- by New Deal democrat

Industrial production, the now-deposed King of Coincident Indicators, rebounded strongly in December.

I say “deposed” because before 2001 and especially before the Great Recession, any YoY decline in production *always* coincided with or at least immediately heralded a recession. But since the accession of China to regular trading status in 1999, downturns of even -5% or more, as in 2015-16 and 2018-19 have not necessarily meant recession.

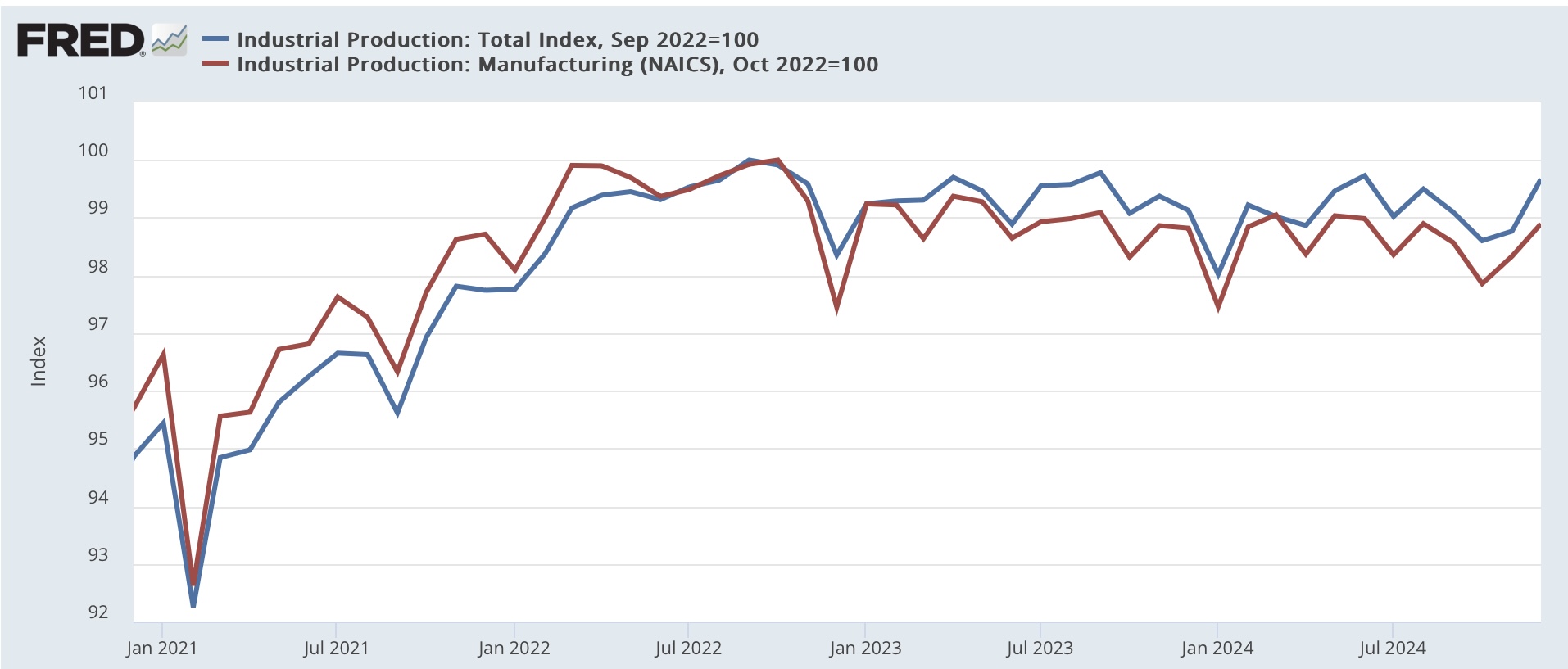

In December total industrial production rose 0.9%, while manufacturing production rose 0.6%. The November number for each was also revised higher by 0.3%. While this is obviously a big increase, mainly it just reverses the likely hurricane induced declines of the past few months. Total production made a 6 month high, while manufacturing production only made a 4 month high. Further, both remain down from their late 2022 peaks by -0.3% and -1.1% respectively:

With the big improvement this month, on a YoY basis total production is now up by 0.6%, and manufacturing production by 0.1%:

Despite the lackluster performance of manufacturing and production for the past two years, the economy has continued to be powered forward by consumption of services, and also by construction sector, and in particular construction employment, which as I pointed out earlier this morning has continued to increase.