From the WSJ:

For the second month in a row, the Commerce Department reported a decline in spending on nonresidential construction -- which includes everything from hospitals to office parks to shopping malls. The report yesterday showed construction spending fell 1.7% in January from December, the steepest drop in 14 years. While residential construction accounted for a big part of the decline, spending on nonresidential construction slid 0.8%.

Meanwhile, there may be an oversupply of shopping malls and office buildings after a period of intensive construction. It adds up to bad news for employment, the economy and investors.

While the boom in commercial construction wasn't as dramatic as in home building, the impact of a slowdown on the economy could be significant. Nonresidential construction accounted for 3.6% of gross domestic product in the fourth quarter of 2007, up from 2.5% five years ago and the most since the second quarter of 1988, according to Moody's Economy.com.

As home construction got caught in a downward spiral last year, nonresidential construction continued to expand at a healthy clip. Spending on nonresidential structures rose 16% in 2007, the biggest four-quarter increase since 1984, according to Morgan Stanley.

Signs of trouble cropped up at the end of the year. As credit markets tightened, office space sold in the fourth quarter dropped 42% from a year earlier, and sales of large retail properties declined 31%, says Real Capital Analytics, a New York real-estate research group.

If spending continues to slow, construction workers, who are reeling from the housing slowdown, face more layoffs. Construction jobs made up 5.4% of nonfarm payrolls in January. While that's down from a peak of 5.7% in April 2006, it's still above the long-term average of 4.9%, say economists at Payden & Rygel in Los Angeles, leaving room for more job losses.

Let's flesh out this story with some graphs.

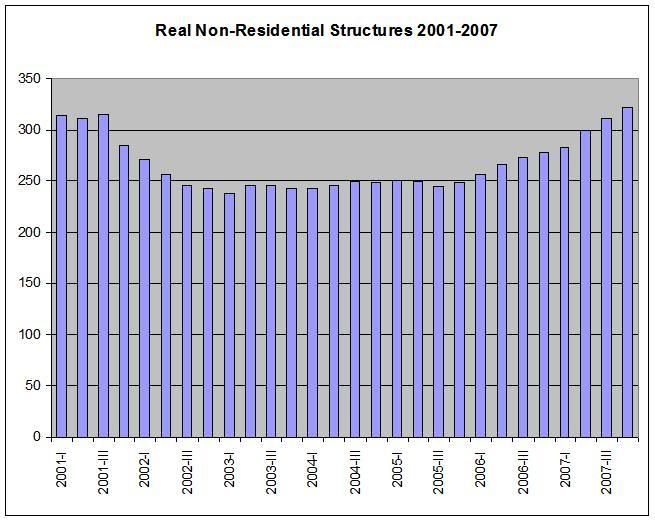

Above is a chart of real (inflation-adjusted) non-residential spending from the BEA.

Notice the steady increase over the last two years.

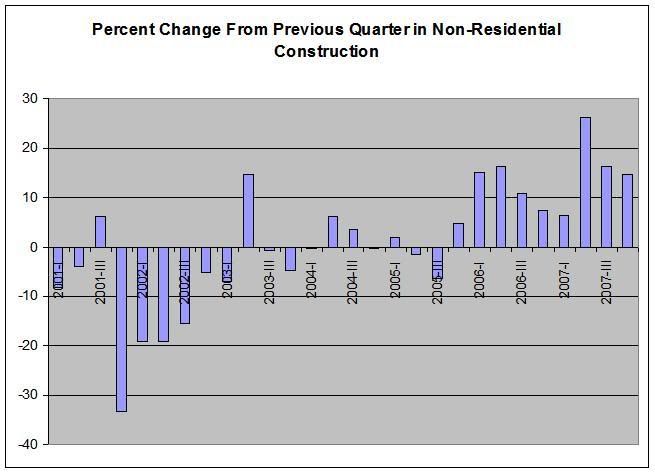

Above is the percentage change from the previous quarter in non-residential spending. Again, note the last two years have seen solid increases.

Let's look at the various REIT sectors that focus on commercial activities. These charts are from Prophet.net.

Office REITS are in a clear correction. There are two support lines in this 5-year chart, and the index has broken both of them. Currently prices are in a clear downward channel and are trading near 2005 levels.

Like the office REIT sector, the industrial REIT sector has broken a clear uptrend and is moving lower in a channel pattern right now.

Hotels have also broken the uptrend they were in for 5 years. They are also clearly correcting right now.

Here is an overview of construction employment:

Notice that construction employment has clearly turned lower over the last half year or so.

Let's look at some graphs from the latest Quarterly Banking Profile.

Commercial and industrial loans comprise 19% of total charge-offs.

While the non-current commercial and industrial loan percentage as ticked up slightly at institutions with less than 1 billion assets -- the uptick is incredibly slight and could just as easily be called statistical noise.

However, non-current commercial and industrial loans have been increasing for the last 5 quarters.

And the quarterly net charge off rates at institutions larger than $1 billion are clearly increasing.

So -- what does all of this information tell us?

1.) The GDP numbers tell us there has been a huge commercial (non-residential) build-out in the last few years. Paces of this magnitude cannot be sustained.

2.) The REIT charts tell us that traders are already concerned about the profit potential of this sector. Traders have already taken some of their profits off the table and aren't looking to get back in anytime soon.

3.) The employment picture tells us that employment is clearly declining. This chart also indicates that commercial construction was probably responsible for absorbing some of residential real estates construction job losses over the last few years. However, with residential in the tank these absorbed workers have no where to go job-wise.

4.) The banking information tells us that that credit quality is starting to deteriorate and that total net charge-offs are starting to hit the big banks ($1 billion and up) at an increasing rate in 2007. In other words, there are cracks in the commercial real estate lending world.