- by New Deal democrat

This might be a good time to reiterate why I post each week on jobless claims, and what my system is.

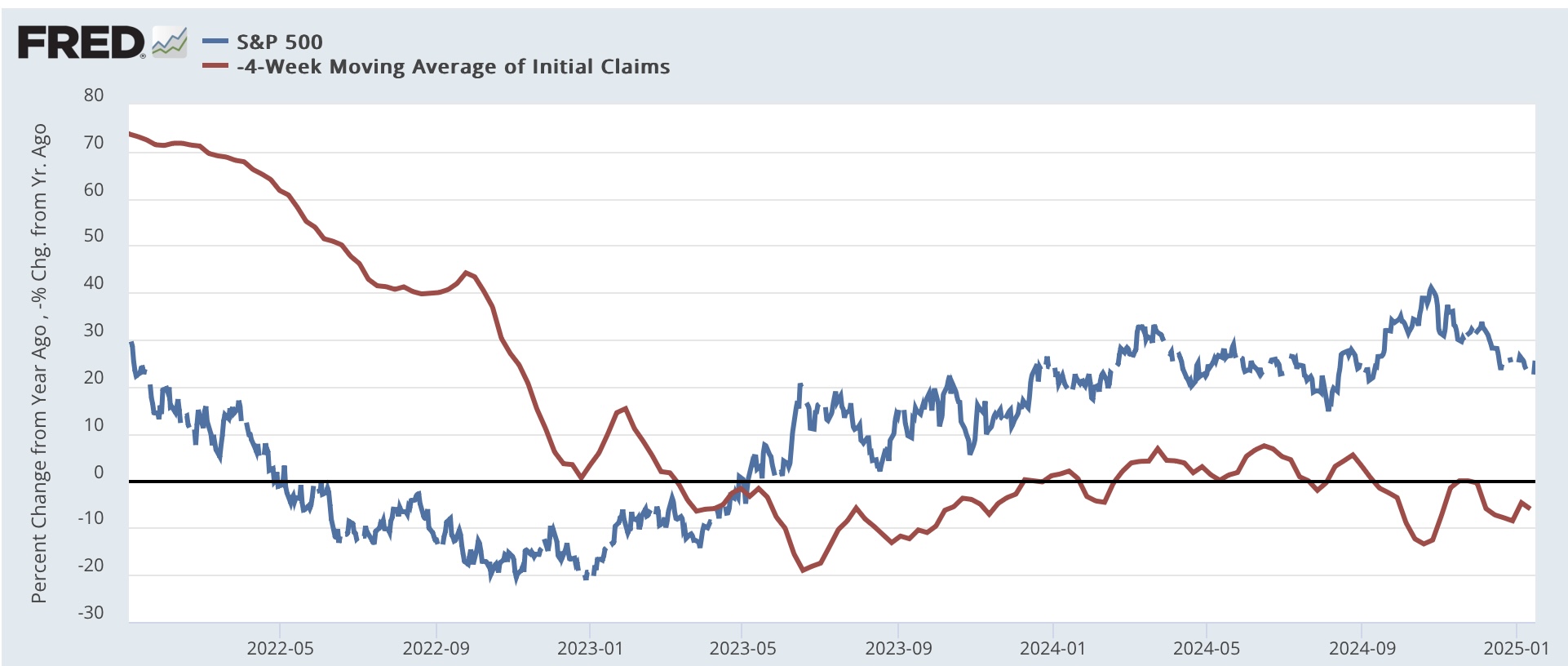

Initial jobless claims in particular are a recognized leading indicator. In fact, they are one of the 10 official components of the Index of Leading Economic Indicators. Additionally, together with the YoY% change in stock prices they form my “quick and dirty” forecasting tool.

Based on the nearly 60 year history of initial jobless claims: when initial claims are lower YoY, that is positive for good economic growth in the next few months. When they are higher by less than 10%, they are neutral — still indicating growth, but more anemic. When they (especially the 4 week moving average) are higher by over 10%, that is a yellow flag indicating the risks of recession are significant. Finally, when they are higher by 12.5% or higher for a period that persists for at least two months, that constitutes a red flag recession warning, because under those circumstances a recession has almost always been close at hand. We almost triggered that red flag 18 months ago, but the high YoY change in claims backed off just short of the two month trigger. It has turned out that there is some residual seasonality that hasn’t been massaged out of the numbers that first really appeared in 2023, and that is the type of reason why I need the signal to persist for at least two months.

