- by New Deal democrat

The message of this morning’s consumer inflation report was the same for almost everything except for the fictitious measures of shelter: sharp deceleration everywhere.

Let’s take a look:

Headline CPI up 0.2% m/m and 3.1% YoY (lowest since March 2021)

Core CPI up 0.2% m/m and 4.9% YoY (lowest since October 2021):

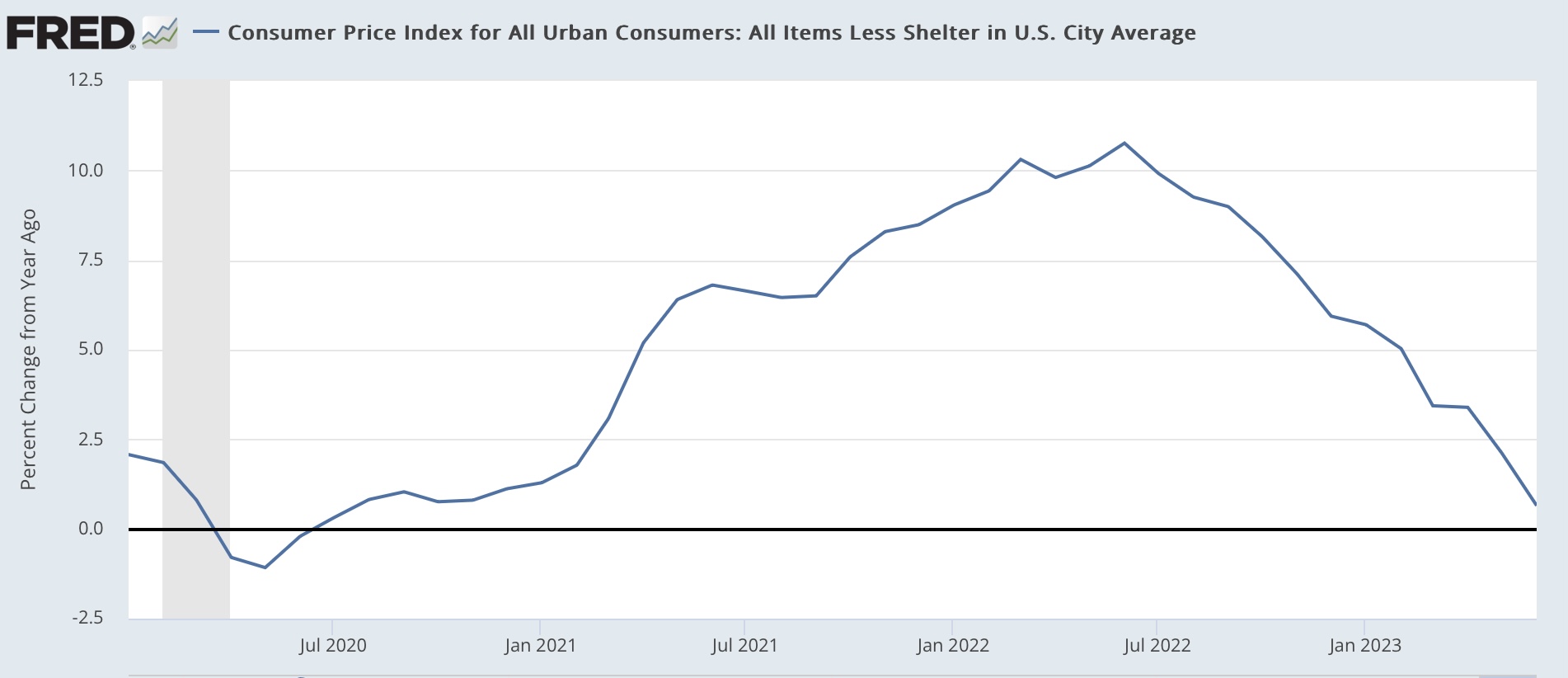

CPI less shelter up +0.2% and 0.7% YoY (lowest since February 2021):

New and Used vehicles: 0.0% and down -0.5% respectively m/m, and up +4.1% and down -5.2% YoY respectively:

Food up 0.1% m/m and 5.7% YoY:

But food is only up 0.3% in the 4 months since February:

Transportation services (replacement parts, repairs etc.) has also been a hot spot, and has also decelerated, up 0.4% m/m and up 8.2% YoY (but down from a peak of 15.2% YoY last October:

Finally, Owners Equivalent Rent up 0.4% m/m:

and 7.8% YoY (down from all time YoY high of 8.1% YoY in April):

Here’s what it looks like in comparison with house prices as measured by the Case Shiller national index YoY (/2.5 for scale):

Since the beginning of this year, monthly increases in OER have declined from 0.8% to 0.45%. YoY OER is probably going to be below 4.0% and maybe below 3.0% by the end of next winter.

To sum up: except for the fictitious measure of shelter, the only other remaining “hot spots” for inflation are new vehicles (but resolving as the supply chain issues have finally resolved) and transportation services. Food inflation has basically stopped in the past 4 months.

And if actual new rent increase and house prices were substituted for the fictitious OER measure and the 12 month average used for leases, headline inflatioin would only be up about 0.8% YoY, and core inflation up 3.0%.

But I’m sure there’s some sticky price blah blah blah somewhere that will justify the Fed’s continued hawkishness.