead, what we've seen for the last week is a lot of sideways trading, which is not exciting me.

2.) Copper has to break out. Right now, copper is trading in a downward range:

Copper has to make strong move higher, indicating that industrial demand is picking up again. The good news from the commodity markets is that we're already seeing the grain markets rally. But, we really need to see the industrial metals pop.

3.) We have to have a sell-off in the treasury markets. So long as there is a safety bid in the market in the form of the treasury market, money will get sucked away from the equity market. What we need to see is traders throw-in the towel on the safety trade and plow their sale proceeds into the equity markets.

1.) Print some strong bars: We've seen a lot of very weak candles on the daily chart. What we really need to see is strong, intra-day price action. In fact, we need to see several days of strong, intra-day price action -- say, 1%+ for 2-3 days on really good volume. Having the trading end on the highs of the day on a volume spike would be great. And having the intra-day rally move higher would be stellar. Instead, what we've seen for the last week is a lot of sideways trading, which is not exciting me.

2.) Copper has to break out. Right now, copper is trading in a downward range:

Copper has to make strong move higher, indicating that industrial demand is picking up again. The good news from the commodity markets is that we're already seeing the grain markets rally. But, we really need to see the industrial metals pop.

3.) We have to have a sell-off in the treasury markets. So long as there is a safety bid in the market in the form of the treasury market, money will get sucked away from the equity market. What we need to see is traders throw-in the towel on the safety trade and plow their sale proceeds into the equity markets.

Morning Market

The 60 minute IWM chart shows that prices gapped higher yesterday. This is technically good, but notice (again) the lack of follow through. Prices gapped and then stopped.

The daily chart shows the remarkable lack of strong bars over the last week and a half. Most bars have very small bodies and small shadows. There is simply no conviction in the market.

In fact, the QQQs gapped higher and then moved lower throughout the session. Notice that prices closed near the low of the day -- not the high. This is not a sign of strength.

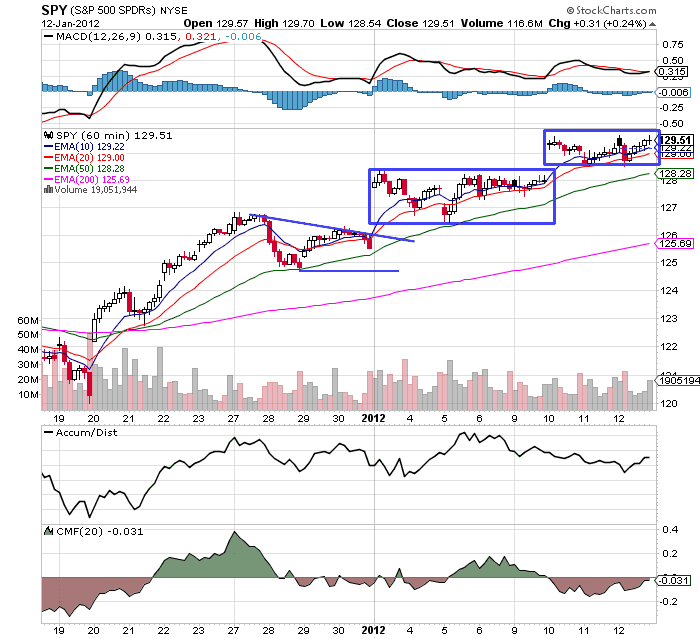

And while the SPYs have technically broken out, I've circled the price clusters the index has formed. Instead of making a strong move through resistance on heavy volume, prices moved higher and then moved sideways for about a week (the first circled area). Then prices gapped higher and formed a second price cluster.

And notice that various sectors of the market are suffering from the same weak conditions.

