- by New Deal democrat

As I wrote last week in discussing existing home sales at XE.com, the housing market tends to cycle in a regular order:

- 1st, interest rates turn

- 2nd, permits, starts, and sales turn

- 3rd, prices turn

- 4th, inventory turns

Now that we are half the way through 2014, let's look at where each of those points in the cycle stands.

Interest rates

First, here is a graph, covering the last 30 years, of the YoY% mortgage rates (inverted so that higher rates give a lower value, blue) vs. housing permits, YoY change in 100,000's (red):

Interest rates on mortgages went up about 1.4% between May and July of last year. On 16 of 19 occasions since the end of World War 2, that big a change led to a YoY decline of at least -100,000 in permits. In this case, housing permits have gone sideways, with small YoY% declines in several months, including May, since the beginning of this year.

In May mortgage rates equalled their lowest in almost a year. Since that appears to have had a big effect on housing activity in May, here is a close-up of the last five years of the YoY% change in permits (red, left scale) and rates for a 30 year mortgage (blue, right scale):

As you can see, these generally are mirror images of one another.

I suspect the situation this year is analogous to the late 1960's, when Boomers first reached adulthood and the existing aparment stock was nowhere near adequate to the task. Multi-unit starts skyrocketed, despite higher interest rates, while single family homes languished. It was an era of generally rising interest rates, and any temporary decline was met with heightened housing activity.

Interest rates

First, here is a graph, covering the last 30 years, of the YoY% mortgage rates (inverted so that higher rates give a lower value, blue) vs. housing permits, YoY change in 100,000's (red):

Interest rates on mortgages went up about 1.4% between May and July of last year. On 16 of 19 occasions since the end of World War 2, that big a change led to a YoY decline of at least -100,000 in permits. In this case, housing permits have gone sideways, with small YoY% declines in several months, including May, since the beginning of this year.

In May mortgage rates equalled their lowest in almost a year. Since that appears to have had a big effect on housing activity in May, here is a close-up of the last five years of the YoY% change in permits (red, left scale) and rates for a 30 year mortgage (blue, right scale):

As you can see, these generally are mirror images of one another.

I suspect the situation this year is analogous to the late 1960's, when Boomers first reached adulthood and the existing aparment stock was nowhere near adequate to the task. Multi-unit starts skyrocketed, despite higher interest rates, while single family homes languished. It was an era of generally rising interest rates, and any temporary decline was met with heightened housing activity.

Permits, starts, and sales

Second, here is a graph of the change, in thousands, YoY of starts (blue), permits (red), new home sales (green), and existing home sales (orange) (note that the St. Louis FRED does not track pending home sales):

Both of these graphs show the clear deceleration in the housing market through 2013 and through March 2014. Whether the spike in starts and new home sales in April and May means the trend has bottomed, or whether these are payback for particularly bad winter season reports, remains to be seen.

This morning we got the final report, pending home sales, which surged by +6.1% in May compared with April, but was still down -5.2% YoY.

More specifically, through May 2014:

- Permits are down -7% from their October 2013 high

- Starts are down -9% from their November 2013 high

- New home sales just blew past their previous June 2013 high

- Existing home sales are down -5% from their July 2013 high

- Pending home sales are down -7% from their June 2013 high

As I wrote last week, May new home sales were as big an outlier to the upside as March was originally reported to the downside. March was subsequently revised about 10% higher. So we should be mindful of revisions, and I think the best way to look at the number is to average March through May, which combined are only about 1% higher YoY.

Today's pending home sales report also adds unusually useful information. In the late 1960s and 1970s, the era of rising interest rates, buyers would pick and choose when to buy, and would pounce whenever there was a meaningful, if short term, did in rates. In May of this year, mortgage rates got as low as 4.12%, the lowest since June 2013 but for one week in October. Since pending sales are based on contract signings, it is likely that buyers jumped in response to these low rates.

