Saturday, September 15, 2012

Weekly Indicators: sharply bifurcated signals edition

- by New Deal democrat

The big monthly news this week was that inflation took off, with sharp increases in both producer and consumer prices, while industrial production and capacity utilization fell just as sharply. Retail sales rose slightly more than gasoline prices, but June and July were revised down slightly. Consumer sentiment improved sharply, and in particular expectations, one of the 10 components of the LEI.

The high frequency weekly indicators should show turns before they show up in monthly or quarterly data. Most of these remain quite positive, although employment indictors are concerning, and gas prices are at the highest levels ever for this time of year. Let's start once again with them.

The energy choke collar is solidly engaged, but gasoline usage is holding up:

Gasoline prices rose yet again last week, up $.01 from $3.84 to $3.85. Gas prices have risen $0.49 since their early July bottom, and are now only $0.09 cheaper than at their highest point this spring.Oil prices per barrel rose from $96.42 to $99.00. Gasoline usage was slightly negative on a YoY basis. For one week, it was 8695 M gallons vs. 8848 M a year ago, down -1.7%. The 4 week average at 9004 M vs. 9011 M one year ago, was essentially unchanged.

Employment related indicators were again mixed this week.

The Department of Labor reported that Initial jobless claims rose 17,000 to 382,000 from the prior week's unrevised figure. The four week average rose 3,750 to 375,000, about 3.3% above its post-recession low. If higher oil prices are again acting as a governor preventing fast economic growth, then this number, unforturnately, should continue to rise in coming weeks, although there is no persuasive impact yet.

The American Staffing Association Index fell by one to 92. This index was generally flat during the second quarter at 93 +/-1, and for it to be positive should have continued to rise from that level after its July 4 seasonal decline. That it has now actually declined again is a serious red flag, as it is still performing worse than it did in 2007 and 2011.

On the other hand, the Daily Treasury Statement showed that 8 days into September, $60.4 B was collected vs. $57.6 B a year ago, a $2.8 B or a 4% increase. For the last 20 days ending on Thursday, $129.4 B was collected vs. $120.6 B for the comparable period in 2011, a gain of $8.8 B or +7.3%.

Same Store Sales and Gallup consumer spending were all solidly positive:

The ICSC reported that same store sales for the week ending September 1 gained +1.0% w/w, and rose +3.4% YoY. Johnson Redbook reported a solid 2.7% YoY gain. The 14 day average of Gallup daily consumer spending as of September 13 was $70, compared with $65 last year for this period. Gallup's comparison plunged at the very end of August, but has rebounded somewhat since, after 5 strong weeks.

Bond yields were mixed but credit spreads contracted:

Weekly BAA commercial bond rates fell slightly -.01% to 4.82%. Yields on 10 year treasury bonds rose slightly, up .01% to 1.64%. The credit spread between the two narrowed to 3.18%, which is closer to its 52 week minimum than maximum, and continues to improve from several months ago.

Housing reports were all positive:

The Mortgage Bankers' Association reported that the seasonally adjusted Purchase Index rose about 8% from the prior week, and is also up about 7% YoY. Generally these are in the middle part of their 2+ year range. The Refinance Index also rose strongly, about +12% for the week, although the MBA cautioned that it may be an artifact from the Labor Day weekend.

The Federal Reserve Bank's weekly H8 report of real estate loans this week rose 15 to 3534. The YoY comparison rose to +1.7%, which is also the seasonally adjusted bottom. This is the best comparison in a long time.

YoY weekly median asking house prices from 54 metropolitan areas at Housing Tracker were up +2.2% from a year ago. YoY asking prices have been positive for over 9 months.

Money supply remains generally positive despite now being fully compared with the inflow tsunami of one year ago:

M1 rose sharply, up 4% last week alone, and was up +3.4% month over month. Its YoY growth rate also rose sharply to +12.6%, as comparisons with last year's tsunami of incoming cash are in full progress. As a result, Real M1 also rose to +10.9%. YoY. M2 increased +0.2% for the week, and was up 0.5% month/month. Its YoY growth rate also rose to +6.4%, so Real M2 remained the same at +4.7%. The growth rate for real money supply has slowed significantly, but is still quite positive.