With that out of the way, let’s look at this week’s numbers.

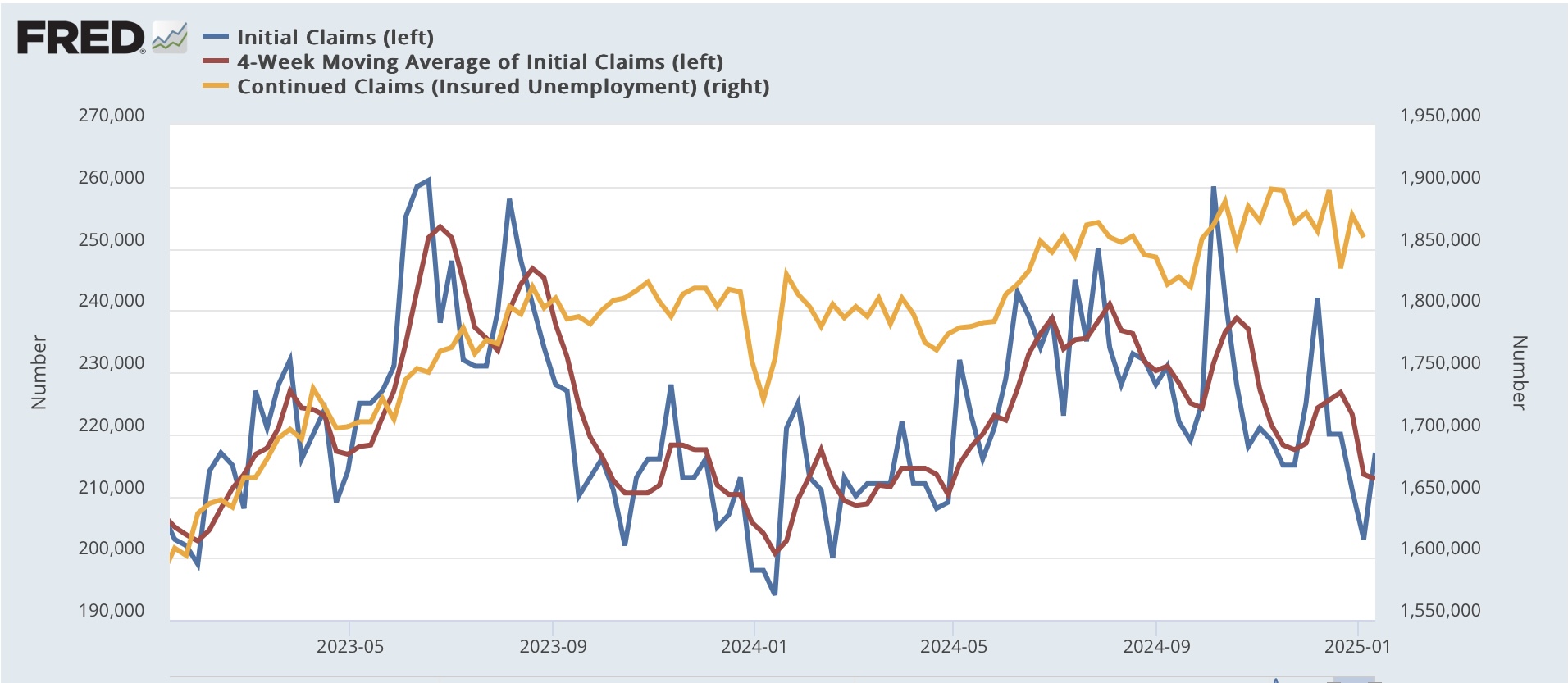

Initial claims rose 14,000 to 217,000, while the four week average declined -750 to 212,750. Continuing claims also decreased -18,000 to 1.859 million:

On the YoY% basis I use for forecasting as described above, initial claims were up 11.9%, while the more important four week moving average was up 6.0%. Continuing claims were also up 7.6%:

Per the above, although the weekly number came in higher by more than 10%, because the four week average remains under that threshold, this was a neutral reading. It suggests slow improvement in the economy in the months ahead.

Finally, since I mentioned it above, here is the current state of the “quick and dirty” model (note the four week average of initial claims is inverted so that a negative reading shows as below the zero line):

Note there was a brief 2 month period in 2023 when both were negative, but jobless claims were not higher by more than 10% during that period, so there was no true recession signal.