Tuesday, January 10, 2012

1951 Summation

Below are links to all the posts on 1951, which are part of the Bonddad Economic History Project

Employment and Income

Exports and Imports

Investment

PCEs, Income and Savings

GDP

Fed policy and inflation

Employment and Income

Exports and Imports

Investment

PCEs, Income and Savings

GDP

Fed policy and inflation

Bonddad Linkfest

- Copper climbs most in a week (BB)

- Hedge funds bearish on US equities (BB)

- US consumer credit increases most since 2001(Reuters)

- French business confidence increases (BB)

- China's trade surplus the lowest since 2005 (WSJ)

- Sluggish Chinese imports hint of lower domestic demand (FT)

- China's copper imports hit record (FT)

- Italian banks borrow 210 billion euros from the ECB (FT)

- Distorted US employment indicators (Dr. Ed Yardeni)

- High Yield Spreads on the decline (Bespoke)

1951; Prices and Fed Policy

This is part of the Bonddad Economic History Project

Remember that the early 1950s saw tremendous growth in consumer demand and employment growth (see here and here). Hence there is s tremendous amount of demand pull inflation in the economy. In addition, the US is now producing for a massive war effort, which greatly increases the demand of basically every raw material. As such, inflation increases. Yet, in 1951 we see a decrease in inflation, which leads to the question, why?

Price controls. In 1951, Congress passed the General Ceiling Price Regulation of 1951, which froze prices at their highest level reached in late December 1950 and late January 1951.

Also of extreme importance this year was the Treasury Fed-Accord of 1951, which was:

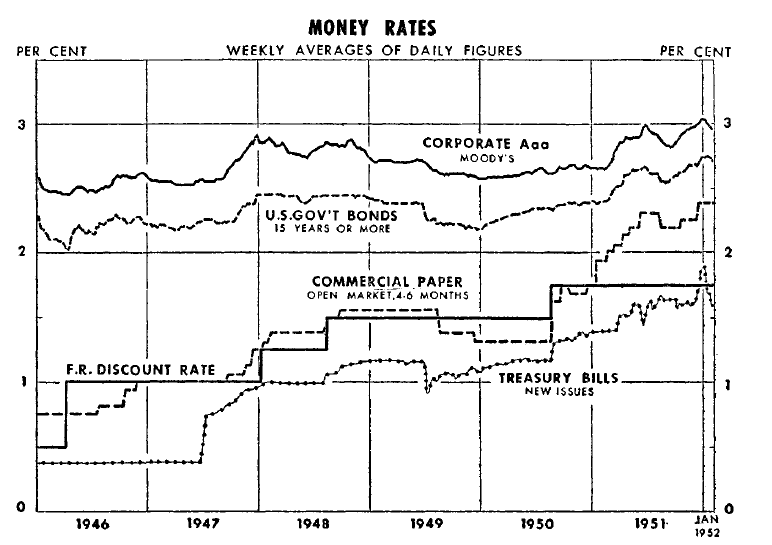

Business loans still grew at a strong rate, largely thanks to loans for essential war activity. The constraints on consumer lending show clearly on the chart (and below, which show a small .1% increase in consumer lending) as does the constraints on mortgage credit.

The above chart shows the overall upward drift of interest rates in the government security areas, which was primarily caused by the new arrangement between the Fed and the Treasury department.

The above chart shows the overall upward drift of interest rates in the government security areas, which was primarily caused by the new arrangement between the Fed and the Treasury department.

Finally, consider the following charts of inflation from the 1952 Economic Report to the President.

Remember that the early 1950s saw tremendous growth in consumer demand and employment growth (see here and here). Hence there is s tremendous amount of demand pull inflation in the economy. In addition, the US is now producing for a massive war effort, which greatly increases the demand of basically every raw material. As such, inflation increases. Yet, in 1951 we see a decrease in inflation, which leads to the question, why?

Price controls. In 1951, Congress passed the General Ceiling Price Regulation of 1951, which froze prices at their highest level reached in late December 1950 and late January 1951.

Also of extreme importance this year was the Treasury Fed-Accord of 1951, which was:

Agreement between the U.S. Treasury Department and the Federal Reserve Board of Governors that enabled the Fed to pursue an active Monetary Policy, independent of the Treasury and the federal government. Before 1951, the Fed had to assure low cost Treasury financing by purchasing Treasury securities at a set price. Afterward, the Federal Reserve Open Market Committee was able to purchase as much, or as little, of Treasury securities offered for sale by the Treasury Department as it wanted, instead of having to buy whatever the Treasury issued at the prevailing rate. Also known as the Treasury-Fed Accord.You can read a more complete history at the Richmond Fed.

Business loans still grew at a strong rate, largely thanks to loans for essential war activity. The constraints on consumer lending show clearly on the chart (and below, which show a small .1% increase in consumer lending) as does the constraints on mortgage credit.