Rail traffic was completely flat YoY due primarily to coal:

The American Association of Railroads reported that total rail traffic was unchanged YoY. Non-intermodal rail carloads were off a substantial -2.3% YoY or -6,300, once again entirely due to coal hauling which was off -11,800. Negative comparisons improved from 10 to 8 types of carloads. Intermodal traffic was up 6,400 or +3.1% YoY.

Turning now to high frequency indicators for the global economy:

The TED spread declined sharply to a new 52 week low of 0.29. The one month LIBOR also declined, to 0.220, and also set another new 52 week low. It remains well below its 2010 peak and is lower than almost the entire past 3 years. Even with the recent scandal surrounding LIBOR, it is probably still useful in terms of whether it is rising or falling.

The Baltic Dry Index fell yet again from 669 to 662, setting another 52 week low. The Harpex Shipping Index fell 3 from 393 to 390, and is now only 15 above its February 52 week low.

Finally, the JoC ECRI industrial commodities index rose once again from 122.23 to 124.64, although it is still down YoY. This number has improved sharply over the last month.

The sharp bifurcation in the numbers continued. Every single manufacturing number is either showing contraction or close thereto. The decline in the ASA's temporary staffing index is particularly concerning as to employment. Gasoline prices may be having an impact on hiring and a slight impact on layoffs so far. Rail traffic is completely flat YoY, although coal is playing the major role here. Globally, shipping rates continue to decline.

At the same time almost all of the housing indicators continue to show solid improvement, money supply is also strongly positive, bond yields are low, and credit spreads are continuing to contract. The stock indexes just made new multi-year highs. These are all long or medium term leading indicators, and suggest that the US economy's prospects generally remain good. On the employment front, Treasury receipts show no weakness at all. On the global front, rising natural resource prices and sharply declining short term interest rates are also very positive.

Continuing increases in gasoline prices as well as the apparent slight manufacturing contraction are making me more concerned about the remainder of this year and the first half of next year, but so long as the consumer continues to hold up, on balance my outlook is still very cautiously positive.

Have a good weekend.

Friday, September 14, 2012

A Long Time Ago, In A Galaxy Far, Far Away ....

More accurately, after college I was a professional musician in Austin, Texas for 5 years. I also spent a year at GIT in Los Angeles (or, more specifically, "Hollyweird"). I hadn't really played with people in a long time until this week when a local accountant invited my to jam. He has a monthly jam/networking, composed of professionals all of whom played in some capacity and enjoy reliving our wasted youth.

Anyway, this picture was taken at the jam, me, playing my '72 strat and reaching for an E7 grip. I had a ball.

Have a good weekend. I'll be back on Monday; NDD will be here on Saturday.

Uh oh: industrial production down, real retail sales still below March high

- by New Deal democrat

In line with Bonddad's last post, this morning's poor industrial production report (blue)adds to the evidence that this vital sector might actually be contracting. Further, although retail sales did increase, July's number was revised down, (red)and we are still below the level of earlier this year.

Add that together with the miserable employment report (green), and it is at least possible that a recession could have started in August (which would still mean that ECRI was wrong).

More on the Manufacturing Slowdown

From the latest ISM report:

This does not bode well for the second half of the year.

