Saturday, August 15, 2015

Weekly Indicators for August 10 -14 at XE.com

- by New Deal democrat

My weekly indicator post is up at XE.com. Needless to say, the biggest issue has to do with the revaluation of the Yuan.

Friday, August 14, 2015

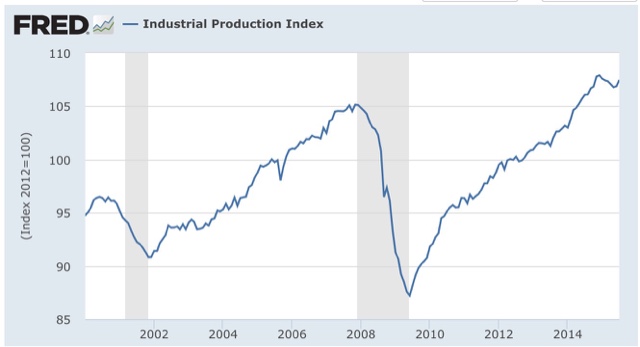

July industrial production: a solid start to Q3

- by New Deal democrat

Like retail sales earlier this week, industrial production rose strongly, also mainly on the back of motor vehicles.

The overall index is still just shy of its all-time high set last autumn:

Below are the three main component groups - manufacturing, mining, and utilities:

Manufacturing is the largest sector, so the big increase there overwhelmed the decrease in utilities. Mining, of course, has suffered as part of the Oil patch, but had a little rebound in July.

Industrial production is basically the King of Coincident Indicators. The NBER historically has almost always dated the beginning and end of recessions as of the date industrial production turns. To put this in a longer term context, as shown in the below graph, the recent downturn wasn't enough to set off recession alarm bells:

Not a perfect report, but a solid one. The pessimists will point out how much the increase relies on autos, and seasonal issues with retooling, but since motor vehicles are the second most important sector after housing, the increase remains real and important. This with retail sales earlier this week and the employment report last week have gotten the 3rd Quarter off to a good start.

I hereby volunteer

- by New Deal democrat

So, no sooner do I tell you that there is no point to my reporting on daily economic statistics, because I am going to agree with Bill McBride, a/k/a Calculated Risk, 90% of the time, than the bastard goes and takes a 10-day vacation.

On top of that, Hale Stewart, the alleged proprietor of this here blog, also went on vacation and didn't even bother to tell me! I think I am going to change the name of the blog and see how long it takes him to notice.

Well, since *somebody* has to stay behind and keep the internet turned on, I suppose I have no choice but to report for duty. Hopefully industrial production, housing permits, and CPI won't blow up the place while I am watching them. < / sigh >

Thursday, August 13, 2015

More evidence we are past the midpoint for jobs growth

- by New Deal democrat

Yesterday's JOLTS report adds to the evidence that this expansion is past its midpoint and that the expansion of jobs is heading towards maturity.

In the last expansion, the only one for which JOLTS provides complete data, hiring stalled out for over a year while job openings continued to grow:

A close-up of the last year shows that for the last 9 months, the same thing has happened.

Similarly, layoffs and discharges bottomed out shortly after hiring stalled:

A close-up of the last year shows a bottom in layoffs and discharges last November, one months before the peak in hiring to date.

Further, as I noted on Tuesday, a weakening of the Labor Market Conditions Index tends to lead a decline in YoY jobs growth by about 6 - 12 months:

That is further evidence that we should expect less YoY growth in jobs for the remainder of this year as compared with 2014.

Finally, unsurprisingly housing permits lead jobs growth as well:

While a steep decline to a stall in housing, as happened in 2014, has not always led to a stall in jobs, usually it has led to at least some weakening, sometimes slight, sometimes very marked. Since the lead time varies between 6 to 18 months, we are about due for last year's weakness in housing to lead to some weakness in payrolls.

What would lead to a positive reboot in jobs growth? A decline towards new lows in mortgage rates. Failing that, we are in the latter stage of the jobs expansion.

Wednesday, August 12, 2015

Why there is no "second housing bubble"

- by New Deal democrat

I have a new post up at XE.com, explaining why I reject the idea that housing has entered a second "bubble."

