While it seems odd to talk about increased inflation as a good economic development, for Japan it is. For the last 15 years they have been dealing with a prolonged period of deflation, which has led to at least one lost decade. About this time last year, Japan's new leader Abe introduced a plan to return Japan to a period of economic growth, which included the Bank of Japan doubling the monetary base in the period of a year. That policy is now having the desired effect of lowering the value of the yen, leading to increased import prices and hence a rise in prices.

Japan's core consumer inflation in August hit its highest level in nearly five years, while prices of personal electronics rose for the first time since 1992 - signs Japan may be emerging from 15 years of nagging deflation.

Core consumer prices, which include oil products but exclude

volatile prices of fresh food, rose 0.8 percent in August from a

year earlier after a 0.7 percent increase in July, marking the

third straight month of gains.

It was the fastest rise since November 2008, when core

consumer inflation hit 1 percent reflecting a spike in global

commodity prices, government data showed on Friday.

But most of the increase was caused by rising gasoline costs

and a weaker yen that inflated the price of food imports and may

dampen consumer sentiment, which is already showing signs of

peaking.

That said, prices of durable leisure goods, such as personal

computers and audio-visual equipment, rose 0.1 percent in August

from a year earlier, turning positive for the first time since

1992, in a sector where consumer prices have fallen steadily.

Showing posts with label Japan. Show all posts

Showing posts with label Japan. Show all posts

Friday, September 27, 2013

Friday, August 30, 2013

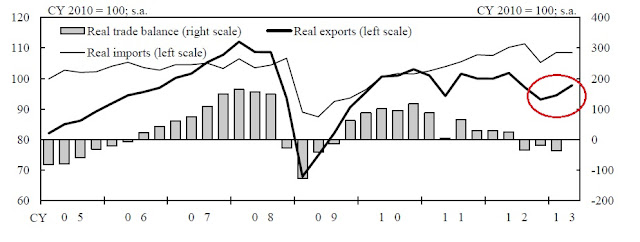

Yen Devaluation Starting to Pay Dividends With Increased Exports

Despite having a very weak economy, the yen actually strengthened over the duration of this expansion because of Japan's safe haven status. In fact, from the yen's ETF's lows in 2008 to its highs in 2011, it gained a little over 32%. However, since the end of last year and the introduction of "Abenomics" (which includes yen devaluation to increase the competitiveness of Japan's exports) the yen's ETF has dropped almost 26%. The end result is an increase in exports, as shown in this excerpt from the latest BOJ Central Bank Meeting Minutes:

Exports had been picking up. Real exports had turned upward in the January-March quarter of 2013 and kept increasing in the April-May period relative to that quarter, after having continued to decline in the July-September and October-December quarters of 2012. Exports of motor vehicles and their related goods -- due in part to the effects of developments in foreign exchange rates -- had resumed an uptrend, assisted by a pick-up in those to China -- which had seen a significant drop -- while those to the United States and other regions had been steady. Exports of capital goods and parts as a whole had recently started to bottom out, with upward movements observed in exports to the United States and East Asia, disregarding the fluctuations in ships. Exports of IT-related goods as a whole appeared to be heading for a bottom, with the effects of the downshift in demand for parts for final products of smartphones -- which had taken place since the end of 2012 -- easing. Exports were expected to increase moderately, mainly against the background of the pick-up in overseas economies.

The latest exports release shows a 12% year over year increase. Here's a chart of total exports from the latest BOJ monthly economic report:

Exports are still weak, as they are in line with the numbers reported over the last 3-4 years. However, we do see the uptick that is mentioned in the BOJ minutes.

Exports had been picking up. Real exports had turned upward in the January-March quarter of 2013 and kept increasing in the April-May period relative to that quarter, after having continued to decline in the July-September and October-December quarters of 2012. Exports of motor vehicles and their related goods -- due in part to the effects of developments in foreign exchange rates -- had resumed an uptrend, assisted by a pick-up in those to China -- which had seen a significant drop -- while those to the United States and other regions had been steady. Exports of capital goods and parts as a whole had recently started to bottom out, with upward movements observed in exports to the United States and East Asia, disregarding the fluctuations in ships. Exports of IT-related goods as a whole appeared to be heading for a bottom, with the effects of the downshift in demand for parts for final products of smartphones -- which had taken place since the end of 2012 -- easing. Exports were expected to increase moderately, mainly against the background of the pick-up in overseas economies.

The latest exports release shows a 12% year over year increase. Here's a chart of total exports from the latest BOJ monthly economic report:

Exports are still weak, as they are in line with the numbers reported over the last 3-4 years. However, we do see the uptick that is mentioned in the BOJ minutes.