- "Internal indicators and feedback from sales channels are indicating a slowdown in demand for capital equipment." (Machinery)

- "Business continues to be very solid, but there is now a slowing of incoming orders." (Fabricated Metal Products)

- "Incoming orders have slowed somewhat, but indications are that there will be a stronger fourth quarter." (Plastics & Rubber Products)

- "Business is slow right now. Companies seem to be holding onto their money." (Computer & Electronic Products)

- "We can sense, feel and see headwinds with customer orders, especially Europe related." (Apparel, Leather & Allied Products)

- "New orders and backlog remain flat." (Miscellaneous Manufacturing)

- "Auto industry slowing a bit in the second half [of the year]." (Transportation Equipment)

- "U.S. drought severely impacting raw materials prices." (Food, Beverage & Tobacco Products)

- "Lackluster demand continues in all regions of the world, and is supporting much lower raw materials prices in the second half of 2012." (Chemical Products)

This does not bode well for the second half of the year.

Morning Market Analysis; Post Fed Wrap-Up

The SPYs have had two strong rallies this month. The first occurred on the 6th, after which prices consolidated for a week. Then yesterday prices again rallied. Notice the very strong volume readings for the session.

On the daily chart, we see a very strong price bar printed yesterday on a large volume spike. Note the continuing bullish orientation in the market. Momentum is increasing, prices are strengthening and the CMF is rising.

While the QQQs (top chart) did not confirm the rally the IWMs (lower chart) are.

For both of these charts, today will be an important trading day. Ideally, we'd like to see the rally continue and for the QQQs to break out.

After spiking in mid June and ending their rally in mid July, prices have been moving sideways, consolidating gains. Notice the declining MACD, which is typical for consolidation patterns. Also note the declining strength in prices -- which is relative.

Gold -- which was rallying -- had a strong jump yesterday on very strong volume. Also note the underlying strength in the market -- rising MACD, CMFs and EMAs.

Finally, we have the declining dollar, which is now near six month lows and in a clear downtrend.

Thursday, September 13, 2012

Bonddad Linkfest

- German high court backs ESM (BB)

- Indian IP up .1% (BB)

- South Korean Joblessness at 3.1% (BB)

- Nine deep thoughts on the latest WaPo poll (WaPo)

- Obama's electoral college edge (WaPo)

- US median income falls to 1996 levels (NYT)

- US jobless claims up 15,000 (Marketwatch)

- Latest USDA crop report gives corn traders hope (Agrimoney)

- European banking union unveiled (FT)

- South Korea leaves rates unchanged (BOK)

Uh oh: two hiring red flags (and one all clear)

- By New Deal democrat

Hot on the heals of Friday's miserably positive employment report, two more jobs measures are also raisng red flags:

In general, hiring seems to lead firing. In a slowdown, employers as a group stop hiring before they increase firing. Although the series has a very limited history, I've suggested that the JOLTS hiring series may be leading indicator. It ticked down in August, but more worryingly, it appears to be stalled if not rolling over:

Hardly dispositive, since it also stalled on 2010. But another indicator that tends to lead is temp hiring, and the American Staffing Association's index has actually declined slightly over the last quarter:

This series actually looks worse than in 2007, and more like 2008. Again, hardly dispositive, but indicative of a stall at least.

Meanwhile, Bespoke Investment Group notes the declining payrolls revisions, but urges caution.

On the bright side, even with today's relatively poor jobless claims number, the trend line of continuously declining YoY% comparisons is intact:

We'd need to see a few weeks of 390,000+ reports for me to be truly concerned.

Three Scary Charts from the Latest EU Monthly Report

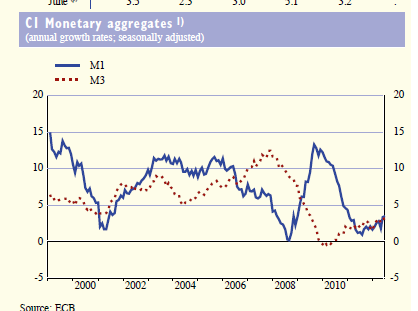

Every month, the ECB releases a report on the overall EU economy. In looking through the latest report, there are three charts that really jump out for their negative implications.

Overall monetary growth is incredibly weak and is at levels associated with recession.

Loans

are not not being made -- and have not been made to many people for the

duration of this expansion. Also note the overall negative reading of

consumer credit for the last few years -- that is definitely not good.

