Saturday, October 7, 2017

Weekly Indicators for October 2 - 6 at XE.com.

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

The slew of positive trends continues.

Friday, October 6, 2017

September jobs report: establishment survey stinks, but household survey rocks!

- by New Deal democrat

HEADLINES:

- -33,000 jobs lost

- U3 unemployment rate down -0.2% from 4.4% to 4.2% (new low)

- U6 underemployment rate down -0.3% from 8.6% to 8.3% (new low)

Here are the headlines on wages and the chronic heightened underemployment:

Wages and participation rates

- Not in Labor Force, but Want a Job Now: down -216,000 from 5.844 million to 5.628 million

- Part time for economic reasons: down -133,000 from 5.255 million to 5.122 million (new low)

- Employment/population ratio ages 25-54: up +0.5% from 78.4% to 78.9% (new high)

- Average Weekly Earnings for Production and Nonsupervisory Personnel: up $.0.09 from $22.14, to $22.23, up +2.5% YoY. (Note: you may be reading different information about wages elsewhere. They are citing average wages for all private workers. I use wages for nonsupervisory personnel, to come closer to the situation for ordinary workers.)

Holding Trump accountable on manufacturing and mining jobs

Trump specifically campaigned on bringing back manufacturing and mining jobs. Is he keeping this promise?

Trump specifically campaigned on bringing back manufacturing and mining jobs. Is he keeping this promise?

- Manufacturing jobs fell by -1,000 for an average of +9,800 a month vs. the last seven years of Obama's presidency in which an average of 10,300 manufacturing jobs were added each month.

- Coal mining jobs rose by 500 for an average of +133 a month vs. the last seven years of Obama's presidency in which an average of -300 jobs were lost each month

The more leading numbers in the report tell us about where the economy is likely to be a few months from now. These were mainly flat.

- the average manufacturing workweek was unchanged at 40.7 hours. This is one of the 10 components of the LEI.

- construction jobs increased by +8,000. YoY construction jobs are up 184,000.

- temporary jobs increased by +5,900.

- the number of people unemployed for 5 weeks or less increased by +4,000 from 2,222,000 to 2,226,000. The post-recession low was set al,ost two years ago at 2,095,000.

Other important coincident indicators help us paint a more complete picture of the present:

- Overtime was flat at 3.3 hours.

- Professional and business employment (generally higher- paying jobs) increased by +13,000 and is up +528,000 YoY.

- the index of aggregate hours worked in the economy fell by -0.1 from 107.4 to 107.3

- the index of aggregate payrolls rose by +0.5 from 134.7 to 135.2.

Other news included:

- the alternate jobs number contained in the more volatile household survey increased by 906,000 (!) jobs. This represents an increase of 2,419,000 jobs YoY vs. 1,777,000 in the establishment survey.

- Government jobs rose by +7,000 .

- the overall employment to population ratio for all ages 16 and up rose +0.3% from 60.1% to 60.4 m/m and is up +0.6% YoY.

- The labor force participation rate rose +0.2% m/m and is up +0.2% YoY from 62.9% to 63.1%.

SUMMARY

This report was certainly affected by Hurricanes Harvey and Irma, but what is surprising is all of the areas of strength, especially in the household report.

Both the U3 and U6 unemployment and underemployment rates fell to new lows for this expansion. Involuntary part-time employment also fell to a new low. Prime age labor force participation rose to a new high.

Even in the establishment survey, but for the huge decline in leisure and hospitalityworkers, the headline number would have been +78,000. And the l eading category of temporary jobs increased.

The only cautions to my surprisingly upbeat take on this report are that net revisions to July and August were lower, which has become increasingly common this year; and the household survey, which included a gain of over 900,000 jobs ( ! ) was likely something of an outlier.

But despite the negative headline number of jobs, the totality of the two reports show an underlying strong labor market -- with of course the dismal and chronic exception of lackluster wage growth.

Thursday, October 5, 2017

Hurricane adjusted initial jobless claims for the week of September 23: 246,000

- by New Deal democrat

I am repeating an exercise I undertook in 2012 when Superstorm Sandy disrupted the initial claims data: estimating what the initial jobless claims would have been, but for the hurricanes.

