We'll be back on Monday. Until then:

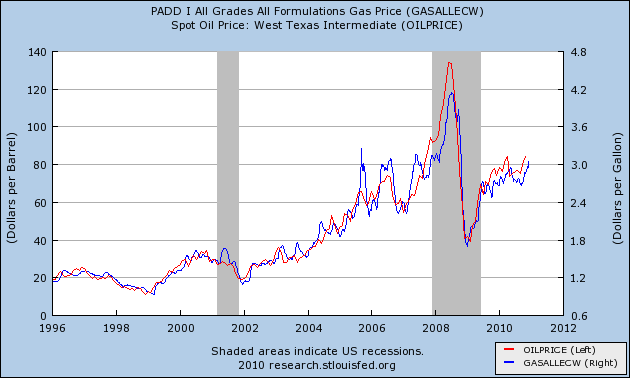

... U.S. total demand over the February through September period is growing at an even stronger pace, slightly over 500,000 barrels per day on average, or about 3 percent.The choke-collar applied by Oil prices to growth is a continuing an chronic problem, and bears continued close scrutiny.

.... U.S. year-over-year growth of almost 750,000 to over 900,000 barrels per day in August and September is of an order approaching, or even exceeding, growth levels seen in China. When the swing from huge declines last year to large third quarter growth levels observed this year is taken into account, the U.S. contribution to tightening global balances is considerable. Nevertheless, even given strong growth this year, U.S. oil demand remains well below peak levels seen in 2005

Treasury prices fell on Wednesday, pushing yields on 10-year notes to the highest level since June, as investors signal worry that the U.S. is not dealing with its budget deficit.

Yields on 10-year notes /quotes/comstock/31*!ust10y (UST10Y 3.26, -0.01, -0.40%) , which move inversely to prices, rose 10 basis points to 3.24%.The yields touched 3.34%, the highest level in six months and up from 2.94% on Monday -- still the biggest 2-day increase since June 2009 in late afternoon trading.

Yields on 2-year notes /quotes/comstock/31*!ust2yr (UST2YR 0.61, -0.02, -3.19%) rose 9 basis points to 0.62%, having touched the highest since July: 0.65%.

.....

On Tuesday, yields jumped by the most since June 2009 after the White House and Republicans revealed a tax-compromise bill that is expected to boost consumer spending and growth, but also increase the federal deficit and trigger more debt issuance. See story on Obama, tax deal.

So -- we have a rising stock market and declining bond market. This is usually the beginning of the second part of the market moves in a bull market. In the first, both Treasuries and stocks rally. Treasuries rally because there is still concern about the economy and little fear of an increase in rates, while equities rally in anticipation of recovery. In the second part of the rally, Treasuries start to sell off as the safe money starts to move into the riskier parts of the market.

how else Congress could spend $60 billion a year — the annual cost of extending the Bush tax cuts on income above $250,000 a year?From the NY Times News section, quoting the National Governors' Association, Sunday:

By the end of fiscal 2011, states estimate that they will have spent nearly $240 billion in Recovery Act funds. Within this temporary aid to states, $151 billion has been flexible funds (Medicaid and State Fiscal Stabilization Funds) that has helped states avoid draconian cuts. However, the wind down of these flexible funds in fiscal 2012 will result in a cliff of more than $65 billion.Maybe all those who lose their jobs or otherwise suffer from state and local budget cuts can get jobs polishing the billionaires' yachts.

With China’s debut in international standardized testing, students in Shanghai have surprised experts by outscoring their counterparts in dozens of other countries, in reading as well as in math and science, according to the results of a respected exam.

.....“I know skeptics will want to argue with the results, but we consider them to be accurate and reliable, and we have to see them as a challenge to get better,” he added. “The United States came in 23rd or 24th in most subjects. We can quibble, or we can face the brutal truth that we’re being out-educated.”

In math, the Shanghai students performed in a class by themselves, outperforming second-place Singapore, which has been seen as an educational superstar in recent years. The average math scores of American students put them below 30 other countries.

PISA scores are on a scale, with 500 as the average. Two-thirds of students in participating countries score between 400 and 600. On the math test last year, students in Shanghai scored 600, in Singapore 562, in Germany 513, and in the United States 487.

In reading, Shanghai students scored 556, ahead of second-place Korea with 539. The United States scored 500 and came in 17th, putting it on par with students in the Netherlands, Belgium, Norway, Germany, France, the United Kingdom and several other countries.

In science, Shanghai students scored 575. In second place was Finland, where the average score was 554. The United States scored 502 — in 23rd place — with a performance indistinguishable from Poland, Ireland, Norway, France and several other countries.

US students are performing poorly in science and math -- the two subject areas that will lead to better jobs.

If you were a company that was looking to build a factory/manufacturing facility, where would you locate it? Frankly, offshoring to Asia makes sense because of the far better educated work force.

