Friday, September 19, 2008

Weekend Weimar and Beagle

I'm in Austin riding out the storm (isn't there an REO Speedwagon song in there?) so I don't have any pictures. I'll be back on Monday. Hopefully the weekend will give me the opportunity to digest everything that has happened this week.

Media Appearance

Tomorrow morning at 7:30 PCT I'll be on KTLK for at least half an hour (and probably and hour) to talk about the last week's happenings.

A Really Good Point

In the previous thread a commenter noted:

This is a very good point and one that needs to be seriously considered.

Right now the system is more than "unstable". It is in chaos as traders wait for the next shoe to drop. And the shoes of late have been getting larger and larger (Fannie/Freddie, AIG). At some point the shoe would be so large as to crush the system.

This begs the question -- at what point does financial instability/chaos become intolerable? I don't think there's an answer for that but it's a good question.

your ideological opposition to the idea of govt taking over banks is, i think, blinding you to the fact that in past instances (most notably the New Deal), such temporary takeovers have succeeded in stabilizing the banking system at least cost to the taxpayer.

This is a very good point and one that needs to be seriously considered.

Right now the system is more than "unstable". It is in chaos as traders wait for the next shoe to drop. And the shoes of late have been getting larger and larger (Fannie/Freddie, AIG). At some point the shoe would be so large as to crush the system.

This begs the question -- at what point does financial instability/chaos become intolerable? I don't think there's an answer for that but it's a good question.

Paulson's Statement

The entire statement is here.

Let's look at the speech in more detail

From a purely logical and technocratic perspective this analysis is very accurate. The Treasury is faced with a true lesser of two evils scenario: continue to deal with this situation on a case by case basis or make a comprehensive step to try and solve it. Either way they will be pilloried. Combine that with a Congress that is probably wetting their beds every night and this does make the most sense.

Earlier this week the WSJ had an article saying this was the worst situation since the great depression. Here is an excerpt from that article along with my commentary:

Above is a long and involved process that is incredibly painful. It is also very stop and start and will cause the markets a ton of anxiety which will lead to great uncertainty. A comprehensive plan will at least stop the bleeding and put the financial system on the road to recovery.

Back to the speech:

At least he gets that part right -- as opposed to blaming the CRA like every other wing nut on the planet.

First -- he's right. The central issue is everybody and their brother is holding assets that are illiquid (and not worth the paper they are printed on). They can't sell these things and they can't write them all off at once because of capital issues. As a result we get the scenario listed above -- fessing up to the bad debt, paying it off/writing it off and raising new capital.

On the surface I agree this is what has to be done. However, I reiterate a my objections as expressed in the Schumer story from last night.

1.) Where is this money going to come from?

2.) Will the companies who sell their assets be penalized?

3.) What is a bad debt?

4.) Will the purchase of these assets be non-political? (fat chance on that one)

5.) Will there be a maximum size of the fund?

6.) How long will the entity last?

7.) At a time when the US government is bleeding money it's going to spend more. Wonderful.

Let's look at the speech in more detail

We have acted on a case-by-case basis in recent weeks, addressing problems at Fannie Mae and Freddie Mac, working with market participants to prepare for the failure of Lehman Brothers, and lending to AIG so it can sell some of its assets in an orderly manner. And this morning we've taken a number of powerful tactical steps to increase confidence in the system, including the establishment of a temporary guaranty program for the U.S. money market mutual fund industry.

Despite these steps, more is needed. We must now take further, decisive action to fundamentally and comprehensively address the root cause of our financial system's stresses.

The underlying weakness in our financial system today is the illiquid mortgage assets that have lost value as the housing correction has proceeded. These illiquid assets are choking off the flow of credit that is so vitally important to our economy. When the financial system works as it should, money and capital flow to and from households and businesses to pay for home loans, school loans and investments that create jobs. As illiquid mortgage assets block the system, the clogging of our financial markets has the potential to have significant effects on our financial system and our economy.

From a purely logical and technocratic perspective this analysis is very accurate. The Treasury is faced with a true lesser of two evils scenario: continue to deal with this situation on a case by case basis or make a comprehensive step to try and solve it. Either way they will be pilloried. Combine that with a Congress that is probably wetting their beds every night and this does make the most sense.