I created that adjustment by backing out the affected states (NY and NJ) from the non-seasonally adjusted data, which gave me the number of initial claims filed in the other 48 states. I compared that with the same metric one year earlier, and multiplied by the seasonal adjustment to arrive at the number if the affected states had the same relative number of claims during the given week, as all of the unaffected states.

This tells us whether or not the hurricane disruptions are masking any underlying weakness in the economy.

This tells us whether or not the hurricane disruptions are masking any underlying weakness in the economy.

This year I backed out Texas starting 3 weeks ago, and added Florida two weeks ago. This week I have added Puerto Rico.

The state by state data is released with a one week delay. So what follows is the analysis for the week of September 23, the number for which was reported at 272,000.

Here is the table for the Week of September 24 in 2016 vs. September 23 this year:

Metric 2016 2017

Seasonally adjusted: 252,000 272,000

Adjustment for total: 1.27 1.26

Not seasonally adjusted: 198,455 215,031

Florida claims: 7,255 18,477

Puerto Rico claims: 1,229 2,489*

Texas claims: 14,694 20,104

Puerto Rico claims: 1,229 2,489*

Texas claims: 14,694 20,104

NSA claims ex-FL,TX,PR:175,277 173,961

FL, TX, PR as % of total: 11.7% n/a

2017 w/ FL,TX, PR adjustment: n/a 194,314

*The Department of Labor estimated the number of claims for Puerto Rico last week.

In 2016 the weekly seasonal adjustment was 1.27. This year it was 1.26 Multiplying the non-seasonally adjusted total of 194,314 by 1.27 gives us 247,000. Multiplying by 1.26 gives us 245,000.

Thus the hurricane-adjusted initial jobless claims number for the week of September 23, 2017 is 246,000.

Thus the hurricane-adjusted initial jobless claims number for the week of September 23, 2017 is 246,000.

Here are the hurricane-adjusted numbers for previous three weeks:

Sept. 2: 239,000.

Sept. 9: 229,000.

Sept. 16: 237,000

The four week hurricane adjusted average is 237,750.

The underlying national trend in initial jobless claims remains very positive.

Wednesday, October 4, 2017

ISM manufacturing and vehicle sales: surprising signs of short term strength

- by New Deal democrat

Just a quick note about two data releases this week, one of which was (apparently) whipsawed by the hurricanes, and the other (surprisingly) was not.

Motor vehicle sales appears to have been whipsawed by Hurricane Harvey, showing a very strong 18.4 million units annualized after a very weak 16.0 units in August:

(Note the FRED data, by contract, is delayed one month so does not yet show September). It's pretty clear these two months should be averaged to get a better idea of the trend, which is a little over 17 million units. Even so, that is an improvement from earlier this year. More importantly, it takes the notion of an immediate recession signal off the table.

ISM manufacturing came it at a very strong 60.8, which is not just the highest reading of this entire expansion, it is the highest since 2004. Meanwhile the new upstart Markit PMI posted at 53.1, a moderately positive number (h/t Doug Short):

The ISM figure once again confirmed the strength shown in the regional Fed indexes, which surprisingly even included Texas. Even PMI's more tepid reading did not appear to be affected by the Texas and Florida hurricanes.

While the regional Fed indexes and ISM manufacturing have been running a little "hot" this year, they do generally correlate well with the manufacturing component of industrial production.

The bottom line is that these are two short leading signals that the economy is doing very well.

Tuesday, October 3, 2017

Construction spending and the housing slowdown

- by New Deal democrat

Is residential construction spending confirming the slowdown apparent in housing permits and new home sales?

This post is up at XE.com.

Sunday, October 1, 2017

A thought for Sunday: of basic decency and humanity, and how the economy is shoring up the GOP

- by New Deal democrat

A few threads of the Trump malAdministration came rogether this past week.

The latest attempt to overturn Obamacare confronted Trump with a choice between his two main goals: basking in a Trump triumph vs. erasing all of Obama's programs from the history books (in retaliation for Obama humiliating him at the White House correspondents' dinner in 2011).

At the beginning of his presidency, Trump opposed the "repeal and run away" Congressional GOP objectives for Obamacare, telling them he wanted a "replacement" plan with more coverage and lower premiums. He wanted, in short, a Trump triumph.

