Saturday, April 29, 2017

Weekly Indicators for April 24 - 28 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com. Stagnant real wages helped make for a punk Q1 GDP report, but the nowcast and the forecast still look positive.

Friday, April 28, 2017

Two hits and a miss on GDP and wages

- by New Deal democrat

We got two pieces of good news from the GDP report this morning, and one piece of bad news for workers.

First, from the important long leading housing sector, real private fixed residential investment rose again to a new post-recession high:

This adds to the generally positive data coming out of that sector.

Second, proprietors income increased:

This is a good proxy for corporate profits, which won't be reported until next month. It isn't quite as reliable an indicator, but the two generally move in the same direction,

So the two long leading aspects of the GDP report were hits.

So the two long leading aspects of the GDP report were hits.

This miss was in the Employment Cost Index. Since this is a median measure, it is not distorted by outsized gains at the top of the distribution. While this measure rose +0.8% in the quarter, inflation increased at least as much, meaning that median real earnings were stagnant:

Had I used persoal consumption expenditures as my deflator, real wages would actually show a decline.

That inflation has been more than eating up nominal gains in wages for the last three quarters is not good news.

Wednesday, April 26, 2017

Declining positivity of background money and financial indicators

- by New Deal democrat

The supply, cost, and rationing of money and credit set the background for almost all other indicators. I take a look at what they look like now over at XE.com.

Tuesday, April 25, 2017

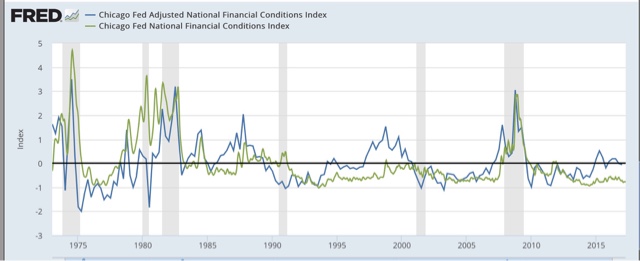

A high frequency indicator for credit conditions: the Chicago Fed'sFinancial Conditions Index

- by New Deal democrat

One particularly useful leading indicator that is handicapped by being reported only quarterly, and late, is the Senior Loan Officer Survey. This tells us whether banks have been tightening or loosening credit standards in the preceding quarter.

It has a 30 year history and has typically reported net tightening about 1 year before a recession, with a fair amount of variability, rapidly intensifying as the recession is about to start, typically showing net tightening about 1 or 2 quarters after corporate profits peak:

But the problem is, for example, that we won't learn about the first Quarter of 2017 for several more weeks. So I have been looking to find a proxy that is reported on a more frequent and timely basis. I have now found it: the Chicago Fed's Financial Conditions Index.

Here is the detailed explanation, according to the Chicago Fed:

The Chicago Fed’s National Financial Conditions Index (NFCI) provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets, and the traditional and “shadow” banking systems. Because U.S. economic and financial conditions tend to be highly correlated, we also present an alternative index, the adjusted NFCI (ANFCI). This index isolates a component of financial conditions uncorrelated with economic conditions to provide an update on how financial conditions compare with current economic conditions

.....

A zero value for the NFCI can be thought of as the U.S. financial system operating at historical average levels of risk, credit, and leverage. The ANFCI removes the variation in these indicators attributable to economic activity, as measured by the three-month moving average of the Chicago Fed National Activity Index (CFNAI), and inflation, according to its three-month total based on the Personal Consumption Expenditures (PCE) Price Index. As such, a zero value for the ANFCI corresponds with a financial system operating at historical average levels of risk, credit, and leverage consistent with economic activity and inflation.

Positive values of the NFCI indicate financial conditions that are tighter than on average, while negative values indicate financial conditions that are looser than on average. Similarly, positive values of the ANFCI indicate financial conditions that are tighter on average than would be typically suggested by current economic conditions, while negative values indicate the opposite.

The NFCI is made up of over a dozen components, including 2 year Swaps and Libor vs. the TED spread, which also are components of the Conference Board's "leading credit index" that is one of the 10 components of the monthly Index of Leading Indicators.

Here is what the Financial Conditions Index, averaged quarterly, looks like compared with the Senior Loan Officer Survey:

This is a pretty close match, except that the Senior Loan Officer Survey's crossover point between tightening and loosening equates to a -0.5 reading on the NFCI.

When we compare the Adjusted Financial Conditions Index with the NFCI, we see that while it is more volatile, it appears to lead by about 6 months:

What this tells us is that background economic conditions tend to move in the direction of credit standards.

What this tells us is that background economic conditions tend to move in the direction of credit standards.

Additionally, the Chicago Fed also touts the Leverage subindex of the NFCI as leading GDP:

So in the next graph we can see the AFNCI (blue) compared with the Senior Loan Officer Survey (red) and the Leverage subindex (purple):

Both the AFNCI and the Leverage subindex appear to lead the Senior Loan Officer Survey by a year or more, but are noisy as for example in 1990 and 2001, where at least one of the two had already turned negative, indicating loosening compared with economic conditions, a year before the Senior Loan Officer Survey spiked coincident with recessions.

Putting this all together, the history of the Financial Conditions Indexes suggest that a positive value of the ANFCI or the Leverage subindex, or a reading higher than -0.5 in the NFCI, correlate with a tightening of credit conditions. Values above +0.5 (as adjusted in the case of the NFCI) should put us on higher alert for a recession, and values above +1.0 signal danger, in 1-3 years in the case of the ANFCI or the Leverage subindex, or 1 year or less in the case of the NFCI.