Thursday, August 29, 2013

A Long-Term View of the Japanese ETF

The are two points I wanted to make about this chart:

1.) We see the Abenomics rally that started in 4Q12 and extended to 2Q13. Prices rallied about 44%.

2.) Since the rally prices have been consolidating in a symmetrical triangle pattern. This is to be expected after such a strong move as traders take profits and assess the effectiveness of the new programs.

Tuesday, July 30, 2013

Market/Economic Analysis: Japan -- Still Looking Better

From Reuters:

Japan's consumer prices rose in June for the first time in more than a year, a positive sign for the government's battle against deflation, but the rises centered on higher electricity bills rather than stronger demand that could drive a durable recovery.

.....

Core consumer prices rose 0.4 percent in June from a year earlier, higher than a median market forecast for a 0.3 percent increase, largely due to higher electricity bills and gasoline prices.

Japan's energy prices have been rising as a weaker yen has boosted the cost of imported fuel needed to make up for the closure of almost all the nation's nuclear reactors after the March 2011 tsunami.

"Such cost-push inflation should not be taken as particularly positive," said Yasuo Yamamoto, senior economist at Mizuho Research Institute. Market participants "are skeptical about the prospects for a steady pickup in inflation, with service-sector firms struggling to pass on costs to consumers due to a persistent output gap."

.....

"If you look at a narrower basket of goods without energy, the clear rising trend isn't there yet and we can't say with great confidence that Japan is clearly on its way out of deflation," said Koichi Fujishiro, economist at Dai-ichi Life Research Institute in Tokyo.

Short version: it's a start.

Here is a link to the Japanese CPI numbers from their statistical bureau.

Most importantly, the rise in inflation is a direct result of the BOJs plan to drop the yen's value. Consider this long-term chart of the yen's ETF:

The yen was in a clear uptrend from 2007 until the end of 2011 -- this despite the obvious weakness of their economy. The first reason is the yen was part of the carry trade -- people would borrow in yen because of their ultra low rates and then invest in another currency, pocketing the difference. After the Great Recession, the yen became a safe haven. But either way, a currency that should have been dropping in value because of the fundamental weakness of the underlying economy was rising.

Now it appears the yen is probably closer to "fair value" given the weakness of the Japanese economy.

In addition, Abe's party swept the most recent elections, giving them a strong mandate to continue their policies:

Japanese Prime Minister Shinzo Abe, fresh from a strong election victory, vowed on Monday to stay focused on reviving the stagnant economy and sought to counter suspicions he might instead shift emphasis to his nationalist agenda.

The victory in parliament's upper house election on Sunday cemented Abe's hold on power and gave him a stronger mandate for his prescription for reviving the world's third-biggest economy.

At the same time, it could also give lawmakers in his Liberal Democratic Party (LDP), some with little appetite for painful but vital reforms, more clout to resist change.

"If we retreat from reforms and return to the old Liberal Democratic Party, we will lose the confidence of the people," Abe told a news conference on Monday.

He emphasized that his priority remains proceeding with his "Abenomics" program of hyper-easy monetary policy, government spending and economic reform, describing it as the cornerstone of other policy goals.

Let's take a look at the Japanese ETF to see how it's fared:

After peaking in late May, the ETF fell to the 200 day EMA and rallied again to just shy of the previous peak. The ETF has dropped over the last few days in reaction to weak news coming out of China. It still appears that the Japanese market is consolidating gains made in the post Abe run-up.

Japan's consumer prices rose in June for the first time in more than a year, a positive sign for the government's battle against deflation, but the rises centered on higher electricity bills rather than stronger demand that could drive a durable recovery.

.....

Core consumer prices rose 0.4 percent in June from a year earlier, higher than a median market forecast for a 0.3 percent increase, largely due to higher electricity bills and gasoline prices.

Japan's energy prices have been rising as a weaker yen has boosted the cost of imported fuel needed to make up for the closure of almost all the nation's nuclear reactors after the March 2011 tsunami.

"Such cost-push inflation should not be taken as particularly positive," said Yasuo Yamamoto, senior economist at Mizuho Research Institute. Market participants "are skeptical about the prospects for a steady pickup in inflation, with service-sector firms struggling to pass on costs to consumers due to a persistent output gap."

.....

"If you look at a narrower basket of goods without energy, the clear rising trend isn't there yet and we can't say with great confidence that Japan is clearly on its way out of deflation," said Koichi Fujishiro, economist at Dai-ichi Life Research Institute in Tokyo.

Short version: it's a start.

Here is a link to the Japanese CPI numbers from their statistical bureau.