Loans

are not not being made -- and have not been made to many people for the

duration of this expansion. Also note the overall negative reading of

consumer credit for the last few years -- that is definitely not good.

Employment is clearly moving in the wrong direction.

Overall monetary growth is incredibly weak and is at levels associated with recession.

Employment is clearly moving in the wrong direction.

Morning Market Analysis; The Post ECB Bond Buying Equity Bump

Over the last week, we've had two important developments in Europe. First, the ECB announced a bond-buying program. This has long been rumored, but we finally got the announcement. In addition, the German high court didn't rule against Germany's participation in certain stability mechanisms. The combined effect of these two events was for the markets to breath a collective sign of relief and rally.

The German market was in an uptrend that started in early June. However, over the last week, prices have broken through upside resistance and are approaching 6 month highs. Note the volume spike that occurred a few days ago, along with the bullish MACD and CMF pictures. Finally, prices are now over the 200 day EMA, with the shorter EMAs all rising.

The Italian (top chart) and Spanish (bottom chart) markets both consolidated their losses over the summer and were meandering higher. Note how both stalled right below their respective 200 day EMAs at the end of August. However, the ECB announcement provided traders the ammunition they needed to rally the markets into bull market territory above the 200 day EMA. Note the rising MACD, and strengthening of prices.

The French market was already above the 200 day EMA and in an upward sloping channel. However, it's important to remember that the new French government is now trying to balance a budget and running into difficulty.

The US treasury market is moving sideways (top chart), trading between the high established after a long rally and lows from mid-August. However, the top chart shows us that prices are right at longer-term support. This is important considering that the Fed is about to (possibly) move into QEIII.

|

The Italian (top chart) and Spanish (bottom chart) markets both consolidated their losses over the summer and were meandering higher. Note how both stalled right below their respective 200 day EMAs at the end of August. However, the ECB announcement provided traders the ammunition they needed to rally the markets into bull market territory above the 200 day EMA. Note the rising MACD, and strengthening of prices.

The French market was already above the 200 day EMA and in an upward sloping channel. However, it's important to remember that the new French government is now trying to balance a budget and running into difficulty.

The US treasury market is moving sideways (top chart), trading between the high established after a long rally and lows from mid-August. However, the top chart shows us that prices are right at longer-term support. This is important considering that the Fed is about to (possibly) move into QEIII.

Wednesday, September 12, 2012

Dollar Breaks Key Support Line

On Monday, I noted that the euro had broken out of a key weekly channel. Today, I wanted to focus on the dollar, where the exact opposite is happening:

Starting last September, the dollar has benefited from a safe haven bid in the market. It's not that traders actually like the dollar; it's more that they dislike it the least. However, with the appearances that the euro is starting to settle into a true solution to their problem and with the Fed looking more and more likely to engage in QEIII, traders are selling off the dollar.

On the weekly chart, prices have moved through the upward sloping trend line started last September and are now at the lower Bollinger Band. Momentum is negative and prices are weakening.

There is a silver lining to this scenario. A cheaper dollar is better for US exports, which helps at a time when US manufacturing is slowing.

Starting last September, the dollar has benefited from a safe haven bid in the market. It's not that traders actually like the dollar; it's more that they dislike it the least. However, with the appearances that the euro is starting to settle into a true solution to their problem and with the Fed looking more and more likely to engage in QEIII, traders are selling off the dollar.

On the weekly chart, prices have moved through the upward sloping trend line started last September and are now at the lower Bollinger Band. Momentum is negative and prices are weakening.

There is a silver lining to this scenario. A cheaper dollar is better for US exports, which helps at a time when US manufacturing is slowing.

Morning Market Analysis; BRICs Not Helping

The Brazilian market bottomed at the end of May and has been meandering higher ever since. However, this is not a strong rally; prices are inching higher and are still below the 200 day EMA.