So in the next graph we can see the AFNCI (blue) compared with the Senior Loan Officer Survey (red) and the Leverage subindex (purple):

Both the AFNCI and the Leverage subindex appear to lead the Senior Loan Officer Survey by a year or more, but are noisy as for example in 1990 and 2001, where at least one of the two had already turned negative, indicating loosening compared with economic conditions, a year before the Senior Loan Officer Survey spiked coincident with recessions.

Putting this all together, the history of the Financial Conditions Indexes suggest that a positive value of the ANFCI or the Leverage subindex, or a reading higher than -0.5 in the NFCI, correlate with a tightening of credit conditions. Values above +0.5 (as adjusted in the case of the NFCI) should put us on higher alert for a recession, and values above +1.0 signal danger, in 1-3 years in the case of the ANFCI or the Leverage subindex, or 1 year or less in the case of the NFCI.

Finally, here is a close-up of the last two years of the weekly values of the ANFCI (blue), the NFCI (green), and the Leverage subindex (purple) [In this graph I have added +0.5 to the NFCI per my comment above]:

Note that the ANFCI did reach above +0.5 for one month two years ago. But all 3 have been below zero for the last six months. This suggests that when the Senior Loan Officer Survey is reported next month, it is at very least likely to be neutral, and more likely than not will show a slight loosening of credit. In broader terms, it means that we now have a useful weekly indicator that tells us that credit conditions are not forecasting a recession.

I will begin to report this each week.

Dear Jazz: The First Thing to Do When You're Digging a Hole ...

The above picture is Jazz Shaw, who continually makes the argument that raising the minimum wage will cost jobs.

Mr. Shaw believes that a recent report published by the Harvard Business Review supports his conclusion. As I wrote, it doesn't (see here and here). But, being that Mr. Shaw is, well, dumber than a post, he'll keep making the argument. So, here's a key excerpt from a report that he claims supports his position

Our results contribute to the existing literature in several ways. First, our findings relate to a large literature seeking to estimate the impact of the minimum wage, most of which has focused on identifying employment effects. While some studies find no detrimental effects on employment (Card and Krueger 1994, 1998; Dube, Lester & Reich, 2010), others show that higher minimum wage reduces employment, especially among low-skilled workers (see Neumark & Wascher, 2007 for a review). However, even studies that identify negative impacts find fairly modest effects overall, suggesting that firms adjust to higher labor costs in other ways. For example, several studies have documented price increases as a response to the minimum wage hikes (Aaronson, 2001; Aaronson, French, & MacDonald, 2008; Allegretto & Reich, 2016). Horton (2017) find that firms reduce employment at the intensive margin rather than on the extensive margin, choosing to cut employees hours rather than counts. Draca et al. (2011) document lower profitability among firms for which the minimum wage may be more binding

Put more directly: the report that Mr. Shaw says supports his position in fact doesn't. The data -- as noted above -- says the opposite.

Now, does this matter to Shaw or the editors at Hot Air? No. They, in fact, could care less. They just know in their bones that they're right, so that's it. The above citation from the report -- which contradicts Hot Air's "analysis" -- is meaningless academic drivel written by liberal economists who are secretly in league .... you get the idea.

Monday, April 24, 2017

Sunday, April 23, 2017

A thought for Sunday: the economy is on autopilot. Pray that it stays that way

- by New Deal democrat

It's Sunday, so I get to step out from nerdy analysis, and opine as I please.

Back in 2014, when there was another GOP "wave" election in the Congress, I wrote that the silver lining was that we were at the best point in the economic cycle for it to function on autopilot for the next 24 months. In other words, almost all of the long term indicators were positive, so if all the Congress did in 2015-16 was agree to continue to pay the country's bills, we would probably be OK. And we were.

So, a little over 3 months into the Trump Administration, what action has it taken to materially change the economic trajectory?

Basically, nothing. Yes, a bunch of executive orders have been signed promising to undo Obama regulations, and the telecoms have gotten the right to sell all of your data, but in terms of actual action, the economy is still on autopilot.

All of the mid-cycle indicators have made their highs, and a couple of the long leading indicators have vacillated between neutral and negative, and a few more of them are weakening, but are still positive. If the economy stays on autopilot, it probably doesn't have a bad accident until at least the middle of next year -- although I do expect things like job and real wage growth, while still positive, to weaken.

So, the good news is that if Trump and the GOP Congress continue to be unable to form a majority to enact actual policy, we're not in any serious economic danger for now.

The bad news is that something might happen within the next week. If stopgap funding is not passed, at least a partial government shutdown seems likely. Actually welching on our debts is apparently still a few months off.

And Obama's negotiating with the hostage-takers at the time of the 2011 debt ceiling debacle is coming back to bit us in the butt, now that it serves as a precedent. First Trump threatened to cut off funding for Obamacare. The Democrats responded by insisting that its statutory funding be codified in the debt ceiling resolution (something that probably a lot of GOPers silently want to happen as well). Now Trump has threatened to shut down the government and stop paying its bills if he doesn't get all of his legislative wishes, like a border wall and a big tax cut for the wealthy, as part of the deal.

Since the odds of a 2/3's majority in both Houses of Congress overriding any Trump veto are essentially zero, the Full Faith and Credit of the United States is in the hands of an ignorant narcissist. One week from now, the economy might be taken off autopilot and deliberately steered into a mountainside.

For the record, I see no reason for Democrats to go along with any of this. The GOP is in nominal controls of both Houses of Congress, and there is a nominally GOP president. Time to put on their big boy pants and govern. If they won't do that, there is no reasonable rationale for trying to negotiate a less awful, but still awful, outcome.

Subscribe to:

Posts (Atom)