After 3 failures, however, Congress's 4th try at dismantling Obamacare has no replacement features. Things like guaranteed coverage of pre-existing conditions were stripped away. The bill in essence simply repealed Obamacare, punted the issue to the States with instructions to not even think about enacting something like universal coverage, and gutted Medicaid to boot. In short, it was very much "repeal and run away" (with a fig leaf).

Trump's support for the bill showed that he will even eschew a Trump triumph if the alternative obliterates an Obama accomplishment.

Another thread of the Trump presidency is its nearly constant failure on the test of basic decency and humanity.

One of the places where it had been safe to avoid the rancid circus of Washington was The Weather Channel. Not this past week, where it more than any other media outlet highlighted the humanitarian crisis in Puerto Rico, which appears to be approaching Katrina x 10. When an outlet as innocuous as The Weather Channel feels compelled to implore Washington to DO SOMETHING! you know that those in power have plumbed a new low in the banality of evil.

One of the places where it had been safe to avoid the rancid circus of Washington was The Weather Channel. Not this past week, where it more than any other media outlet highlighted the humanitarian crisis in Puerto Rico, which appears to be approaching Katrina x 10. When an outlet as innocuous as The Weather Channel feels compelled to implore Washington to DO SOMETHING! you know that those in power have plumbed a new low in the banality of evil.

I have a feeling, however, that conditions in Puerto Rico are going to get much worse -- and maybe finally noticed by the actual news media -- before they get better.

Which brings me to the final thread. Polling for Trump has been waxing and waning within a limited range for half a year now. It waxes when there he rails against foreign or domestic enemies, like North Korea or uppity nonwhite malcontents, and wanes when his basic lack of decency and humanity is in the forefront. To wit, here is the latest update from Gallup:

Why hasn't it sunk any lower?

Paradoxically, Trump and the GOP are benefitting from the pretty decent Obama economy -- which is still in place, on autopilot, because the GOP has accomplished exactly zero legislatively on economic matters.

Paradoxically, Trump and the GOP are benefitting from the pretty decent Obama economy -- which is still in place, on autopilot, because the GOP has accomplished exactly zero legislatively on economic matters.

And the ongoing Obama economy at the moment has a 4.4% unemployment rate, is still adding about 150,000 new jobs a month, has real median household income at its highest in a decade, if not forever, and real hourly wages for nonsupervisory workers at their highest in 4 decades. In short, civil society may be going to hell, but the economy? Not too shabby.

Historically, in the absence of either war or civil unrest generating a real death toll that dominates the headlines (like Korea, Vietnam, or the race riots of the late 1960s), an economy with these numbers generates reasonably good numbers for the incumbent political party. The benefit of that -- of Obama's economy -- is currently going to the GOP!

But if Trump's approval is in the 35%-40% range with a decent economy -- and the Congressional GOP polling at the worst ever -- just imagine what the polling is going to be like when the economy as it must ieventually turns down.

Saturday, September 30, 2017

Weekly Indicators for September 25 - 29 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

Despite the disruptions of three major hurricanes, the underlying economy remains in pretty strong shape.

Friday, September 29, 2017

Ex-hurricane trend in September industrial production is positive

- by New Deal democrat

As I outlined earlier this week, a reasonable temporary workaround for industrial production unaffected by the recent hurricanes is to average the 4 regional Fed surveys, minus Dallas, plus the Chicago PMI. Over the long run, each +5 in the average of the indexes is consistent with a +.1 in the manufacturing component of industrial production. Because these indexes have been running "hot" this year compared with industrial production, I further suggested subtracting .3 from the result to be confident in a positive trend.

All of these indexes have been reported for September. Here are the numbers:

Empire State: 24.4

Philadelphia Fed: 23.8

Richmond Fed: 19

Kansas City Fed: 17

Chicago PMI: 30.4 (adjusted)*

Interestingly, even the Dallas Fed's index was positive, at 19.5!

*Since Chicago is on a 0 to 100 scale with 50 being neutral, we subtract 50 from the raw number of 65.2, which gives us 15.2, and then double the result.

The average of the 5 is 22.9.

Dividing that by 5 gives us +.5.

