- by New Deal democrat

We got two important leading indicators this morning. Both were better than expected.

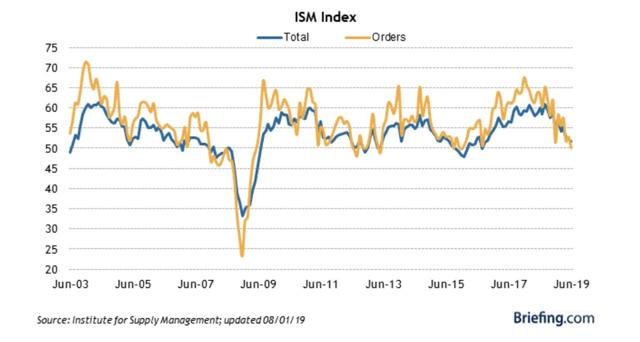

First, July data started out with an ISM manufacturing index reading that declined slightly to 51.2, but remained above the neutral level of 50.0. Even more important, the new orders subindex rose slightly to 50.8:

Manufacturing as measured by this index, as well as the regional Fed indexes, has been slow, but has doggedly resisted going into contraction.

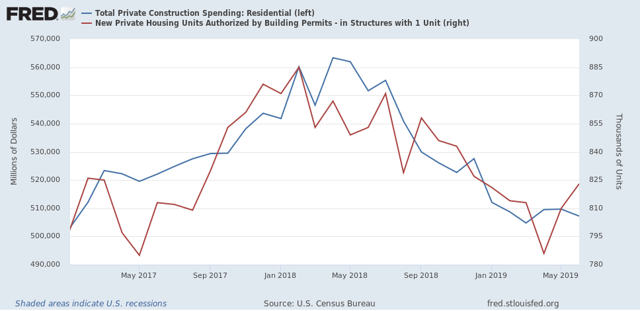

June construction spending declined, as did the component of residential construction. But the good news here is that there were substantial upward revisions to the last few months, so the final number was about 1% higher than the initial reading for last month:

Construction spending follows permits and starts with a lag, but is much less noisy. I don’t think we’ve reached bottom yet in this metric, but with the revisions the June number has to be treated as a positive.

One last thing: looking ahead to tomorrow’s employment report, the American Staffing Index had the worst YoY reading of the year so far this week, at -3.7%:

So I’m expecting weak numbers for the leading manufacturing, residential construction, and temporary employment sectors tomorrow, at least as compared with last year, with the most likely negative number being in temporary employment.

One last thing: looking ahead to tomorrow’s employment report, the American Staffing Index had the worst YoY reading of the year so far this week, at -3.7%:

So I’m expecting weak numbers for the leading manufacturing, residential construction, and temporary employment sectors tomorrow, at least as compared with last year, with the most likely negative number being in temporary employment.