The Indian market also bottomed in May and has risen since. This rally is a bit stronger -- prices have advanced about 15%. However, prices are still below the 200 day EMA.

The Russian market is the strongest performer over the last three months of the BRICs. Prices have advanced about 23.5% and are now over the 200 day EMA.

The Chinese market is still stuck at levels seen at the end of May. Prices advanced to the 200 day EMA in early August and have since retreated.

Remember that the BRICs were the prime reason we got out of the recession as quickly as we did. China ramped up spending, which gave Brazil a market for their raw materials. India had stronger internal consumption but was also a source for outsourced service employees. Russia had oil to export.

India and Brazil are right below their respective 200 day EMAs, so they could make a move soon into bullish territory, following Russian's lead. But the Russian rally is probably tied to oil and anticipation of a higher price in oil rather than a robust economic breakout, leaving the other countries really holding the bag.

Tuesday, September 11, 2012

Bonddad Linkfest

- Obama 49, Romney 48 in poll (WaPo)

- Senate control up for grabs (NYT)

- Tough for Romney to keep the best of health care law while repealing the rest (NYT)

- Chinese CPI up 2% YOY in August (NBS)

- Chinese retail sales up 13% YOY (NBS)

- Real GDP up .3% M/O/M (South Korean Central Bank)

- Italian GDP down .8% M/O/M and 2.6% Y/O/Y

- US hiring plans holding steady (Marketwatch)

- Small caps and copper join break-outs (Marketwatch)

- Taking stock of US exports to Mexico (WaPo)

US-Mexico Trade Booming

From the Washington Post:

The growing middle class that is fast becoming Mexico’s majority is buying more U.S. goods than ever, while turning Mexico into a more democratic, dynamic and prosperous American ally.

“We are obsessed with China when we ought to seriously focus, for our own benefit, on our neighbor Mexico,” said Robert Pastor, a professor of international relations at American University and author of “The North American Idea.”

While news about headless torsos, drug barons and illegal immigration dominates the headlines, and much of the Obama administration agenda south of the border has focused on law enforcement, economists say another story is one of roaring trade.

“Not only is Mexico doing better, macroeconomically speaking, than the false stereotypes would have us think, Mexico is actually doing better than the United States,” said Richard Fisher, president of the Federal Reserve Bank of Dallas, who applauds Mexico for controlling inflation, balancing budgets and managing debt.

Read the whole article.

The growing middle class that is fast becoming Mexico’s majority is buying more U.S. goods than ever, while turning Mexico into a more democratic, dynamic and prosperous American ally.

“We are obsessed with China when we ought to seriously focus, for our own benefit, on our neighbor Mexico,” said Robert Pastor, a professor of international relations at American University and author of “The North American Idea.”

While news about headless torsos, drug barons and illegal immigration dominates the headlines, and much of the Obama administration agenda south of the border has focused on law enforcement, economists say another story is one of roaring trade.

“Not only is Mexico doing better, macroeconomically speaking, than the false stereotypes would have us think, Mexico is actually doing better than the United States,” said Richard Fisher, president of the Federal Reserve Bank of Dallas, who applauds Mexico for controlling inflation, balancing budgets and managing debt.

Read the whole article.

Copper Breaking Out

On the weekly chart, the copper ETF traded right about the 42 price level for a three months, while also consolidating in a triangle pattern. Over the last four weeks, prices have broken out and are now above the 200 week EMA.

On the daily chart, prices traded between 42 and 45. However, over the last two trading days, prices have spiked on strong volume and are now above the 200 day EMA.

Morning Market Analysis; Asia Consolidating

With China slowing down, we see the rest of the Asian markets consolidating gains on their long-term charts. Consider the following:

The Hong Kong market is consolidating between highs established last fall and lows established at the end of last year. The overall pattern is one of a a symmetrical triangle.

The Hong Kong market is consolidating between highs established last fall and lows established at the end of last year. The overall pattern is one of a a symmetrical triangle.

Malaysia is forming an ascending triangle pattern.

