It’s been a blissfully long time since John Hinderaker of Powerline has written about economics. I believe we can thank the presidential election for that. He broke his long silence earlier this week with his post Economists for Clinton. I’m sure most of his readers believe he brilliantly skewered the work of Mark Zandi. But to anyone who is even slightly familiar with economics, it once again conclusively demonstrated that Mr. Hinderaker is an economic idiot.

First, let’s understand the parties involved. The Powerline blog contains the following biography of Mr. Hinderaker:

John H. Hinderaker practiced law for 41 years, enjoying a nationwide litigation practice. He retired from the practice of law at the end of 2015, and is now President of Center of the American Experiment, a think tank headquartered in Minnesota.

Mr. Hinderaker lives with his family in Apple Valley, Minnesota. He is a graduate of Dartmouth College and Harvard Law School. During his career as a lawyer, he was named one of the top commercial litigators and one of the 100 best lawyers in Minnesota, and was voted by his peers one of the most respected lawyers in that state. He was repeatedly listed in The Best Lawyers in America and was recognized as Minnesota’s Super Lawyer of the Year for 2005.

Mr. Hinderaker is an Ivy League educated litigator who had a successful courtroom practice. Curiously absent is any mention of economics. That’s because, even if he took courses in college, it wasn’t part of what he did for a living. Instead, he went to court.

This is a very different background that Mr. Zandi’s. The following is from his Moody’s page:

Mark M. Zandi is chief economist of Moody’s Analytics, where he directs economic research. Moody’s Analytics, a subsidiary of Moody’s Corp., is a leading provider of economic research, data and analytical tools. Dr. Zandi is a cofounder of the company Economy.com, which Moody’s purchased in 2005.

Dr. Zandi’s broad research interests encompass macroeconomics, financial markets and public policy. His recent research has focused on mortgage finance reform and the determinants of mortgage foreclosure and personal bankruptcy. He has analyzed the economic impact of various tax and government spending policies and assessed the appropriate monetary policy response to bubbles in asset markets.

.....

Dr. Zandi conducts regular briefings on the economy for corporate boards, trade associations and

policymakers at all levels. He is on the board of directors of MGIC, the nation’s largest private mortgage insurance company, and The Reinvestment Fund, a large CDFI that makes investments in disadvantaged neighborhoods. He is often quoted in national and global publications and interviewed by major news media outlets, and is a frequent guest on CNBC, NPR, Meet the Press, CNN, and various other national networks and news programs.

.....

Dr. Zandi earned his B.S. from the Wharton School at the University of Pennsylvania and his PhD at the University of Pennsylvania. He lives with his wife and three children in the suburbs of Philadelphia.

Dr. Zandi is also Ivy League educated, but he has a doctorate in economics. His Moody’s page has a link to a large number of testimonies, studies and writings on the economy. Using the Daubert standard (which I’m sure Mr. Hinderaker is more than a little familiar with), any court would accept Mr. Zandi’s testimony as that of an expert in economics. Mr. Hinderaker’s … not so much.

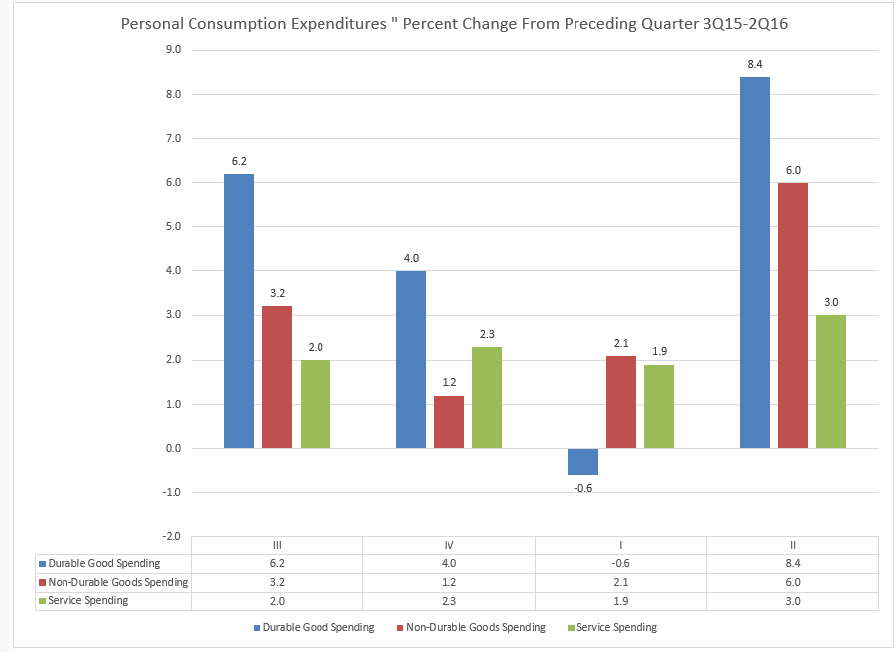

Let’s turn to Mr. Hinderaker’s “analysis,” where he first tries to discredit Dr. Zandi by referencing his work on the 2009 stimulus. Conservatives love to post the following chart, which shows the then hoped path unemployment would take as a result of the 2009 spending package.

But the problem with the stimulus was that it was too small as demonstrated by Dean Baker and Paul Krugman (both would also easily pass the Daubert test). Both used basic math to illustrate their points.

Next, Hinderaker makes the following unsubstantiated assertion:

Later versions of the same chart traced the ongoing failure of the “stimulus” to perform anywhere near the level that was promised by Obama’s economists and, apparently, Mr. Zandi. Perhaps Mr. Zandi still believes in the magical “multiplier effect” that was in vogue in the 1960s, and somehow transformed government spending into a growth vehicle exceeding all others. Most economists wised up long ago.

Perhaps Mr. Hinderaker should read the 2013 paper, Growth Forecast Errors and Multipliers, published by the IMF, which reached the exact opposite conclusion:

This paper investigates the relation between growth forecast errors and planned fiscal consolidation during the crisis. We find that, in advanced economies, stronger planned fiscal consolidation has been associated with lower growth than expected, with the relation being particularly strong, both statistically and economically, early in the crisis. A natural interpretation is that fiscal multipliers were substantially higher than implicitly assumed by forecasters. The weaker relation in more recent years may reflect in part learning by forecasters and in part smaller multipliers than in the early years of the crisis.

Or perhaps he should read the section on Multiplier Models in the 10th edition of Paul Samuelson’s textbook Economics. Either way, he’ll learn that his basic assertion is 100% wrong.

Mr. Hinderaker has no business writing about economics. He’s a slightly above-average political commentator who has a long and documented history of reaching the exact wrong economic conclusion. As I’ve documented, Powerlines’ entire economic analysis for 2014 was 100% wrong. This won’t stop him, of course. Because while he’s been fundamentally wrong he also has the litigators ego, which means he won’t admit to his being this bad.