Earlier this week the WSJ had an article saying this was the worst situation since the great depression. Here is an excerpt from that article along with my commentary:

At least three things need to happen to bring the deleveraging process to an end, and they're hard to do at once. Financial institutions and others need to fess up to their mistakes by selling or writing down the value of distressed assets they bought with borrowed money. They need to pay off debt. Finally, they need to rebuild their capital cushions, which have been eroded by losses on those distressed assets.

But many of the distressed assets are hard to value and there are few if any buyers. Deleveraging also feeds on itself in a way that can create a downward spiral: Trying to sell assets pushes down the assets' prices, which makes them harder to sell and leads firms to try to sell more assets. That, in turn, suppresses these firms' share prices and makes it harder for them to sell new shares to raise capital. Mr. Bernanke, as an academic, dubbed this self-feeding loop a "financial accelerator."

The first issue is huge because assets that were hard to value to begin with are trading an an illiquid market. That means the value is incredibly low -- if the owner can find a value at all. In other words -- this is the exact worst time to be trying too figure out what these instruments are worth.

Then remember that paying down debt takes money. Earnings are way down at financial institutions. The money they are getting for their assets is way low. So paying down debt is incredibly difficult.

And then there is rebuilding balance sheets. Who in their right minds would inject cash into any of these institutions? Their stock charts are all terrible and indicate traders are looking for bankruptcies across the board. The early round of infusions came last fall. Anyone else who puts money into one of these companies is going to ask for a ton of conditions.

Above is a long and involved process that is incredibly painful. It is also very stop and start and will cause the markets a ton of anxiety which will lead to great uncertainty. A comprehensive plan will at least stop the bleeding and put the financial system on the road to recovery.

Back to the speech:

As we all know, lax lending practices earlier this decade led to irresponsible lending and irresponsible borrowing. This simply put too many families into mortgages they could not afford. We are seeing the impact on homeowners and neighborhoods, with 5 million homeowners now delinquent or in foreclosure. What began as a sub-prime lending problem has spread to other, less-risky mortgages, and contributed to excess home inventories that have pushed down home prices for responsible homeowners.

At least he gets that part right -- as opposed to blaming the CRA like every other wing nut on the planet.

These illiquid assets are clogging up our financial system, and undermining the strength of our otherwise sound financial institutions. As a result, Americans' personal savings are threatened, and the ability of consumers and businesses to borrow and finance spending, investment, and job creation has been disrupted.

To restore confidence in our markets and our financial institutions, so they can fuel continued growth and prosperity, we must address the underlying problem.

The federal government must implement a program to remove these illiquid assets that are weighing down our financial institutions and threatening our economy. This troubled asset relief program must be properly designed and sufficiently large to have maximum impact, while including features that protect the taxpayer to the maximum extent possible. The ultimate taxpayer protection will be the stability this troubled asset relief program provides to our financial system, even as it will involve a significant investment of taxpayer dollars. I am convinced that this bold approach will cost American families far less than the alternative – a continuing series of financial institution failures and frozen credit markets unable to fund economic expansion.

First -- he's right. The central issue is everybody and their brother is holding assets that are illiquid (and not worth the paper they are printed on). They can't sell these things and they can't write them all off at once because of capital issues. As a result we get the scenario listed above -- fessing up to the bad debt, paying it off/writing it off and raising new capital.

On the surface I agree this is what has to be done. However, I reiterate a my objections as expressed in the Schumer story from last night.

1.) Where is this money going to come from?

2.) Will the companies who sell their assets be penalized?

3.) What is a bad debt?

4.) Will the purchase of these assets be non-political? (fat chance on that one)

5.) Will there be a maximum size of the fund?

6.) How long will the entity last?

7.) At a time when the US government is bleeding money it's going to spend more. Wonderful.

Read This Now

Barry at the Big Picture on the latest short selling BULLSHIT.

And this is complete and total BULLSHIT.

And this is complete and total BULLSHIT.

