Why is this information important? The primary reason the Fed has lowered interest rates to barely positive is to spur lending. However, if businesses aren't borrowing -- or if banks aren't lending -- than this policy won't be nearly as effective.

Let's start by looking at the commercial an industrial section of the report.

Regarding lending standards, fewer domestic banks eased standards and terms on commercial and industrial (C&I) loans over the third quarter compared with recent quarters, particularly on loans to large and middle-market firms.2 About one-fourth of foreign respondents, which primarily lend to businesses, reported that they had tightened lending standards on C&I loans.3 All of the domestic and foreign respondents that reported having tightened standards or terms on C&I loans cited a less favorable or more uncertain economic outlook as a reason for the tightening. In response to a special question, a large number of both domestic and foreign respondents indicated that they had tightened standards on loans to European banks and their affiliates or subsidiaries. Standards for commercial and residential real estate loans changed little over the past three months, and a small net fraction of banks indicated that they had eased standards on several types of consumer loans.Let's place the above statements in context.

According to the survey, changes in loan demand were mixed. A moderate net fraction of banks reported weaker demand for C&I loans, in contrast to the increased demand reported in the previous three surveys; however, some large domestic banks continued to report stronger demand.4 Several large banks also reported increased demand for commercial real estate (CRE) loans. On the household side, demand for loans to purchase homes reportedly increased, though those reports may reflect the moderate rise in refinancing activity. Demand for home equity loans decreased, and demand for consumer loans reportedly was little changed.

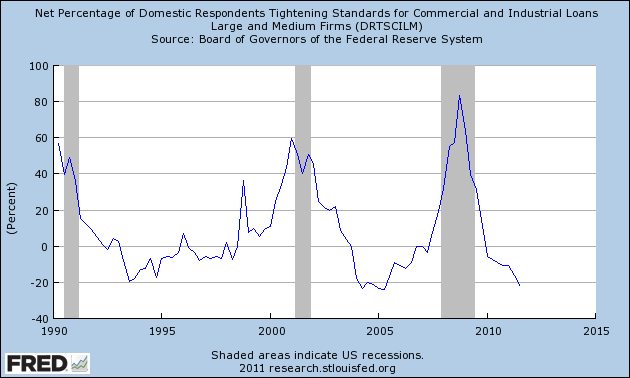

Since the worst parts of the recession, we've seen an overall loosening of lending standards on large C and I borrowers. Current levels are near the lows of the preceding two expansions.

But these reponses are for larger borrowers -- what about for smaller borrowers?

Here, again, we see a general unchanged situation.

Let's place these numbers in historical context

Like the chart for loans to larger borrowers, the number of institutions tightening lending standards to smaller firms is also dropping.

Let's see how this is playing out in the total number of C and I loans that have been extended.

After taking a serious nosedive during and slightly after the recession, the total number of C and I loans is increasing.

However, it's not the smaller banks that are making the loans, but

The largest 100.