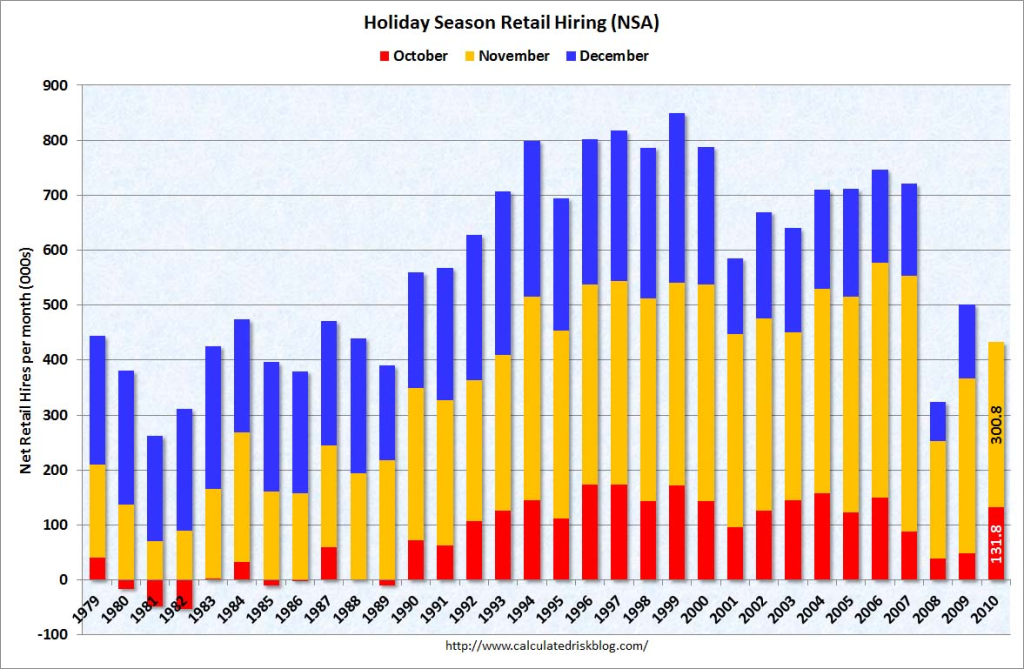

The economy is starting to fire on almost every cylinder these days but the one that matters most: Job creation.

Factories are busier. Incomes are rising. Autos are selling. The holiday shopping season is shaping up as the best in four years. Stock prices are surging.

And many analysts are raising their forecasts for the economy's growth. Goldman Sachs, for instance, just revised its gloomy prediction of a 2 percent increase in gross domestic product in 2011 to 2.7 percent and forecast 3.6 percent growth for 2012.

"The upward momentum has more traction this time," says James O'Sullivan, chief economist at MF Global.

If only every major pillar of the economy were faring so well.

Despite weeks of brighter economic news, employers still aren't hiring freely. The economy added a net total of just 39,000 jobs in November, the government said Friday.

That's far too few even to stabilize the unemployment rate, which rose from 9.6 percent in October to 9.8 percent last month. Unemployment is widely expected to stay above 9 percent through next year, in part because of the still-depressed real estate industry.

| Month | Job gains |

|---|---|

| Jan | +5 |

| Feb | +23 |

| Mar | +160 |

| Apr | +147 |

| May | +21 |

| Jun | +50 |

| Jul | +77 |

| Aug | +113 |

| Sep | +53 |

| Oct | +172(p) |

| Nov | +39(p) |

this is a clear step in the wrong direction. Considering the rate of job losses at the beginning of the year (600,000+/month) expecting an immaculate recovery is highly unrealistic. However, the bleeding has to stop at some point. So by the end of this year we have to be far lower than today's number for a recovery to be viable. Consumers cannot continue to hear news like this and expect to have a positive attitude about the economy. It's that simple.Two months later, that had been revised to -139,000, and November would ultimately be revised to +4,000, the first positive jobs report after the bottom of the Great Recession.

| Month | Initial | Final | net change |

|---|---|---|---|

| Jan | -20 | +14 | +34 |

| Feb | -36 | +39 | +75 |

| Mar | +162 | +208 | +46 |

| Apr | +250 | +313 | +63 |

| May | +431 | +432 | +1 |

| Jun | -125 | -175 | -50 |

| Jul | -131 | -66 | +75 |

| Aug | -54 | -1 | +53 |

| Sep | -95 | -24 | +71 |

| Oct | +151 | +172(p) | +21(p) |

| Nov | +39 |

| Month | Jobs | month/month change |

|---|---|---|

| Jan | 5317 | +3 |

| Feb | 5310 | -7 |

| Mar | 5321 | +11 |

| Apr | 5333 | +12 |

| May | 5337 | +4 |

| Jun | 5330 | -7 |

| Jul | 5352 | +22 |

| Aug | 5363 | +11 |

| Sep | 5410 | +17 |

| Oct | 5402(p) | +30(p) |

| Nov | 4319(p) | -8 (p) |

| Month | Jobs | month/month change |

|---|---|---|

| Jan | 14409.1 | +49.1 |

| Feb | 14416.2 | +7.1 |

| Mar | 14438.9 | +22.7 |

| Apr | 14453.3 | +14.4 |

| May | 14447.5 | -5.8 |

| Jun | 14431.3 | +16.2 |

| Jul | 14442.4 | +11.2 |

| Aug | 14448.8 | +6.4 |

| Sep | 1444,9 | -3.9 |

| Oct | 14457.9(p) | +13.0(p) |

| Nov | 14429.8(p) | -28.1(p) |

| Month | Initial | Final | net change |

|---|---|---|---|

| Jan | 42.1 | 49.1 | +7.0 |

| Feb | -0.4 | +7.1 | +7.5 |

| Mar | 14.9 | 22.7 | +7.8 |

| Apr | 12.4 | 14.4 | +2.0 |

| May | -6.6 | -5.8 | +0.8 |

| Jun | -6.6 | -16.2 | -10.2 |

| Jul | 6.7 | 11.2 | +4.5 |

| Aug | -4.9 | +6.4 | +11.3 |

| Sep | 5.7 | -3.9 | -9.6 |

| Oct | 27.9 | 13.0 | -14.9(p) |

{kind=link}

{kind=link}