Further, just as in the late 1960's, when Boomers first entered the market, now it is Millennials. Now as then, it is only multi-unit (apartment) construction that is carrying the recovery in housing this year. Single family home starts and sales have completely stalled. Here is a graph of single family permits (blue) compared with 5 unit or higher permits (red) since January 2013:

It is easy to see that it is multiunit construction, especially beginning in the second half of 2013, that is entirely responsible for any continuing increase in residential construction. Single family home construction and sales have gone essentially nowhere since the beginning of 2013.

Prices

Prices continue to increase, but YoY the price gains are decelerating, and in the case of existing home sales the non-seasonally adjusted data shows May 2014 prices below June and July 2013 prices. So let's start by showing the YoY% change in median prices in the Case Shiller 20 city index:

The YoY% change in median prices for new homes (red) and existing homes (blue): shows the same deceleration:

Finally, it is worth noting that the same deceleration is also showing up in the data at Depatment of Numbers Housing Tracker. I used this database of asking prices, which is updated weekly, to call in real time both the top of the housing boom in 2006, and the bottom of the housing bust in 2012. What is particularly noteworthy is that in 2006, it was the asking prices for houses in the 75th percentile (more expensive homes) which turned first. Now prices for those same more expensive houses are showing the most deceleration of all, as shown in this table, which shows the YoY% change for each percentile of houses for sale nationwide:

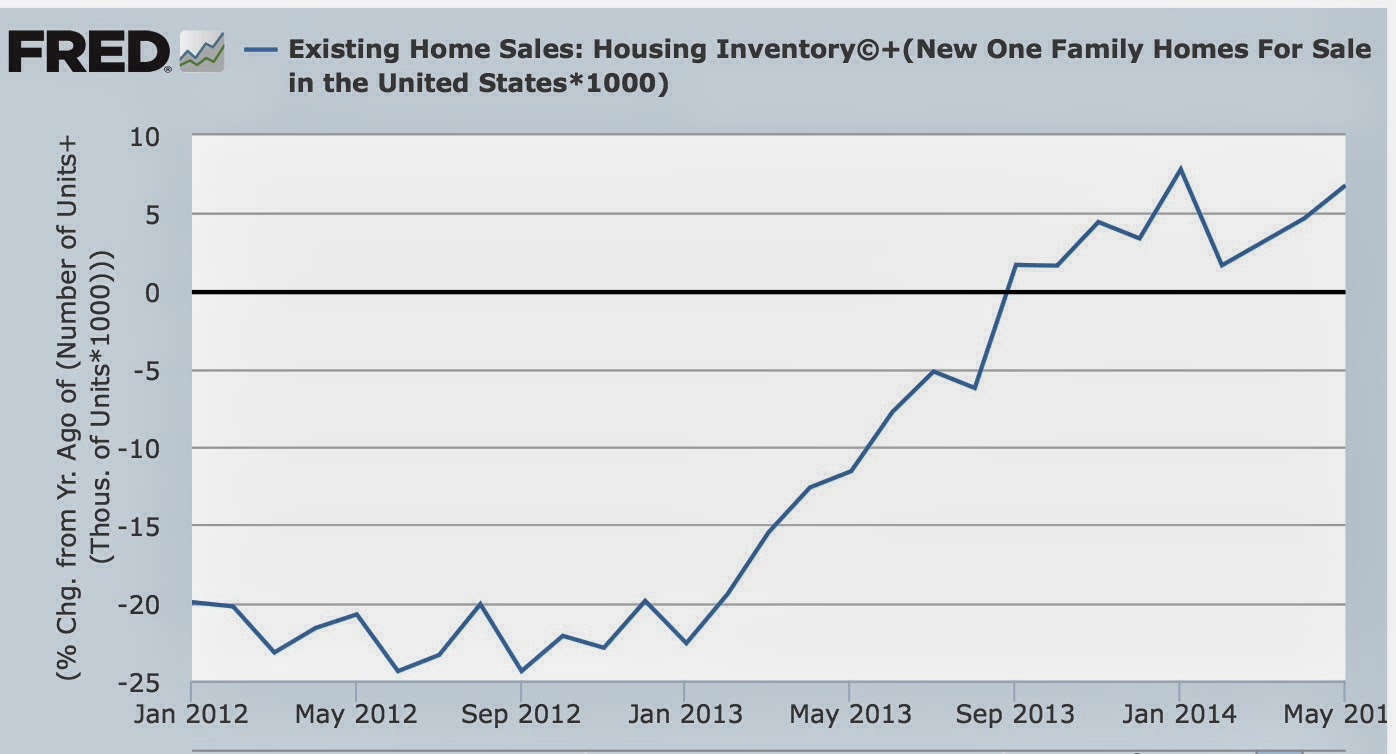

Inventory

With housing prices still increasing, albeit at a reduced rate, we would expect to find more inventory entering the market, as potential sellers hope to take advantage of the improved pricing situation. And that's exactly what we find. Below is the graph of combined new and existing home inventories:

The inventory of houses for sale is not just increasing, but it is increasing at an accelerating rate YoY.

In summary, examining interest rates, sales, prices, and inventory in order:

Today's pending home sales report also adds unusually useful information. In the late 1960s and 1970s, the era of rising interest rates, buyers would pick and choose when to buy, and would pounce whenever there was a meaningful, if short term, did in rates. In May of this year, mortgage rates got as low as 4.12%, the lowest since June 2013 but for one week in October. Since pending sales are based on contract signings, it is likely that buyers jumped in response to these low rates.

Further, just as in the late 1960's, when Boomers first entered the market, now it is Millennials. Now as then, it is only multi-unit (apartment) construction that is carrying the recovery in housing this year. Single family home starts and sales have completely stalled. Here is a graph of single family permits (blue) compared with 5 unit or higher permits (red) since January 2013:

Prices

Prices continue to increase, but YoY the price gains are decelerating, and in the case of existing home sales the non-seasonally adjusted data shows May 2014 prices below June and July 2013 prices. So let's start by showing the YoY% change in median prices in the Case Shiller 20 city index:

The YoY% change in median prices for new homes (red) and existing homes (blue): shows the same deceleration:

Finally, it is worth noting that the same deceleration is also showing up in the data at Depatment of Numbers Housing Tracker. I used this database of asking prices, which is updated weekly, to call in real time both the top of the housing boom in 2006, and the bottom of the housing bust in 2012. What is particularly noteworthy is that in 2006, it was the asking prices for houses in the 75th percentile (more expensive homes) which turned first. Now prices for those same more expensive houses are showing the most deceleration of all, as shown in this table, which shows the YoY% change for each percentile of houses for sale nationwide:

Month

|

25th

percentile

|

50th

percentile

|

75th

percentile

|

|---|---|---|---|

Jun 2013

|

6.3

|

7.4

|

7.5

|

Sep 2013

|

12.0

|

10.9

|

7.9

|

Dec 2013

|

13.3

|

11.2

|

7.8

|

Mar 2014

|

13.8

|

10.7

|

6.3

|

Jun 2014

|

14.3

|

10.9

|

5.9

|

Inventory

With housing prices still increasing, albeit at a reduced rate, we would expect to find more inventory entering the market, as potential sellers hope to take advantage of the improved pricing situation. And that's exactly what we find. Below is the graph of combined new and existing home inventories:

The inventory of houses for sale is not just increasing, but it is increasing at an accelerating rate YoY.

In summary, examining interest rates, sales, prices, and inventory in order:

- With interest rates turning slightly lower YoY, there will probably be renewed vigor in housing permits, starts, and sales by the end of this year. We have either already seen the interim bottom in permits, starts, and sales, or will shortly.

- Decelerating and/or YoY declining sales have existed long enough for prices gains to decelerate, although they haven't turned negative. The median price for existing home sales, however, may turn negative in the next 2 months.

- Although prices are decelerating, they are still higher YoY and thus inventory is continuing to pour onto the market. This will probably continue, but will begin to decelerate between now and the end of this year.

Interest rates have turned, sales are bottoming, prices are increasing at a quickly decelerating rate, and inventory is still increasing smartly. As per the normal order.