Finally, consider the following charts of inflation from the 1952 Economic Report to the President.

2012: Housing, Oil, and the race between Deleveraging and Deflaton

- by New Deal democrat

Part I: The K.I.S.S. method forecast

This is one of those times when I am working on so much different material that nothing gets finished on time, like my year-end review of housing sales and prices, and reflections on the Oil choke collar. The good news is, I have been spending so much time decoding ECRI's black box (with a great deal of success, I might add. It just isn't finished yet) that I can give you a much more detailed forecast for 2012.

Let me begin this year the same way I began last year: why I use the K.I.S.S. method of forecasting. Even though the LEI is the statistic most denigrated by Wall Street forecasters, it has the inconvenient habit of being right more often than the highly-paid punditocracy, especially at turning points.

Since I'm not a highly paid Wall Street pundit, I simply rely upon the LEI for the short term, and the yield curve for the longer term with the caveat of watching out for deflation. The simple fact is, with one exception, if real M1, and real M2 (less 2.5%), are positive, and the yield curve 12 months ago was positive, the economy has always been in expansion. When real money supply is negative, and the yield curve was inverted 12 months ago, the economy has always been in contraction. The exception is that the yield curve does not help to project the economy 12-16 months later if the economy at that later date is in deflation - as it was in 1930-32 and late 2008 through early 2009 - which will feature a negative real money supply.

The simplest forecast, therefore, is that since the LEI were positive all during 2011, and since both M1 and M2 are positive -- in fact, courtesy of the tsunami of cash that washed ashore in August and September due to the Euro crisis, both have been almost off-the-charts YoY positive for the last few months -- and since the yield curve did not invert at any point in the last year, so long as we don't fall into deflation we should have growth all through 2012.

This year, though, simply citing leading indicators is uniquely complicated because of what Doug Short calls The Great Leading Indicator Smackdown. The Conference Board's LEI shows clear sailing ahead. ECRI called for a recession to begin by the end of 2011, and has insisted that at very least one will begin by the end of this half. Here's Doug Short's close-up of the divergence between the two indexes:

The divergence is due in part to differing approaches, and in part to what are elements of the indexes. ECRI makes use of long, short, and weekly leading indicator indexes, while the Conference Board relies upon one mixed medium-term index. While we don't know exactly what is in ECRI's black boxes, we do know what indexes they inherited from their founder, Prof. Geoffrey Moore. Specifically, we know his proposed long leading index consisted of real M2 money supply, the Dow Jones Bond Average, housing permits, and a measure of corporate profits. His proposed WLI included weekly readings of M2, the DJBA, the S&P500, Dun and Bradstreet's business birth/death count, and (probably) the Mortgage Bankers Association's Purchase Mortage Index, and credit spreads. The Conference Board, by contrast, does not make use of the DJBA or corporate profits, but does include the yield curve.

That difference is crucial. In fact at some point between December 2009 and June 2011 one or more of ECRI's 4 legacy long leading indicators were always negative: real M2 (minus 2.5%) was negative the longest, but housing permits also declined by 150,000 between April 2010 and February 2011, corporate profits dipped at the end of 2010, and the DJBA turned down between August 2010 and February 2011. Here's the graph, showing each of the LLI normed to 100 at their maximum reading before turning down in 2010 (note: substituting the nearly identical BAA bonds trend for the DJBA):

That is about equivalent to their collective negative turn in advance of the 2001 just-barely-a-recession, although the relative components were different. The yield curve, by contrast, did invert in 1999 but did not come close in 2011. Nor did real M1, which has also always turned negative before at the inception of a recession. Here's the equivalent graph with each LLI normed to 100 at their pre-2001 recession peak:

Since the long leading indicators are designed to give at least 12 months warning of a recession, that puts us in the greatest window of weakness right about now.

In this respect, the LEI aren't that different: their weakest readings were in April and September, and if you discount the M2 and yield curve readings, were negative in April and again from June through September (h/t EconomPicData):

meaning that they also forecast maximum weakness right about now.

Just as interestingly, though, all of ECRI's long leading indicators have turned up since last spring, with real M2 and the DJBA making new all time highs. Here's the same graph we looked at above -- you can see that all 4 LLI's have rebounded and two have made new highs:

This, plus the positive yield curve, tells me that for the second half of 2012, the indicators are really in agreement -- there will be growth.