Most importantly, the rise in inflation is a direct result of the BOJs plan to drop the yen's value. Consider this long-term chart of the yen's ETF:

The yen was in a clear uptrend from 2007 until the end of 2011 -- this despite the obvious weakness of their economy. The first reason is the yen was part of the carry trade -- people would borrow in yen because of their ultra low rates and then invest in another currency, pocketing the difference. After the Great Recession, the yen became a safe haven. But either way, a currency that should have been dropping in value because of the fundamental weakness of the underlying economy was rising.

Now it appears the yen is probably closer to "fair value" given the weakness of the Japanese economy.

In addition, Abe's party swept the most recent elections, giving them a strong mandate to continue their policies:

Japanese Prime Minister Shinzo Abe, fresh from a strong election victory, vowed on Monday to stay focused on reviving the stagnant economy and sought to counter suspicions he might instead shift emphasis to his nationalist agenda.

The victory in parliament's upper house election on Sunday cemented Abe's hold on power and gave him a stronger mandate for his prescription for reviving the world's third-biggest economy.

At the same time, it could also give lawmakers in his Liberal Democratic Party (LDP), some with little appetite for painful but vital reforms, more clout to resist change.

"If we retreat from reforms and return to the old Liberal Democratic Party, we will lose the confidence of the people," Abe told a news conference on Monday.

He emphasized that his priority remains proceeding with his "Abenomics" program of hyper-easy monetary policy, government spending and economic reform, describing it as the cornerstone of other policy goals.

Let's take a look at the Japanese ETF to see how it's fared:

After peaking in late May, the ETF fell to the 200 day EMA and rallied again to just shy of the previous peak. The ETF has dropped over the last few days in reaction to weak news coming out of China. It still appears that the Japanese market is consolidating gains made in the post Abe run-up.

Thursday, July 11, 2013

Bank of Japan Sees Brighter Economic Picture

This is from the Bank of Japan's latest policy statement. I've broken out the individual points.

Japan's economy is starting to recover moderately. As for overseas economies, while the manufacturing sector continues to show a lackluster performance, they are gradually heading toward a pick-up as a whole.

Japan's economy is starting to recover moderately. As for overseas economies, while the manufacturing sector continues to show a lackluster performance, they are gradually heading toward a pick-up as a whole.

- In this situation, exports have been picking up.

- Business fixed investment has stopped weakening and shown some signs of picking up as corporate profits have improved.

- Public investment has continued to increase, and the pick-up in housing investment has become evident.

- Private consumption has remained resilient, assisted by the improvement in consumer sentiment. Reflecting these developments in demand both at home and abroad, industrial production is increasing moderately.

- Business sentiment has been improving. Meanwhile, financial conditions are accommodative.

- On the price front, the year-on-year rate of change in the consumer price index (CPI, all items less fresh food) is currently 0 percent.

- Some indicators suggest a rise in inflation expectations.

Tuesday, July 9, 2013

Market/Economic Analysis: Japan

Recent news out of Japan has been positive, as recently noted on the FT Alphaville blog:

A recovery in industrial production and consumer spending points to above-trend growth in Q2. Consumer price inflation may soon make a brief appearance above zero on the back of higher energy and import prices. But deflation isn’t beaten yet. The splurge of Japanese data overnight confirms the overall positive trend in the economy. Notably, industrial production increased by 2% in the month of May, the fourth consecutive monthly increase. Output in May was boosted by electronic components and machinery in particular. Both industrial production and exports are now on an upward trend (see chart below). To a large extent this recovery is due to the weaker yen. Although the yen is above its recent lows against the US dollar, it is still 19% lower than last November.

... the fall in the yen has coincided with an equity market rally. This, plus an increase in inflation expectations triggered by aggressive monetary ease from the Bank of Japan, is also helping to boost consumer spending. For May household spending data show a 0.1% monthly gain, while retail trade data were up by 1.5%. Both are on an upward trend and will support another quarter of fairly robust GDP growth in Q2. Meanwhile headline CPI inflation was -0.3% in May, up from -0.7% in April.

Higher energy prices are contributing to less deflation. Electricity prices are up 8.7% over the last 12 months, the fastest rate in over 30 years. Higher import prices as a consequence of the weaker yen may push national CPI inflation slightly above zero in coming months. But of course this would not herald the end of deflation as underlying pressures remain deflationary.

