- by New Deal democrat

Consumption leads employment, and as I reiterated yesterday real per capita retail sales has a history as a long leading indicator.

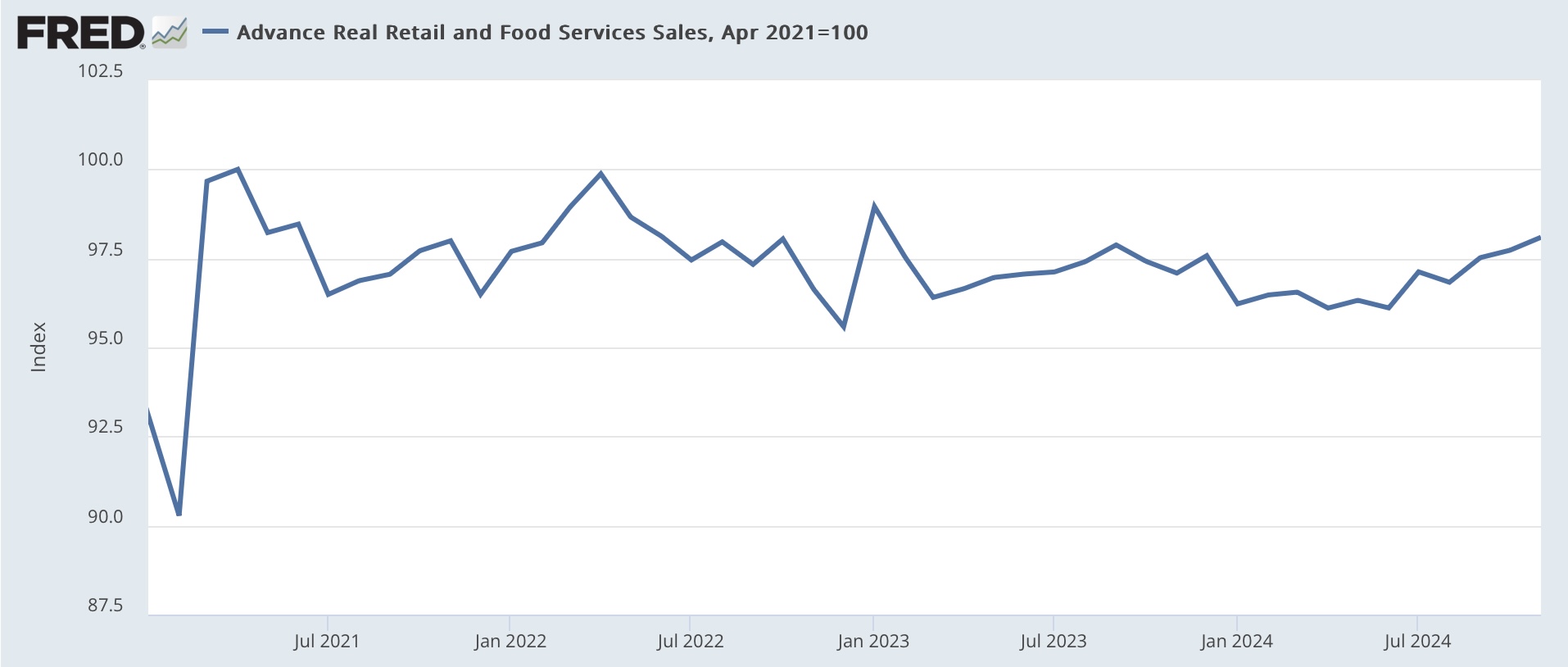

Which means that retail sales for November, which rose 0.7% nominally, continues its recent strong string of positives, increasingly looking like it is finally breaking out of its 2 year plus doldrums.

Since consumer prices rose 0.3% in November, real retail sales were up 0.4% for the month. While real retail sales are still -1.9% below their all time peak right after the 2021 stimulus package, with today’s report they are the highest since May 2022 except for one month:

On a YoY basis, they are also higher by 1.0%:

This is another positive since recessions typically occur with sales negative YoY. Here’s what the past 30 years before the pandemic look like, subtracting 1% from the YoY measure so that it shows at the zero line:

It’s a weak result, but for a change a non-recessionary one.

Finally, real retail sales are a good short leading indicator for the trend in jobs growth. Yesterday I speculated that real retail sales per capita might be distorted in the past several years by the outsized importance to CPI of the sharp increase in the shelter component. So in the graph below I also include real sales ex-shelter (light blue):

Either way, real retail sales are forecasting continued deceleration - which at this point translates into increased weakness - in hiring in the months ahead. Because, as I have pointed out in several posts in the past few weeks, YoY jobs gains are likely to be revised significantly downward for late 2023 and 2024 when we get the annual benchmark revisions in a couple of months, we may be closer to the trend line forecast by real retail sales already.