So what do the shorter leading indicators say about the first half of 2012? I'll spare you a very noisy graph, but here's the scorecard:

Part I: The K.I.S.S. method forecast

This is one of those times when I am working on so much different material that nothing gets finished on time, like my year-end review of housing sales and prices, and reflections on the Oil choke collar. The good news is, I have been spending so much time decoding ECRI's black box (with a great deal of success, I might add. It just isn't finished yet) that I can give you a much more detailed forecast for 2012.

Let me begin this year the same way I began last year: why I use the K.I.S.S. method of forecasting. Even though the LEI is the statistic most denigrated by Wall Street forecasters, it has the inconvenient habit of being right more often than the highly-paid punditocracy, especially at turning points.

Since I'm not a highly paid Wall Street pundit, I simply rely upon the LEI for the short term, and the yield curve for the longer term with the caveat of watching out for deflation. The simple fact is, with one exception, if real M1, and real M2 (less 2.5%), are positive, and the yield curve 12 months ago was positive, the economy has always been in expansion. When real money supply is negative, and the yield curve was inverted 12 months ago, the economy has always been in contraction. The exception is that the yield curve does not help to project the economy 12-16 months later if the economy at that later date is in deflation - as it was in 1930-32 and late 2008 through early 2009 - which will feature a negative real money supply.

The simplest forecast, therefore, is that since the LEI were positive all during 2011, and since both M1 and M2 are positive -- in fact, courtesy of the tsunami of cash that washed ashore in August and September due to the Euro crisis, both have been almost off-the-charts YoY positive for the last few months -- and since the yield curve did not invert at any point in the last year, so long as we don't fall into deflation we should have growth all through 2012.

This year, though, simply citing leading indicators is uniquely complicated because of what Doug Short calls The Great Leading Indicator Smackdown. The Conference Board's LEI shows clear sailing ahead. ECRI called for a recession to begin by the end of 2011, and has insisted that at very least one will begin by the end of this half. Here's Doug Short's close-up of the divergence between the two indexes:

The divergence is due in part to differing approaches, and in part to what are elements of the indexes. ECRI makes use of long, short, and weekly leading indicator indexes, while the Conference Board relies upon one mixed medium-term index. While we don't know exactly what is in ECRI's black boxes, we do know what indexes they inherited from their founder, Prof. Geoffrey Moore. Specifically, we know his proposed long leading index consisted of real M2 money supply, the Dow Jones Bond Average, housing permits, and a measure of corporate profits. His proposed WLI included weekly readings of M2, the DJBA, the S&P500, Dun and Bradstreet's business birth/death count, and (probably) the Mortgage Bankers Association's Purchase Mortage Index, and credit spreads. The Conference Board, by contrast, does not make use of the DJBA or corporate profits, but does include the yield curve.

That difference is crucial. In fact at some point between December 2009 and June 2011 one or more of ECRI's 4 legacy long leading indicators were always negative: real M2 (minus 2.5%) was negative the longest, but housing permits also declined by 150,000 between April 2010 and February 2011, corporate profits dipped at the end of 2010, and the DJBA turned down between August 2010 and February 2011. Here's the graph, showing each of the LLI normed to 100 at their maximum reading before turning down in 2010 (note: substituting the nearly identical BAA bonds trend for the DJBA):

That is about equivalent to their collective negative turn in advance of the 2001 just-barely-a-recession, although the relative components were different. The yield curve, by contrast, did invert in 1999 but did not come close in 2011. Nor did real M1, which has also always turned negative before at the inception of a recession. Here's the equivalent graph with each LLI normed to 100 at their pre-2001 recession peak:

Since the long leading indicators are designed to give at least 12 months warning of a recession, that puts us in the greatest window of weakness right about now.

In this respect, the LEI aren't that different: their weakest readings were in April and September, and if you discount the M2 and yield curve readings, were negative in April and again from June through September (h/t EconomPicData):

meaning that they also forecast maximum weakness right about now.

Just as interestingly, though, all of ECRI's long leading indicators have turned up since last spring, with real M2 and the DJBA making new all time highs. Here's the same graph we looked at above -- you can see that all 4 LLI's have rebounded and two have made new highs:

This, plus the positive yield curve, tells me that for the second half of 2012, the indicators are really in agreement -- there will be growth.

