- by New Deal democrat

HEADLINES:

- +266,000 million jobs added: 218,000 private sector plus 48,000 government. The alternate, and more volatile measure in the household report indicated a gain of 328,000 jobs, which factors into the unemployment and underemployment rates below.

- U3 unemployment rate rose 0.1% to 6.1%, compared with the January 2020 low of 3.5%.

- U6 underemployment rate declined 0.3% to 10.4%, compared with the January 2020 low of 6.9%.

- Those on temporary layoff increased 88,000 to 2,114,000.

- Permanent job losers increased 97,000 to 3,529,000.

- February was revised upward by 68,000, while March was revised downward by 146,000, for a net loss of 78,000 jobs compared with previous reports.

Leading employment indicators of a slowdown or recession

I am still highlighting these because of their leading nature for the economy overall. These were almost uniformly negative, their worst performance in a year: - the average manufacturing workweek was unchanged at 41.6 hours. This is one of the 10 components of the LEI.

- Manufacturing jobs declined 18,000. Since the beginning of the pandemic, manufacturing has still lost -515,000, or 4.0% of the total.

- Construction jobs were unchanged. Since the beginning of the pandemic, -14,000 construction jobs have been lost, or 0.2% of the total.

- Residential construction jobs, which are even more leading, declined by 1,300. Since the beginning of the pandemic, there have still been almost 30,000 in gains in this sector.

- temporary jobs decreased by 111,400. Since the beginning of the pandemic, there have still been 184,800 jobs lost, or 6.3% of all temporary jobs.

- the number of people unemployed for 5 weeks or less rose fell by 79,000 to 2.414 million, 332,000 more than just before the pandemic hit.

- Professional and business employment declined by 79,000, which is still 685,000, or about 3.2%, below its pre-pandemic peak.

Wages of non-managerial workers

- Average Hourly Earnings for Production and Nonsupervisory Personnel: rose $0.20 to $25.45, which is a 1.2% YoY gain***WHICH IS THE LOWEST YOY GAIN IN THE ENTIRE NEARLY 60 YEAR HISTORY OF THIS SERIES.*** This is a huge reversal of the 5%+ YoY gains recently seen, and reflects the rehiring of low-wage workers in sectors like food and beverage serving.

Aggregate hours and wages:

- the index of aggregate hours worked for non-managerial workers was unchanged, which is a loss of -3.6% since just before the pandemic.

- the index of aggregate payrolls for non-managerial workers rose by 0.7%, which is a gain of 1.4% since just before the pandemic.

Other significant data:

- Full time jobs gained 935,000 in the household report.

- Part time jobs declined 54,000 in the household report.

- The number of job holders who were part time for economic reasons decreased by 583,000 to 5.243 million, which is an increase of 845,000 since before the pandemic began.

SUMMARY

Needless to say, this was a very disappointing report compared with all of the employment-related indicators we have seen in the past few weeks. My main thoughts are that (1) this was compositional; and (2) there is likely to be a substantial revision.

Usually when there is one report that sticks out like a sore thumb compared with other related data, it gets revised significantly. This is particularly so when one looks at the composition of the gains and losses in this report. Consider the following two points:

- there were job gains in food and drinking establishments of 187,000, over 2/3’s of the entire month’s improvements.

- the entire goods-producing sector of the US economy - which has been at very least red hot in the past few months - *lost* 16,000 jobs! This includes job losses in residential construction (housing), which has been going through the roof in recent months.

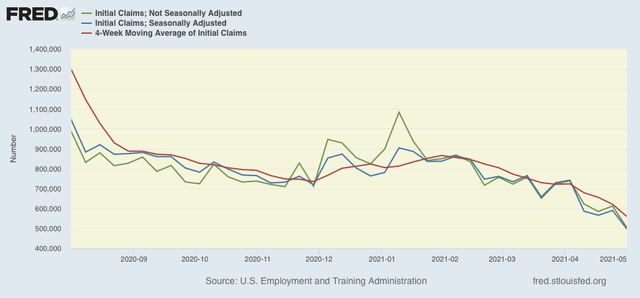

Another anomaly is that those unemployed less than 5 weeks, which usually correlates fairly closely with initial jobless claims, *increased* by 237,000; plus, both permanent and temporary layoffs *increased* - a direct contradiction to the big decline in new jobless claims in the past 6 weeks.

Another big compositional change was the big decline in temporary jobs, paired with a huge increase in full time employment. This suggests that previous temps were converted to permanent hires.

Finally, note that the YoY% increase in average wages completely reversed, and made an all-time series low (although still positive).

So, basically, either (1) bottlenecks in supplies caused a complete halt in the goods producing sector including both manufacturing and construction; plus there was an anomalous contraction in professional and business services; or (2) there will be substantial upward revisions to those aspects of the report. I am more inclined to believe that #2 is the primary driver of this relatively poor report than #1.