Tuesday, August 11, 2015

The Labor Market Conditions Index as a leading indicator

- by New Deal democrat

Via Naked Capitalism, Bill Mitchell writes that the Fed's "Labor Market Conditions Index is Weakening." As usual, I hate the present progressive tense, since there is nothing about the index that forecasts what it itself will do over the coming months. Further, since it is still positive, labor market conditions are still above trend - just much less so than last year. But the Index itself turns out to be a useful addition to the forecasting toolbox.

The LMCI is based on 19 components. Click on the link above if you want further information on its makeup. What is important to me is that it has a 40 year history of signaling a turn in the economy.

Here is the entire history of the index:

Here's what the data behind the Index shows: (1) the index has with one exception (1981's double-dip) always failed to make a new high for at least 12 months before the next recession, sometimes much longer than that; and (2) the index has always dropped below 0 and stayed negative for 6 months or somewhat more before the onset of the next recession.

Here is the Index over the last 5 years:

The Index made its cycle high at the beginning of 2012. It made a secondary high in early 2014. But it has not turned consistently negative.

The Index become more valuable when it is teamed with two other measures: the YoY% growth in nonfarm payrolls, and interest rates.

As shown in the graph below, the LMCI consistently leads the YoY% growth in jobs by 6 - 12 months, but YoY job growth (red) is a much smoother measure:

Thus job growth serves as an important confirmation for the long leading part of the Index.

But a downturn below 0 in the LCMI, even partnered with a downturn in the growth of YoY jobs, hasn't always meant recession, as in the 1980s and 1990s. That's where interest rates come into play. In the 1980s and 1990s, as shown in the graph below (green), a marked increase in interest rates led to the declines in both the LMCI and YoY job growth.

When that upturn in interest rates abated, the LMCI, and jobs, came back. It was only when both weakened to the point where the LMCI was consistently negative, before interest rates declined, that a recession ensured.

Here is the same information for the period 2000 - present:

While the "taper tantrum" in interest rates briefly put a dent in the LMCI and YoY job growth, interest rates have calmed down since. In other words, more confirmation that we are probably past mid-cycle, but no imminent threat of an actual downturn.

On the negative side, since the LMCI does lead the much smoother YoY growth in jobs, it strongly suggests that YoY payroll growth is going to decline over the next 6 months or so. And that can only happen if those payroll numbers generally come in under 225,000, and probably even below 200,000 through next winter.

All in all, the LMCI is a useful addition to the forecasting toolbox.

Monday, August 10, 2015

Forecasting the 2016 election economy: what are the best metrics?

- by New Deal democrat

How well do economic conditions predict the outcome of Presidential elections? Can we forecast the most important of those conditions in advance? If so, what can we say even now about 2016?

That's what I am examining in this series, Forecasting the 2016 Election Economy.

Fortunately, I don't have to start from scratch. As I noted in my inaugural post, most significantly, in 2011, Nate Silver undertook an examination of 43 economic variables, and their potency in predicting the election outcomes, going back all the way to the 1950s. Additionally, James Surowiecki has suggested that growth in real personal income in Q2 of the election year is the most determinative economic fact. Also, Professor of Economics Douglas Hibbs has used what he calls:

I'll look at that model, which has a generally good record, but missed badly in 2000 and 2012, in a later post.

In this post, I still start by looking at 5 of the variables identified by Nate Silver as being the most dispositive. To cut to the chase, in order of their predictive importance, here's the top 20 variables he found most predictive of election results, in order of their value:

Below, I have taken those 5 indicators, and charted them all the way back to the 1952 election, or the start of the series when applicable, as to their YoY change (q/q change for ISM) during Q2 and Q3 of each election year. All of these are adjusted for inflation when relevant:

For reasons of space limitation, for now I omitted the series for real GDP, real final sales, real aggregate payroll growth, and real disposable personal income per capita.

The top 5 variables identified by Silver mostly give me the same result: if they were consistent, Humphrey would have won in 1968, and Ford in 1976. Both Humphrey and Ford had objectively great economic numbers to run on. Further, while poor economic performace as in 1980 and 2008 are a death sentence for the incumbent party, mediocre numbers are less dispositive. If they were, Clinton in 1992, Bush in 2004, and Obama in 2012, all would have lost.

That being said, the single variable with the best record is the change in the unemployment rate. It has correctly forceast 13 of the 15 elections since 1956. If the unemployment rate is rising in Q2 and Q3 of the election year, the incumbent party is going to lose. If it is declining, with two exceptions, (Humphrey in 1968, Gore in 2000) the incumbent party is going to win.