And that's not all. The latest data from the Tankan business survey shows that business confidence is on the rise. The latest coincident economic indicators may be signaling a possible turning point and the Conference Board's leading indexes are all rising:

The Conference Board LEI for Japan increased again in April, its fifth consecutive gain. Stock prices and the Tankan business conditions survey both made large positive contributions this month. Between October 2012 and April 2013, the LEI increased 6.1 percent (about a 12.5 percent annual rate), sharply up from the decline of 5.0 percent (about a -9.7 percent annual rate) during the previous six months. Moreover, the strengths among the leading indicators have remained very widespread in recent months.

.....

Eight of the ten components that make up The Conference Board LEI for Japan increased in April. The positive contributors to the index – in order from the largest positive contributor to the smallest – include stock prices, the Tankan business conditions survey, the six month growth rate of labor productivity, dwelling units started, real operating profits*, the interest rate spread, real money supply, and the new orders for machinery and construction component*. The negative contributors include the index of overtime worked and (inverted) business failures.

Also note bank lending has hit a four year high:

Let's turn to the markets:

From mid-May to early June the Japanese ETF sold off about 17%, largely thinking that the rally was a bit overdone. However, prices have since stabilized, trading between 10.25 and 11.25, also using the 200 day EMA as technical support. The decreasing volume tells us the sell-off is probably done for now, while the MACD is rising and is now in positive territory.

The yen rallied to just below the Fib fan from mid-May to mid-June, but has since fallen back. Expect a second test of the 94 level within the next few weeks.

A recovery in industrial production and consumer spending points to above-trend growth in Q2. Consumer price inflation may soon make a brief appearance above zero on the back of higher energy and import prices. But deflation isn’t beaten yet. The splurge of Japanese data overnight confirms the overall positive trend in the economy. Notably, industrial production increased by 2% in the month of May, the fourth consecutive monthly increase. Output in May was boosted by electronic components and machinery in particular. Both industrial production and exports are now on an upward trend (see chart below). To a large extent this recovery is due to the weaker yen. Although the yen is above its recent lows against the US dollar, it is still 19% lower than last November.

... the fall in the yen has coincided with an equity market rally. This, plus an increase in inflation expectations triggered by aggressive monetary ease from the Bank of Japan, is also helping to boost consumer spending. For May household spending data show a 0.1% monthly gain, while retail trade data were up by 1.5%. Both are on an upward trend and will support another quarter of fairly robust GDP growth in Q2. Meanwhile headline CPI inflation was -0.3% in May, up from -0.7% in April.

Higher energy prices are contributing to less deflation. Electricity prices are up 8.7% over the last 12 months, the fastest rate in over 30 years. Higher import prices as a consequence of the weaker yen may push national CPI inflation slightly above zero in coming months. But of course this would not herald the end of deflation as underlying pressures remain deflationary.

And that's not all. The latest data from the Tankan business survey shows that business confidence is on the rise. The latest coincident economic indicators may be signaling a possible turning point and the Conference Board's leading indexes are all rising:

The Conference Board LEI for Japan increased again in April, its fifth consecutive gain. Stock prices and the Tankan business conditions survey both made large positive contributions this month. Between October 2012 and April 2013, the LEI increased 6.1 percent (about a 12.5 percent annual rate), sharply up from the decline of 5.0 percent (about a -9.7 percent annual rate) during the previous six months. Moreover, the strengths among the leading indicators have remained very widespread in recent months.

.....

Eight of the ten components that make up The Conference Board LEI for Japan increased in April. The positive contributors to the index – in order from the largest positive contributor to the smallest – include stock prices, the Tankan business conditions survey, the six month growth rate of labor productivity, dwelling units started, real operating profits*, the interest rate spread, real money supply, and the new orders for machinery and construction component*. The negative contributors include the index of overtime worked and (inverted) business failures.

Also note bank lending has hit a four year high:

Japanese bank lending marked its biggest annual increase in four years in June, suggesting the central bank’s aggressive monetary stimulus and brightening economic prospects are spurring fund demand for fresh investment.

Outstanding loans held by Japanese banks rose 1.9 per cent in June

from a year earlier, Bank of Japan data showed on Monday, marking the

20th straight month of increase and posting the biggest gain since July

2009.Let's turn to the markets:

From mid-May to early June the Japanese ETF sold off about 17%, largely thinking that the rally was a bit overdone. However, prices have since stabilized, trading between 10.25 and 11.25, also using the 200 day EMA as technical support. The decreasing volume tells us the sell-off is probably done for now, while the MACD is rising and is now in positive territory.

The yen rallied to just below the Fib fan from mid-May to mid-June, but has since fallen back. Expect a second test of the 94 level within the next few weeks.