So what do the shorter leading indicators say about the first half of 2012? I'll spare you a very noisy graph, but here's the scorecard:

- The positives are that the stock market has been rallying for the last 5 months, durable goods orders are still climbing, and consumer expectations have regained virtually all their losses from the July debt debacle. Initial jobless claims have come down to 3 1/2 year lows.

- The negatives are that the ISM manufacturing indexes have been just barely positive for most of the last 6 months, the vendor delivery subindex has declined substantially, and credit spreads are at their widest since 2009. Also, the gasoline price spike from a year ago has reached the point, based on past history, of maximum impact, and will remain there through April. Commodity prices are falling, and the last two months the CPI has actually registered deflation, raising a caution flag about relying upon the yield curve. Finally, as I will detail more in part 2, you can't go on forever with real wages in decline, as they have been for all of 2011.

One other item: typically recessions do not begin until at least 8 of the 10 LEI's are lower than they were 6 months ago: through November 6 are negative, 4 are positive. That's close, but not quite enough.

Ultimately the question as to whether the trend is slightly positive or slightly negative in the first part of 2012 becomes whether housing will show enough actual strength, and whether the Oil choke collar will weaken sufficiently, to support US growth if manufacturing and exports falter. For reasons I will explore more in part 2, my best judgment is that we will avoid recession, but that at least one quarter of negative GDP, with the likelihood greater in this quarter than the second quarter, can't be ruled out.

Ultimately the question as to whether the trend is slightly positive or slightly negative in the first part of 2012 becomes whether housing will show enough actual strength, and whether the Oil choke collar will weaken sufficiently, to support US growth if manufacturing and exports falter. For reasons I will explore more in part 2, my best judgment is that we will avoid recession, but that at least one quarter of negative GDP, with the likelihood greater in this quarter than the second quarter, can't be ruled out.

Morning Market -- Still Not Sold on the Rally

{kind=link}

First, I'm starting to feel like the great complainer regarding the latest developments in the equity markets. However, consider the above three charts, which are in the 30 minute time frame.

The IWMs opened the year by gapping higher and then fell. While it has rallied since then, it is still below the highs established on the gap higher. The IYTs are in the same boat. The SPYs are the same way, although they have moved a bit closer to their highs. The QQQs are the only averages who have continued their break-out and advanced to higher levels. In short, there just isn't any follow-through on the rally, and the length of time from the original pop to now is a big deal.

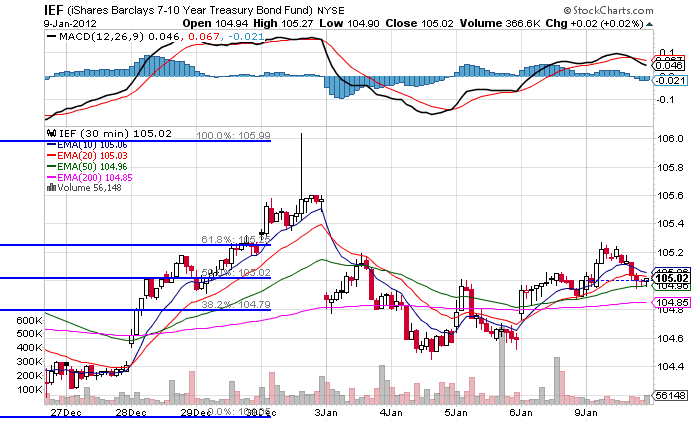

In addition, we see that the IEFs gapped lower, but haven't sold off any more. If we were seeing a big rush into equities, we'd probably be seeing a bigger sell-off in the treasury market.

After hitting resistance at the 38.2% Fibonacci level and selling off into the EMAs, the grains ETF has a nice move higher yesterday. Notice the upward momentum implied by the EMAs -- the shorter EMAs are rising and the 50 is also turning positive, although at a smaller angle. We see overhead resistance at the 38.2% Fib level and the 200 day EMA.

Oil is still trapped below resistance established in November. The volume indicators tell us there has not been a major move out of the security, but we also haven't seen a big rush in yet.

Subscribe to:

Posts (Atom)