Subtracting .3 gives us +.2.

We can be reasonably confident that underlying trend in industrial production in September, despite the hurricanes, has been positive.

Thursday, September 28, 2017

Hurricane-adjusted initial claims for the week of September 16: 237,000

- by New Deal democrat

I am repeating an exercise I undertook in 2012 when Superstorm Sandy disrupted the initial claims data: estimating what the initial jobless claims would have been, but for the hurricanes.

In 2012 I created that adjustment by backing out the affected states (NY and NJ) from the non-seasonally adjusted data. That gave me the number of initial claims filed in the other 48 states. I compared that with the same metric one year earlier, and multiplied by the seasonal adjustment.

That gave me the number if the affected states had the same relative number of claims during the given week, as all of the unaffected states. In 2012, it showed that Sandy was not masking any underlying weakness in the economy.

I backed out Texas starting 2 weeks ago, and also Florida beginning last week.

I backed out Texas starting 2 weeks ago, and also Florida beginning last week.

The state by state data is released with a one week delay. So what follows is the analysis for the week of September 16, the number for which was reported at 259,000 one week ago and revised upward today to 260,000.

Here is the table for the Week of September 17 in 2016 vs. September 16 this year:

Metric 2016 2017

Seasonally adjusted: 252,000 260,000

Adjustment for total: 1.23 1.22

Not seasonally adjusted: 205,649 212,962

Florida claims: 7,603 10,052

Texas claims: 14,817 28,387

Texas claims: 14,817 28,387

NSA claims ex-TX+FL 183,229 174,523

TX+FL as % of total: 10.9% n/a

2017 w/ TX+FL adjustment: n/a 193,546

In 2016 the weekly seasonal adjustment was 1.23. This year it was 1.22 Multiplying the non-seasonally adjusted total of 193,546 by 1.23 gives us 238,000. Multiplying by 1.22 gives us 236,000.

Thus the hurricane-adjusted initial jobless claims number for the week of September 16, 2017 is 237,000.

Thus the hurricane-adjusted initial jobless claims number for the week of September 16, 2017 is 237,000.

The previous adjustment for Sept. 2 was 239,000.

Sept. 9 was 229,000.

The average of the three hurricane adjusted weeks so far is 235,000.

The underlying national trend in initial jobless claims remains very positive.

Wow! Yellin confirms 2% inflation is the Fed's ceiling

- by New Deal democrat

You may have already seen this elsewhere, but in case you didn't, Janet Yellin all but officially confirmed the other day that 2% isn't in fact the Fed's target, it's their ceiling. Per the New York Times:

Given that monetary policy affects economic activity and inflation with a substantial lag, it would be imprudent to keep monetary policy on hold until inflation is back to 2 percent,” Ms. Yellen told the National Association for Business Economics .Let me just remind you one more time that in the past 50 years, during recessions the inflation rate has typically fallen by more than 2%. That means that if the Fed is "successful," the next recession will tip over into outright deflation, including deflation in even nominal wages.

Now imagine a wage-price deflationary spiral beginning with Donald Trump as president and the GOP in control of both houses of Congress.

Wednesday, September 27, 2017

Home sales decline -- even leaving out the hurricane-affected South

- by New Deal democrat

As promised yesterday, I put together the graphs and charts to show you that, even when we take out Florida and Texas, new home sales have still turned down slightly since their last peak in March.

The trend in prices is still slightly -- very slightly -- higher.

This post is up at XE.com.

Tuesday, September 26, 2017

Despite the hurricanes, the slowdown in the housing market is real

- by New Deal democrat

I'll have a detailed post up tomorrow, but the takeaway from this morning's report on new home sales is that, even when we delete the hurricane-affected South, new home sales cotninue to be down from their March peak.

Further, median prices in August actually turned negative YoY. It appears that the lack of affordability may finally be having a significant effect on the market. Note that even though lack of affordability probably is what mainly causes sales downturns, typically the sales downturn shows up first before sellers get the message and begin to lower prices.

More tomorrow, with graph-y and chart-y goodness.

