First, in talking about the current account as a percentage of GDP, it's important to understand what we're talking about. From the Economists' Economics Dictionary:

The total of all the money coming into a country from abroad less all of the money going out of the country during the same period. This is usually broken down into the current account and the capital account. The current account includes:

*visible trade (known as merchandise trade in the United States), which is the value of exports and imports of physical goods;

*invisible trade, which is receipts and payments for services, such as banking or advertising, and other intangible goods, such as copyrights, as well as cross-border dividend and interest payments;

*private transfers, such as money sent home by expatriate workers;

*official transfers, such as international aid.

The capital account includes:

*long-term capital flows, such as money invested in foreign firms, and profits made by selling those investments and bringing the money home;

*short-term capital flows, such as money invested in foreign currencies by international speculators, and funds moved around the world for business purposes by multinational companies. These short-term flows can lead to sharp movements in exchange rates, which bear little relation to what currencies should be worth judging by fundamental measures of value such as purchasing power parity.

What's important to remember is that all of these totals eventually have to balance out -- that is, if one country is a net importer than other countries have to be net exporters, with the grand total eventually hitting 0.

Let's start with the big net importers:

The US is obviously the world's largest importer. However, notice that this number has weakened over the last two years in the aftermath of the recession.

The UK is also a large importer. While their imports have not risen to the GDP level of the US, they are still high.

The EU and Brazil have bounced between net importer and exporter over the last 10 years.

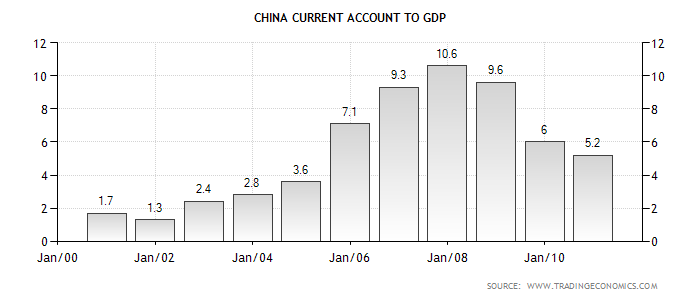

The exporting juggernauts of the top 10 world economies are Japan and China, both of whom who have modeled their economies to become net exporters. Overall, their respective philosophies can be partially characterized as mercantilist, which is defined thusly:

Mercantilism is the economic doctrine in which government control of foreign trade is of paramount importance for ensuring the prosperity and military security of the state. In particular, it demands a positive balance of trade. Mercantilism dominated Western European economic policy and discourse from the 16th to late-18th centuries.[1] Mercantilism was a cause of frequent European wars in that time and motivated colonial expansion. Mercantilist theory varied in sophistication from one writer to another and evolved over time. Favors for powerful interests were often defended with mercantilist reasoning.

.....

Neomercantilism is a 20th century economic policy that uses the ideas and methods of neoclassical economics. The new mercantilism has different goals and focuses on more rapid economic growth based on advanced technology. It promotes such policies as substitution state taxing, subsidizing, spending, and general regulatory powers for tariffs and quotas, and protection through the formation of supranational trading blocs

What started me on this thought process was the following chart from the Free Exchange Blog:

When we think about the entire global balance system, it's easy to start thinking in the US/China/EU paradigm, while forgetting about the importance and overall impact of the oil exporting countries. It's the oil exporters who, by far, have the strongest current account position; money literally flows into these countries on a daily basis, leaving them with the big question: what do we do with all of this money?

FIRST, the good news: China, the country at the centre of the debate about global imbalances, has a current-account surplus that has fallen sharply over the past few years. Now the bad: China was never really the prime culprit when it comes to imbalances at the global level. The biggest counterpart to America’s current-account deficit is the combined surplus of oil-exporting economies, which have enjoyed a huge windfall from high oil prices (see left-hand chart). This year the IMF expects them to run a record surplus of $740 billion, three-fifths of which will come from the Middle East. That will dwarf China’s expected surplus of $180 billion. Since 2000 the cumulative surpluses of oil exporters have come to over $4 trillion, twice as much as that of China.

One reason why this enormous stash has received much less attention than China’s is that only a fraction of it has gone into official reserves. Most of it is in opaque government investment funds. Middle Eastern purchases of Treasury bonds are often channelled through intermediaries in London, hiding their true ownership. A lot of money has been invested in equities, hedge funds, private equity and property, where ownership is harder to track. Oil exporters’ surpluses are also proving much more durable than those accumulated after previous oil-price shocks. This is partly because the tightness of oil supplies has kept prices high, and partly because oil exporters have spent less of their windfalls on imports than in previous booms.

Perhaps a better way to think of global trade flows is that the world is divided between oil importers and oil exporters.