Federal Government Will Take Bad Assets

From the WSJ:

Paulson has a press conference at 10AM EST that will explain what is going on. Here are my issues on the surface:

1.) "Regulations are toooooooo complicated! Please stop!"

2.) The Federal government stops.

3.) "We made a lot of bad decisions. Please take these assets from us so the financial system doesn't fall apart!"

4.) Define "bad asset".

5.) What's the total amount the federal government is willing to commit?

Here are some conditions:

1.) Executives at any company that sells an asset can only take home 10 times what the lowest paid person in the company takes home.

2.) They have to buy their own health insurance

3.) The company cannot engage in any lobbying for the next 25 years.

The federal government is working on a sweeping series of programs that would represent perhaps the biggest intervention in financial markets since the 1930s, embracing the need for a comprehensive approach to the financial crisis after a series of ad hoc rescues.

At the center of the potential plan is a mechanism that would take bad assets off the balance sheets of financial companies, said people familiar with the matter, a device that echoes similar moves taken in past financial crises. The size of the entity could reach hundreds of billions of dollars, one person said.

Paulson has a press conference at 10AM EST that will explain what is going on. Here are my issues on the surface:

1.) "Regulations are toooooooo complicated! Please stop!"

2.) The Federal government stops.

3.) "We made a lot of bad decisions. Please take these assets from us so the financial system doesn't fall apart!"

4.) Define "bad asset".

5.) What's the total amount the federal government is willing to commit?

Here are some conditions:

1.) Executives at any company that sells an asset can only take home 10 times what the lowest paid person in the company takes home.

2.) They have to buy their own health insurance

3.) The company cannot engage in any lobbying for the next 25 years.

Thursday, September 18, 2008

Senator Schumer Proposes One Of the Dumbest Ideas Yet

From Bloomberg:

Why is this a dumb idea? Let me count the ways.

1.) Where is the money for this going to come from? I've detailed the proposed spending plans we've seen so far. They total $900 billion. Now we're going to pump more money into the system from some as yet unknown source.

2.) Just what will the government do with these interests? They're going to wind up the majority shareholder in some of these institutions -- and a minor big holder in others. Who will decide the government's policy?

3.) What is the criteria for investing in a company? If ever there was going to be a highly politicized process this is it. I can see it now ... "Senator from big important district gets huge cash infusion not because it's a good investment but because the Senator is in a close reelection bid and needs votes.

4.) Will the government ever get out of these companies? Will there be a time limit?

5.) Will there be a time limit for this entity's duration? Will it go on forever?

6.) Will the government become intimately involved with the company's internal deliberations and policy? Will Congressmen sit on various boards?

I could go on, but you get the idea. This is a disaster waiting to happen.

Treasury Secretary Henry Paulson and Federal Reserve Chairman Ben S. Bernanke are considering a new plan to address the credit crisis, said Senator Charles Schumer, who proposed an agency to pump capital into troubled banks.

``The Federal Reserve and the Treasury are realizing that we need a more comprehensive solution,'' Schumer, a Democrat who chairs the congressional Joint Economic Committee, told reporters in Washington today. ``I've been talking to them about it.''

Schumer urged forming an agency to inject funds into financial companies in exchange for equity stakes and pledges to rewrite mortgages and make them more affordable. His remarks indicate momentum is building for some wider plan after the Fed and Treasury's takeovers of Fannie Mae, Freddie Mac and American International Group Inc. this month.

Schumer advocated a Great Depression-era Reconstruction Finance Corp. model, different from the Resolution Trust Corp.- type plan others have floated. Another RTC, which was a 1990s agency that sold devalued assets in the Savings and Loan Crisis, would ``simply transfer excessive risk to the U.S. government without addressing the plight of homeowners,'' he said.

Treasury spokeswoman Michele Davis didn't immediately respond to a request for comment and Fed spokeswoman Michelle Smith declined to comment.

Why is this a dumb idea? Let me count the ways.

1.) Where is the money for this going to come from? I've detailed the proposed spending plans we've seen so far. They total $900 billion. Now we're going to pump more money into the system from some as yet unknown source.

2.) Just what will the government do with these interests? They're going to wind up the majority shareholder in some of these institutions -- and a minor big holder in others. Who will decide the government's policy?