Monday, September 25, 2017

A hurricane workaround for industrial production

- by New Deal democrat

Last week I mentioned that the regional Fed surveys plus the Chicago PMI can be used as a workaround to account for the effects of hurricanes on Industrial Production. It isn't pretty and by no means is it perfect, but for the (hopefully only) two or three months that we need it, we can use the workaround to give us the underlying trend in production, particularly for manufacturing.

This is a two-step correlation.

The first correlation is between the regional Fed indexes and the ISM manufacturing index. This is something Bill McBride, a/k/a Calculated Risk, has been keeping track of for years. Here's his graph going back all the way to 2000:

While the correlation isn't perfect, most notably in the years 2010 and 2011, when the regional Fed average was high, and in 2015 and 2016, when it was too low, in general it holds, with the two rising or falling between positive and negative in tandem, even if we just use the Empire State and Philly indexes.

The second step is that the ISM manufacturing index similarly correlates well with, and slightly leads industrial production:

Again this is a pretty good correlation, even if the ISM manufacturing index was much higher than production in 2004, and somewhat higher generally since 2013.

Unfortunately FRED doesn't publish the regional Fed indexes, so I can't show you a direct graphic comparison, but what I can do is give you a quarterly sampling of the monthly average of each going back to the "shallow industrial recession" of 2015.

To do this I am averaging the Empire State, Philly, Richmond, and Kansas City indexes, along with the Chicago PMI. Since Chicago uses a different scale (where 50 is "neutral"), to include that I subtract 50 and then double the result. I omit the Dallas index, since that includes the Houston area. Florida is in the Atlanta Fed district, which doesn't have a manufacturing index.

Here's the result:

| Quarter | Industrial Production | Ind. Pro. Manufacturing | Regional Fed +Chi PMI Average | Reg. Fed. Avg. /5 |

|---|---|---|---|---|

| Dec 2015 | -.9 | -.2 | -.35.8 | -.7 |

| Mar 2016 | -.3 | +.3 | +32.3 | +.6 |

| Jun 2016 | -.2 | -.2 | +16.4 | +.3 |

| Sep 2016 | +.2 | 0 | +16.8 | +.3 |

| Dec 2016 | +.2 | +.4 | +50.7 | +1.0 |

With the exception of March, which was greatly affected by a positive Richmond Fed outlier, the regional Fed indexes caught the rising trend in manufacturing from negative to positive, and especially positive at the end of the year.

Here is the monthly chart for this year so far:

Here is the monthly chart for this year so far:

| Month | Industrial Production | Ind. Pro. Manufacturing | Regional Fed +Chi PMI Average | Reg. Fed. Avg. /5 |

|---|---|---|---|---|

| Jan | -.3 | +.4 | +10.3 | +.2 |

| Feb | +.2 | +.3 | +21.6 | +.4 |

| Mar | +.2 | +.3 | +21.3 | +.4 |

| Apr | +1.1 | +.4 | +14.2 | +.3 |

| May | +.1 | -.5 | +13.1 | +.3 |

| Jun | +.2 | +.2 | +19.4 | +.4 |

| Jul | +.4 | 0 | +20.2 | +.4 |

| Aug | -.9* | -.3* | +24.4 | +.5 |

| Sep** | n/a | n/a | +24.1 (2 reports) | +1.2 |

*affected by Hurricane Harvey

**so far this month

While this is nowhere near a 1:1 correlation, as I said at the outset this is good enough to communicate the overall trend for the next several months until the hurricane effects recede.

Since both the Regional Fed indexes and the ISM manufacturing index have somewhat outperformed Industrial Production this year, to be confident that a positive average of regional Fed indexes translates into a positive hurricane-adjusted industrial production report, we probably want to see a reading of at least +.3. Even doing so, for August -- and so far in September -- the underlying trend remains positive.

Since both the Regional Fed indexes and the ISM manufacturing index have somewhat outperformed Industrial Production this year, to be confident that a positive average of regional Fed indexes translates into a positive hurricane-adjusted industrial production report, we probably want to see a reading of at least +.3. Even doing so, for August -- and so far in September -- the underlying trend remains positive.

Sunday, September 24, 2017

A thought for Sunday: the most important issue in the 2016 election was . . .