Singapore is forming an upward sloping channel

Both Taiwan and South Korea are forming symmetrical triangles.

Malaysia is forming an ascending triangle pattern.

Singapore is forming an upward sloping channel

Both Taiwan and South Korea are forming symmetrical triangles.

Monday, September 10, 2012

Bonddad Linkfest

- How climate change effects the power grid (WaPo)

- Romney agrees to keep key Obamacare provisions (WaPo)

- Everything people think they know about the stimulus is wrong (WaPo)

- Romney tax plan leaves key variables blank (NYT)

- Chinese exports drop 2.7% (FT)

- Chinese investment and industrial output move lower (FT)

- South Korea unveils $5.2 billion stimulus (FT)

Euro Breaks Out of Key Weekly Channel

The above chart is a weekly chart of the euro. The chart has been in a downward sloping channel for roughly the last year. Last week, prices broke through upside resistance, printing a strong bar on high weekly volume. This is an ideal example of a textbook breakout for a chart. It also signifies a fundamental change in the markets attitude toward the euro. For the last year, the EU has been a net drag on the overall trading environment for obvious reasons. However, last week's announcement by the ECB obviously provided a strong enough change of events for the currency markets to start taking net long positions in the euro.

The Fits and Starts Expansion Gets Stuck In The Mud

A little more than three years ago, I wrote a piece titled "the Fits and Starts Expansion" where I wrote the following:

First, the following has been my position regarding the expansion:

I basically argued that the economy would be moved by lower consumer spending (somewhere between 0%-2% year over year growth), Asian economies expanding, manufacturing ramping up, inventory adjustments, and stimulus spending. For the last three years, we've seen the above scenario pretty much play out.

The reason for this trip down economic memory lane is that we've been seeing the more or less same economic situation for the last year or so -- meandering growth that's very ill-defined and extremely lackluster. US unemployment has been stuck a little over 8% for the last year. GDP growth is incredibly uneven and at times barely positive. Our political system is dominated by two parties, the first of which completely embraces abject ignorance and stupidity ("raise your hand if you if you don't believe in evolution or global warming") as its central policy platform while the second continues to demonstrate a complete lack of leadership or any meaningful policy advances ("No, really, we have a platform and are going to implement it").

On this point, consider the following charts:

The year over year percentage change in real GDP has been fluctuating right around 2% for the last 7 quarters. So, yes, we're growing, but no, it's hardly exceptional growth. As a result,

the unemployment rate has been meandering lower for the last 2-3 years. Most importantly, it's been stuck at over 8% for the duration of this expansion.

The point I'm trying to make is that we're stuck in this slow growth environment and can't seem to get out. As a result, unemployment just isn't going to budge in any meaningful way.

First, the following has been my position regarding the expansion:

I am also on record as saying growth will be weak, printing somewhere in the 1% to 2% range with high unemployment. It's extremely important to remember where certain numbers were just recently. For example, an economy that loses over 600,000 jobs over a series of months is not going to print a positive jobs number for some time. That's simply the way an economy the size of the US's works. To expect otherwise is very unrealistic.The traditional view is for the expansion to "ramp up" from a slow bottom and then increase speed until the economy as a whole gets to maximum potential. In other words, ideally GDP will increase from 0% to 1% to 2% to 3% etc... I don't see that happening right now. That's why the next wave of the expansion will be the "fits and starts" expansion.

I basically argued that the economy would be moved by lower consumer spending (somewhere between 0%-2% year over year growth), Asian economies expanding, manufacturing ramping up, inventory adjustments, and stimulus spending. For the last three years, we've seen the above scenario pretty much play out.

The reason for this trip down economic memory lane is that we've been seeing the more or less same economic situation for the last year or so -- meandering growth that's very ill-defined and extremely lackluster. US unemployment has been stuck a little over 8% for the last year. GDP growth is incredibly uneven and at times barely positive. Our political system is dominated by two parties, the first of which completely embraces abject ignorance and stupidity ("raise your hand if you if you don't believe in evolution or global warming") as its central policy platform while the second continues to demonstrate a complete lack of leadership or any meaningful policy advances ("No, really, we have a platform and are going to implement it").