Tuesday, June 25, 2013

BOJ's Initial Actions Effective

The above charts shows the currency problem faced by the BOJ: even as their interest rates were at record lows and their economy was barely growing, the yen was strengthening. The ETF rose from 90 in mid-2008 to 130 at the end of 2011, for a percentage gain of 44%. The banks recent moves to double the currency base has effectively told the markets the central bank intends to have the yen drop in value -- which it clearly has. It's moved from from the high of 130 to 94 earlier this year, for a drop of 27.4%.

Monday, June 10, 2013

The Japanese Sell-Off In Perspective

Since Abe's election in November, the Japanese ETF has rallied strongly, rising from a low of 8.75 to ~12.50, for a net gain of about 43%. Prices dropped through support at the beginning of June on very strong volume, indicating that traders were concerned about the strength of the rally relative to the underlying economic fundamentals (essentially asking have we risen too far too fast). Prices fell to the 200 day EMAn which is also near the 50% Fib level.

The weekly charts shows that prices have found support around the 61.8% Fib level for the mid-2012/mid-2013 price levels.

My guess is we'll continue to see a thinning out of the rally trade as people take more of a wait and see attitude about Abe's policies. However, news like this certainly won't hurt:

Japan has revised up its first-quarter economic growth to 1 per cent, giving Prime Minister Shinzo Abe a boost as he seeks to strengthen his grip on power in next month’s upper house elections.

Government data released on Monday showed that the economy expanded at an annualised rate of 4.1 per cent between January and March, lifted by strong household spending and a pick-up in private residential investment. That was much higher than the preliminary estimate of 3.5 per cent, which was already the fastest rate recorded by any Group of Seven economy.

Thursday, March 21, 2013

Will Japan Return To Growth?

The above weekly chart of the the Japanese ETF shows two recent rallies. The first occurred at the end of last year. The ETF traded in sideways for the first few weeks of the year, then started to move higher. Now prices have moved through resistance at around the 10.5 area and have a fair amount of daylight to the 11.1 level.

However, the real story for Japan has been the drop in the yen's value:

From the peak to low on the chart, we see a decline of a little over 20%.

Most of the recent market action is due to the hope that the new head of the BOJ will engage in a reflation of the economy:

Investors are betting that Prime Minister Shinzo Abe’s nominee to run the Bank of Japan will open the monetary floodgates, buy government bonds and pursue a 2% inflation target to reflate the long-stagnant Japanese economy. The new leadership team at the BOJ, led by Haruhiko Kuroda, is awaiting approval from the Japanese Diet this week.

Viewing Japan as the mother of all reflation plays, foreign investors are pouring money into Japanese stocks at a frantic pace. Last week, overseas investors bought about $10.5 billion worth of Japanese equities. That matters since non-Japanese investors drive about 60% of the daily trading activity at the Tokyo Stock Exchange.

Abe is trying to simultaneously push the BOJ to weaken the yen to boost exports, and stoke domestic demand by creating inflationary expectations. Nomura estimates that Japan currently has about a $170 billion gap between current GDP and potential GDP. The yen has already weakened dramatically against the dollar. However, it’s uncertain whether the central bank can move Japan from its current deflation to moderate inflation. (For a useful guide to Abenomics, check out this recent post from Business Insider.)

Let's take a look at some underlying Japanese data, starting with GDP.

At the end of 2010 and beginning 2011, we see a contraction caused by the Tsunami that occurred in the spring of 2010. However, since the sharp rebound in 3Q11, GDP has been on a downward trajectory.

Let's take a look at the detail of the GDP report:

The most obvious point of the above graph is that Japan has been contracting for the last three quarets. The primary reason for this has been a drop in private demand. In looking at the sub-components, notice that non-residential investment has either stood at 0 or contracted for the last three quarters. However, we see an uptick in this number from the latest data:

Inventory adjustments have also been responsible for two quarers of contraction.

However, for the Japanese, the big issue is the drop in exports. Remember: Japan invented the Asian model for growth, namely, export your way to prosperity. Yet exports have been dropping for the last three quarters, and have contracted in four of the last five. One of the things that traders are betting on is that the 20% drop in the yen will turn this number around. This is necessary, as the nominal Japanese trade balance has been negative for the last seven quarters:

Part of the reason for this drop has been the EU recession and US' slow growth. However, the US appears to be at least holding its own. Also remember that Japan and China had a 2 quarter trade spat last year that greatly reduced Japanese exports to that country; this spat has been calming down over the last few months.

Japan isn't out of the woods by any stretch. However, the government is hoping for the following series of events to take place: a drop in the yen leads to an increase in exports, which in turn leads to an increase in business investment to support the increase in external demand.

Link for all charts and economic data.

Subscribe to:

Posts (Atom)