- by New Deal democrat

This is a post I've been meaning to write for several months. For a while after the election last year, there was a debate about whether the "economic anxiety" in the (white) working class was the most important factor vs. was it simply a matter of racism. The consensus has nearly settled on the narrative that racism was decisive, to the point where "economic anxiety" has become a taunt, and some who embrace identity politics actively disparage progressive economic issues.

I'm here to show you data that - in part - disputes that consensus. What was the most important issue in the 2016 presidential election? The below data on that issue all comes from the Voter Study Group, from its survey published several months ago: "Insights from the 2016 Voter survey."

I'm here to show you data that - in part - disputes that consensus. What was the most important issue in the 2016 presidential election? The below data on that issue all comes from the Voter Study Group, from its survey published several months ago: "Insights from the 2016 Voter survey."

In the below graphs, the potency of various issues are examined in terms of how well they lined up on a liberal/conservative or favorable/unfavorable axis, but for simplicity's sake it is pretty clear that they correlate with a vote for Clinton (left) or Trump (right). The more vertical the line, the more decisive the factor, whereas a horizontal line means that the factor made essentially no difference in whether a vote was for one candidate or the other. the 2016 results are in red, vs. the 2012 results in gray. What I've done is to delete the names of the nine factors they tested, so you won't be swayed by any pre-existing opinion you might have had about the factor. Here they are:

I'll give away one finding right away. The most decisive factor, shown at the right of the lowermost column, is party affiliation. D's voted for Clinton. R's voted for Trump.

But after that, it's pretty clear that the close runner-up for most decisive factor in how people voted is the issue at the left of the middle column, which was ...

the economy!

That's right. The single most decisive factor in the 2016 vote was how people felt about the economy.

How can that be true? After all, haven't we all heard that racism was dispositive?

The clue is in the difference in slope between the red and gray lines. Even though the economy was the single most important issue in 2016, it was relatively *less* important than it was in 2012. Graphically it was less vertical in 2016 than 2012. And the difference disfavored democrats. The economy was equally dispositive for conservatives, but less dispositive for liberals. Put another way, economic progressives voted less in lock-step on the economy in 2016 than they did in 2012.

And where did those votes go in 2016? The three issues in the top column, and especially the issue at the top left.

But let's take them in reverse order. The issue at the top right is nearly horizontal -- i.e., it made little difference to voters, but while it didn't motivate progressives at all, it did have a slight affect on conservative votes compared with 2012. That issue is:

attitudes towards Muslims.

The issue at the top middle had some effect both in 2012, but moreso in 2016. It motivated both conservatives and progressives, but conservatives relatively more. That issue is:

attitudes towards black people. There more than anywhere is your racism, and while the issue did drive progressive voters to Clinton, it drove even more racist voters to Trump.

This is an unfortunate dynamic for the left. What it appears to mean is, both progressives and conservatives were motivated by the "Black Lives Matter" movement and protests against police violence. But while the protests may have convinced some progressives, they drove EVEN MORE CONSERVATIVES to harden, and act on, their racial views. In other words, in electoral terms the protest movement was actually COUNTERproductive.

Finally, here is the social issue (top left among the nine) which most drove voter behavior in 2016 compared with 2012:

attitudes towards immigration. Note that, it too motivated both progressives and conservatives, and it too was more decisive in voting behavior on the right than on the left.

To get to the heart of the matter, it wasn't racism per se which drove the electoral college victory to Trump. It was Xenophobia, and anger in particular directed at illegal aliens. While probably about half of the Muslim immigrants to the US come from countries in the Middle East and are white, many also are from places like south Asia and are not white. Yet feelings about Muslims barely moved the needle.

Further, if it were racism per se which was most dispositive, we would expect to see a bigger correlation with feelings towards black people than feelings towards immigrants. Not only was that not the case, but the *reverse* was true.

In an article only a week after the election, Loren Collingwood wrote in the Washington Post that:

I also found evidence consistent with the "racial threat" hypothesis. As shown by the orange dotted line in the graph, Trump’s vote was higher in counties where the number of Latinos has increased significantly since 2000. This suggests that some voters may have supported Trump as a way of expressing white identity in an increasingly diverse nation.