On this point, consider the following charts:

The year over year percentage change in real GDP has been fluctuating right around 2% for the last 7 quarters. So, yes, we're growing, but no, it's hardly exceptional growth. As a result,

the unemployment rate has been meandering lower for the last 2-3 years. Most importantly, it's been stuck at over 8% for the duration of this expansion.

The point I'm trying to make is that we're stuck in this slow growth environment and can't seem to get out. As a result, unemployment just isn't going to budge in any meaningful way.

Morning Market Analysis

There's good and bad news in the above charts of the major US averages. The IWMs show a strong move higher by printing two strong bars at the end of last week. As this market is really more of the risk based market, this is an encouraging sign. However, the QQQs (middle chart) didn't print any follow through and the SPYs (bottom chart) printed a weak bar on Friday. Considering the strength of the underlying technicals (rising CMFs and MACDs giving buy signals) these weaknesses aren't fatal, but they do mean the current rally is a bit suspect.

Gold has broken out to a new high with prices of the GLD ETF moving through two important areas of resistance (the first at the 158 level and the second at the 166 level). The reason for this is the EUs move into the bond market and the potential for the Fed to engage in QEIII -- both of which are raising inflation fears.

The weekly GLD chart shows the latest move. Prices have moved through resistance with the next logical price target at the 175 level. Also note the bullish CMF and MACD position; this chart has some room to run.

Oil rallied from a low in the high 70s at the end ot June to 97.5 in mid-August. Now prices are consolidating gaisn in the 95-97.5 area, using the 20 day EMA as technical support.

There are a few ways to look at the weekly oil chart. First, we have a high established in mid-2-11 and a low in the fall of 2011 with prices simply moving between those two points for the last year. You could also argue that price are in the middle of a triangle consolidation with an incomplete rally in progress.

Sunday, September 9, 2012

Three Very Scary Charts From the EU's Monthly Report

Every month, the ECB releases a report on the overall EU economy. In looking through the latest report, there are three charts that really jump out for their negative implications.

Overall monetary growth is incredibly weak and is at levels associated with recession.

Loans are not not being made -- and have not been made to many people for the duration of this expansion. Also note the overall negative reading of consumer credit for the last few years -- that is definitely not good.

Employment is clearly moving in the wrong direction.

Overall monetary growth is incredibly weak and is at levels associated with recession.

Employment is clearly moving in the wrong direction.

Obama should nationalize the Congressional elections

- by New Deal democrat

(Note: regular economic blogging will resume tomorrow)

The Democratic National Convention was a nearly flawless launch of Barack Obama's official re-election campaign. But it glossed over the first order problems of America's ever more squeezed middle/working class, and it's "invisible poor." On Friday Felix Salmon wrote an absolutely first-rate column about America's invisible poor. I've excerpted it below but you really should read the entire piece:

[T]here’s a very strong correlation between numeracy, or intelligence, or financial literacy, on the one hand, and having a solid financial footing, on the other.As Ezra Klein pointed out, also on Friday, that's exactly where Obama's acceptance speech fell short:

.... Financially literate people are more likely to plan for retirement. And if you plan for retirement, [studies show] you have more wealth .... And similarly, at the other end of the spectrum, there’s huge amounts of research showing that if you’re particularly financially illiterate, or you’re not good at numbers, then you’re much more likely to be ripped off by predatory lenders or other scams, be they legal or otherwise.

There are various conclusions to be drawn here, one of which is that if we do a better job of financial education, then Americans as a whole will be better off. That’s true. But at the same time, financial illiteracy, and general innumeracy, and low IQs, are all perfectly common things which are never going to go away. It’s idiotic to try to blame people for having a low IQ: that’s not something people can control. And so it stands to reason that any fair society should look after people who are at such a natural disadvantage in life. [NDD note: my emphasis]

.... [T]he number of Americans lifted out of poverty has been shamefully low for basically all this century. ....