Meanwhile, Surowiecki's measure of real personal income calls for Clinton and Obama to lose their re-election bids, and also misses 1968 and 1976.

How well do economic conditions predict the outcome of Presidential elections? Can we forecast the most important of those conditions in advance? If so, what can we say even now about 2016?

That's what I am examining in this series, Forecasting the 2016 Election Economy.

Fortunately, I don't have to start from scratch. As I noted in my inaugural post, most significantly, in 2011, Nate Silver undertook an examination of 43 economic variables, and their potency in predicting the election outcomes, going back all the way to the 1950s. Additionally, James Surowiecki has suggested that growth in real personal income in Q2 of the election year is the most determinative economic fact. Also, Professor of Economics Douglas Hibbs has used what he calls:

... the Bread and Peace model to explain presidential voting outcomes. The model claims that just two fundamental variables systematically affected post-war aggregate votes for president: (1) weighted-average growth of per capita real disposable personal income over the term, and (2) cumulative US military fatalities due to unprovoked, hostile deployments of American armed forces in foreign wars.

In this post, I still start by looking at 5 of the variables identified by Nate Silver as being the most dispositive. To cut to the chase, in order of their predictive importance, here's the top 20 variables he found most predictive of election results, in order of their value:

Below, I have taken those 5 indicators, and charted them all the way back to the 1952 election, or the start of the series when applicable, as to their YoY change (q/q change for ISM) during Q2 and Q3 of each election year. All of these are adjusted for inflation when relevant:

| Y ear | ISM Mfg | Change Nonfarm payrolls | Change unemplymt rate | Real personal income | Change Emp/Pop ratio |

|---|---|---|---|---|---|

| 1956 | 1.0/0.4 | 3.9/2.5 | -0.2/0.0 | 5.6/4.1 | 1.2/0.5 |

| 1960 | -5.9/-4.4 | 1.9/1.4 | 0.1/0.2 | 2.9/3.2 | 0.1/0.1 |

| 1964 | 9.3/13.2 | 2.6/3.0 | -0.5/-0.5 | 5.8/6.4 | 6.1/5.5 |

| 1968 | 5.6/2.9 | 3.2/3.4 | -0.2/-0.3 | 5.1/5.5 | 0.8/0.3 |

| 1972 | 9.8/12.3 | 3.2/4.3 | -0.2/-0.4 | 5.1/6.3 | 0.4/0.6 |

| 1976 | 9.2/4.7 | 3.6/3.2 | -1.3/-0.8 | 4.5/4.3 | 1.6/1.2 |

| 1980 | -17.6/-6.5 | 0.8/-0.3 | 1.6/1.8 | -0.7/-0.8 | -0.1/-0.8 |

| 1984 | 9.2/3.0 | 5.0/4.9 | -2.7/-2.0 | 7.7/8.3 | 2.7/1.9 |

| 1988 | 6.9/6.2 | 3.2/3.2 | -0.8/-0.5 | 4.5/0.5 | 0.8/0.7 |

| 1992 | 4.0/2.3 | 0.3/0.6 | 0.6/0.7 | 3.2/3.3 | -0.4/-0.2 |

| 1996 | 0.7/0.8 | 2.0/2.2 | -0.2/-0.4 | 4.3/4.4 | 0.3/0.7 |

| 2000 | 3.1/0.7 | 2.5/2.1 | -0.4/-0.2 | 6.1/6.5 | 0.2/-0.1 |

| 2004 | 10.8/8.6 | 1.1/1.5 | -0.5/-0.7 | 0.2/3.5 | 0.0/0/4 |

| 2008 | -0.9/-13.8 | -0.1/-0.7 | 0.8/1.3 | -0.3/-1.2 | -0.5/-0.9 |

| 2012 | 3.0/0.9 | 1.7/1.6 | -0.9/-1.0 | 3.7/3.8 | 0.6/0.7 |

For reasons of space limitation, for now I omitted the series for real GDP, real final sales, real aggregate payroll growth, and real disposable personal income per capita.