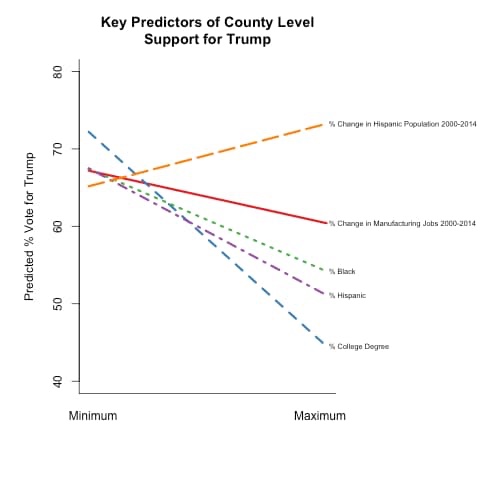

... Trump also did better in counties experiencing a loss in manufacturing since 2000.

Here's her graph:

It's worth noting that the unemployment rate among Latinos (I'm using men in the non-seasonal adjusted graph below) has declined further - from an admittedly higher peak - in this expansion than that among whites:

At the height of the tech boom in 1999, male Latino unemployment was 1.3% higher than that of white males. In 2006 and again in June of this year, it was only 0.1% higher.

Since roughly 11 million, or 1/4 of the total Latino population, are illegals/undocumented workers, it is not difficult to imagine whites (and maybe some blacks) seething that illegals have taken some of their jobs, in a very long and still-incomplete recovery. Is that "economic anxiety" or racism or Xenophobia, or both?

And by the way, a similar dynamic about the volume and nature of immigation, by the way, appears to be behind the big decline in the center left Social Democratic parties of Europe.

Further, I wish I had kept the cite, but I recall reading stories of white working class voters who went to Trump rallies and participated in all of the chants, who supported him in part because they didn't take his racial rhetoric seriously. They treated it as all part of the show. The distinction is worth emphasizing -- if I am a minority, I may not like a person who is willing to overlook that racial rhetoric, but it is different from a person who actually *agrees with* that racial rhetoric. More succinctly, if it comes down to whether you win or lose political power, you may be dead set against compromising with the latter, but what about the former?

I think there are three big lessons here for future elections:

- Even if you want to embrace the importance of social issues, you simply cannot ignore the economy, which remains the single most important issue to most voters. As I have pointed out a number of times, econometric models did a very good job in 2016 forecasting a narrow popular vote advantage for the incumbent party.

- Social issues should not be highlighted in ways which drive your supporters to the polls, but drive your opponents to the polls even more.

- While I unequivocally support a path to legalization, and ultimately citizenship, for DREAMers, it is crystal clear from the experiences in both the US an d Europe that progressive parties have to come to grips with reasonable restrictions on immigration, and enforcement of, immigration laws.

Saturday, September 23, 2017

Weekly Indicators for September 18 - 22 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

The biggest news was in purchase mortgage applications, hurricane adjusted jobless claims, and stock prices.

Friday, September 22, 2017

On August housing permits and starts, curb your enthusiasm

- by New Deal democrat

Hurricanes Harvey and Irma together affected over 10% of the housing market at minimum. That's one of three good reasons to take the good permits number with a grain of salt.

This is a two part post I have up at XE.com.

Part 1 is here.

Part 2 is here.

Thursday, September 21, 2017

Hurricane adjusted initial jobless claims for the week of September 9: 229,000

- by New Deal democrat

I am repeating an exercise I undertook in 2012 when Superstorm Sandy disrupted the initial claims data: estimating what the initial jobless claims would have been, but for the hurricanes.

In 2012 I created that adjustment by backing out the affected states (NY and NJ) from the non-seasonally adjusted data. That gave me the number of initial claims filed in the other 48 states. I compared that with the same metric one year earlier, and multiplied by the seasonal adjustment.

That gave me the number if the affected states had the same relative number of claims during the given week, as all of the unaffected states. In 2012, it showed that Sandy was not masking any underlying weakness in the economy.

The state by state data is released with a one week delay. So what follows is the analysis for the week of September 9, the number for which was reported one week ago and revised this week to 282,000. Last week I found the adjusted number for September 2 was 239,000. Last week I only had to back out Texas, but this week I have also backed out Florida.