It seems to me that the current election campaign comes down in large part to a simple question: “who do you care about”? Do you care about the ... “job creators” ... [o]r do you care about ... the people who have been left behind by US economic policy and who desperately need help and support? The Republicans clearly are the party of the 1%, and the Democrats are trying to paint themselves as the party of the middle class — of the 59%, you might say. But no one is standing up for the bottom 40%, the invisible poor ....

Obama’s speech Thursday night took place in a world where the jobs crisis didn’t exist. It’s not that he didn’t talk about jobs. But there was no particular urgency in his diagnosis, much less in his prescription. The mentions of the unusual severity of the situation were glancing and the proposals mostly unresponsive. The speech would have been as appropriate for an economy at 6.5 percent unemployment as 8.1 percent unemployment.The choice of Bill Clinton to nominate Obama speaks volumes. It seems like Obama has abandoned his original goal of surpassing Clinton and becoming a Great President, and is willing to settle for being heir to Clinton's legacy, provided it gets him re-elected. As part of that racheting down, the large goals of more equal economic opportunity and fairness toward the under- and unemployed invisible working class and poor have been mooted.

.... Into this ocean of grim news, the president flung a handful of policy prescriptions that wouldn’t do anything much anytime soon. Plans to boost natural gas production, to recruit new math and science teachers, to make college more affordable, and to boost exports might help us create jobs in the coming years, but they won’t ease the pain for the unemployed in the coming months.

But then, those policy prescriptions weren’t meant to solve the jobs crisis.... they’re about upgrading the skills of American workers and fostering new, high-paying industries. The problem — as the official admitted — is that the project of the first term is not over. Our ongoing jobs crisis has not yet ended.

The administration is not without answers. The American Jobs Act is a serious, real policy proposal that would boost the labor market right now. Private forecasters estimate that it would add around 2 million new jobs over the next two years. In stark contrast to the policies outlined last night, which would be as appropriate in 2005 or 1995 as they are today, the American Jobs Act is actually designed for jobs crisis we’re in, and wouldn’t make much sense in more normal times.

And yet, insofar as the president mentioned it, it was only a glancing, opaque reference. ... White House officials ... [have] made a decision, presumably because they think it’s better politics, to refrain from reminding voters how bad things are and to resist using the campaign as an opportunity to continue pushing emergency measures that congressional Republicans implacably oppose. [NDD note: my emphasis]

Indeed, once upon a time, Obama is reputed to have said that he would rather not be re-elected then fail to enact policies he deemed essential. Now it is said that he will work with Republicans where possible, but work around them when they are obstructive. That political calculation assumes that he must continue to work with an intransigent GOP majority in the House and possibly even in the Senate.

I contend that there is another alternative. If Obama is able to nationalize the Congressional elections as a referendum on the "do-nothing" Tea Party GOP Congress, even if he believes it carries some risk to his own personal success, he may be richly rewarded with Democratic majorities in both Houses of Congress -- who will be indebted to him for their victories. He can then work with friendly collaborators to enact the long-term policies he values so highly -- and those policies will be much more palatable than the ones that would have to gain support from the Congressional GOP.

Wishful thinking on my part? Hardly. In 1948, when he ran against the "do-nothing" GOP Congress that ignored all his initiatives, Harry Truman didn't just secure his own, surprising, re-election. The Democrats also picked up 7 seats in the Senate and 75 seats in the House of Representatives, obtaining Democratic majorities in both.

Is this election just about re-electing Barack Obama, or is it more? If it is also about addressing the long-suffering American working class and the Invisible Poor, it's worth the effort and the chance to make a major theme of this election the defeat of the GOP hostage-taking, do-nothing Congress.

Subscribe to:

Posts (Atom)