The top 5 variables identified by Silver mostly give me the same result: if they were consistent, Humphrey would have won in 1968, and Ford in 1976. Both Humphrey and Ford had objectively great economic numbers to run on. Further, while poor economic performace as in 1980 and 2008 are a death sentence for the incumbent party, mediocre numbers are less dispositive. If they were, Clinton in 1992, Bush in 2004, and Obama in 2012, all would have lost.

That being said, the single variable with the best record is the change in the unemployment rate. It has correctly forceast 13 of the 15 elections since 1956. If the unemployment rate is rising in Q2 and Q3 of the election year, the incumbent party is going to lose. If it is declining, with two exceptions, (Humphrey in 1968, Gore in 2000) the incumbent party is going to win.

Meanwhile, Surowiecki's measure of real personal income calls for Clinton and Obama to lose their re-election bids, and also misses 1968 and 1976.

Note that when a trend has markedly accelerating or decelerating during the election year, the voters have reacted to that. In 2000, it was clear by the end of Q3 that the economy was decelerating markedly. The reverse was true in 2004.

Looking at Silver's most valuable indicators, in general good growth will lead to re-election of the incomumbent, and usually re-election of the incombent party. A downturn, unsurprisingly, results in the incoumbent or their party being ousted. Mediocre growth leads to more incomsistent results, although the change in the unemployment rate stands out as having the most promise.

That being said, none of even the best economic variables have an infallible record. The economiy is not always the dominant issue in an election. For lack of a better word, the economy can be trumped by "moral" issues -- winning or losing a war, a big increase or decrease in crime, Watergate and the Nixon pardon, The Most Expensive Blow Job in History, and even in 2004 the spectre of gay marriage.

In my next post, I will look at one of the long leading economic indicators, and what it can already tell us about employment and unemployment next year.

Sunday, August 9, 2015

Value added

- by New Deal democrat

Why should you read me?

After all, there are about a bazillion economic commentators out there, a significant number of whom feel obligated to give their take on the latest statistics. As far as I am concerned, for reasoned commentary on daily statistics, 90% of the time you could read Bill McBride a/k/a Calculated Risk, and Doug Short (maybe the most informative graphs in the entire econoblogosphere), and just stop there. There's no point in my feeling the need to add my $.02.

So what is it that I bring to the table? Fitting the data into the business cycle.

I know of nobody else in the econoblogosphere who so relentlessly parses the economic data into long and short leading indicators, coincident indicators, short and long lagging indicators, and midcycle indicators -- and backs up the categorizations with as much historical data as possible, sometimes going back an entire century.

I know of nobody else in the econoblogosphere who so relentlessly parses the economic data into long and short leading indicators, coincident indicators, short and long lagging indicators, and midcycle indicators -- and backs up the categorizations with as much historical data as possible, sometimes going back an entire century.

So when I read somewhere that, e.g., employment will drive consumer spending, or housing, I already know that the historical data shows exactly the reverse: housing drives employment with a 12 month or more lag; consumer spending drives employment with a much shorter lag. I know that, over the longer term, corporate profits lead stock prices, not the other way around. I know that bank lending only turns up once an expansion has started. I know that the trend in hiring, whether up or down, slows and then turns first in comparison with the trend in firing. And so on.

In short, I see myself as the ECRI (Economic Cycle Research Institute) for those who don't have the $64,000 (last I heard) annual subscription fee to spare.

And I am particularly focused on how that data will play out in the lives of ordinary workers. A modern industrial democratic society ought to be improving the lot of the vast majority of its people. If it's not. something is seriously amiss.

A side effect of my focus is that unlike most observers, I do not fall prey to the fallacy of projecting the present trend into the future. In November 2006 I forecast the last recession being 1 year ahead. In January 2009 I forecast that the bottom of the Great Recession was likely to be that summer. For the last 6 years, with various amounts of waxing and waning, I have been bullish on the economy, and relentlessly eviscerating Doomers. I still am bullish.

Now more and more of the midcycle indicators have appeared to hit their inflection points. That just means the numbers underlying the expansion will remain positive but in general be gradually less so as time goes on.

Just remember, when the time comes - and it hasn't yet and may not for quite a while - that I yellow-flag the next recession, all of the coincident numbers like industrial production and employment will still be quite positive. You will think I have gone over to the Dark Side. I won't. I will simply be "skating to where the puck will be," in the words of hockey great Wayne Gretsky. That's why you read me.

Subscribe to:

Posts (Atom)