Here is the table for the Week of September 10 in 2016 vs. September 9 this year:

Metric 2016 2017

Seasonally adjusted: 258,000 282,000

Adjustment for total: 1.33 1.33

Not seasonally adjusted: 193,291 212,284

Florida claims: 7,493 4,773 (!!! - yes, a decline this year)

Texas claims: 13,432 52,024

Texas claims: 13,432 52,024

NSA claims ex-TX+FL 202,008 155,487

TX+FL as % of total: 10.8% n/a

2017 w/ TX+FL adjustment: n/a 172,280

In both 2016 and 2017 the weekly seasonal adjustment was 1.33. Multiplying the non-seasonally adjusted total of 172,280, gives us the hurricane-adjusted initial jobless claims number for the week of September 9, 2017 of 229,000.

The underlying national trend in initial jobless claims remains very positive.

Wednesday, September 20, 2017

The asterisk in real median household income

- by New Deal democrat

This is a follow-up to the post I wrote last week about the latest data on real median household income.

One of the things I notes is that "households" includes the millions that are composed of retirees, a burgeoning demographic due both to healthier longevities and the demographics of the Boomer generation.

This morning Jared Bernstein helpfully includes a graph of real median household income excluding those over age 65:

Households headed by working age adults did finally surpass their 2007 income, but were still 3.4% below the all-time highs of incomes of 2000.

But mainly I wanted to follow up on that break in the graph in 2013. It was caused by a change in methodology by the Census Bureau.

But mainly I wanted to follow up on that break in the graph in 2013. It was caused by a change in methodology by the Census Bureau.

Here's the graph I ran last week of real median household incomes at various quintiles and deciles:

So I was surprised a few days later to see another, more pessimistic graph floating around, purporting to show that only the top 20% of households had higher incomes than in 2000:

Note that this graph doesn't have any break.

I traced the information back to its source, which turned out to be the Economic Policy Institute. And at the bottom of their article, I found a footnote explaining thus:

In other words, as best I can tell the E.P.I. simply took the 3.2% difference in the two methodologies in 2013 and projected it forward.

Now, let me state right up front that I don't know whether the data as represented by E.P.I. is correct or not.

But, neither does the E.P.I.

In fact, neither does anybody else, apparently including the Census Bureau itself.

That's because the Census Bureau hasn't provided data in any year since 2013 as to what the numbers would have been under their old methodology, so that we can form a basis of comparison.

By contrast, when the methodology for "real retail sales" was updated in the 1990s, the old data series continued to run for nearly 10 years, giving us an excellent basis for comparison, and confirming that the YoY changes were virtually identical, meaning that we can stitch the two series together confidently, giving us 70 years worth of data:

The Census Bureau didn't do that with real median household income, so there will *always* be a disconnect and a lack of ability to reliably and directly compare data from before 2013 with data afterward. We'll always be guessing.

This is a major problem for this important data series, and the Census Bureau should take steps, to the extent possible, to correct it.

Tuesday, September 19, 2017

Hurricane workarounds for industrial production and housing

- by New Deal democrat

Hurricane Harvey has already affected some of the August data releases. Irma has already started to affect some weekly releases, and will undoubtedly affect the September monthly releases.

I have already begun to adjust for the hurricanes in the case of initial jobless claims. But what of the monthly data?

While there is nothing so timely and precise as backing out affected states from the initial jobless claims report, there are workarounds that can at least tell us if there has been any significant change in trend for both the industrial production and housing reports.

I will put up separate posts, but to cut to the chase, we can use the Regional Fed reports (minus Dallas, and adding the Chicago PMI) to give us a reasonable estimate of industrial production in the non-hurricane affected areas. Similarly, we can make use the regional breakdowns in the housing report by subtracting the South and determining the trend in the remaining 60% of the country outside of that census region. I have already looked at this morning's housing report, and it turns out the effect is not what you would think! I'll have that post up by tomorrow.

Unfortunately there is no regional or state-by-state breakdown of retail sales or regional consumption expenditures on any sort of timely basis, so we're kind of stuck there.

Saturday, September 16, 2017

Weekly Indicators for September 11 - 15 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

The effects of Hurricane Harvey have shown up in a number of data series, but the underlying trends are intact.

Subscribe to:

Posts (Atom)