3.) What is the criteria for investing in a company? If ever there was going to be a highly politicized process this is it. I can see it now ... "Senator from big important district gets huge cash infusion not because it's a good investment but because the Senator is in a close reelection bid and needs votes.

4.) Will the government ever get out of these companies? Will there be a time limit?

5.) Will there be a time limit for this entity's duration? Will it go on forever?

6.) Will the government become intimately involved with the company's internal deliberations and policy? Will Congressmen sit on various boards?

I could go on, but you get the idea. This is a disaster waiting to happen.

Today's Markets

On the daily chart notice the following:

-- The general trend since the end of August is down

-- All the shorter SMAs are heading lower

-- The shorter SMAs are below the longer SMAs

-- Prices are below all the SMAs

-- Prices have moved below the 117 level, but have bounced back to 120.

This is still a bearish chart. But the good news to today we saw the slide stop (at least for now).

Wednesday, September 17, 2008

A Look At The QQQQs and the IWMs

This is a chart of the IWMS -- the ETF that tracks the Russell 2000. It's a great proxy for the market's risk appetite in equities. This is a multi-year chart in weekly increments. Notice the following:

-- Prices clearly broke their multi-year uptrend that started in 2004

-- Prices have revolved around the 200 week SMA since the beginning of this year. However, prices are now below the 200 week SMA

-- Prices have bounced off the 38.2% Fibonacci level several times over the last year.

-- The weekly SMA picture is cloudy. They are bunched together with the averages within a few points of each other and the SMAs moving in different directions

This is a multi-year chart in weekly increments

Notice the following:

-- There are three primary trend lines. The QQQQs have broken through two: the upper trend line of the multi-year trading channel and the upward sloping trend line that started in mid-2006

-- Prices are now heading for the lower trend line of the multi-year upward sloping channel

-- Prices have just moved below the 200 day SMA.

WSJ: Worst Crisis Since the Depression

From the WSJ:

For the longest time there were all sorts of juicy rationalizations going on. It was contained to subprime; most people were paying their mortgages so everything was OK, it was a few bad apples in the bunch, everything outside of the financial sector was doing well. There were many more. But the problem -- as correctly seen primarily by the blogs -- was simple: the US went on a debt acquisition spree the likes of which we haven't seen for a really long time. But all of that debt has to go somewhere. As a result, everybody owns a little piece of this problem.

Who would have thought a year ago that the US would now basically be the biggest shareholder in AIG insurance? Or how about the massive bail-out of Freddie and Fannie? These are huge commitments of capital the likes of which we're just beginning to understand.

That's exactly what the problem is -- way too much debt that no one ever had any intention of paying back. Enter all sorts of great loan documentation schemes like "stated income loans" and the like. "Just tell us what you really want to make in your wildest dreams and we'll base out loan to you on that." Well, now we know what it has gotten us.

The first issue is huge because assets that were hard to value to begin with are trading an an illiquid market. That means the value is incredibly low -- if the owner can find a value at all. In other words -- this is the exact worst time to be trying too figure out what these instruments are worth.

Then remember that paying down debt takes money. Earnings are way down at financial institutions. The money they are getting for their assets is way low. So paying down debt is incredibly difficult.

And then there is rebuilding balance sheets. Who in their right minds would inject cash into any of these institutions? Their stock charts are all terrible and indicate traders are looking for bankruptcies across the board. The early round of infusions came last fall. Anyone else who puts money into one of these companies is going to ask for a ton of conditions.

Short version: this is going to take a lot longer than anyone wants to admit. Sometime over the last few weeks, Paul Krugman wrote he thought the next president will simply be going from financial crisis to financial crisis. I think that's about right.

Wouldn't that just be wonderful -- a new set of problems with an entire financial sector that is far more opaque than any publicly traded sector. That will just be a joy -- I simply can't wait for that shoe to drop.

Here's the shortest version of all: this isn't over by a long shot. And it stands a decent possibility of getting worse.

The financial crisis that began 13 months ago has entered a new, far more serious phase.

Lingering hopes that the damage could be contained to a handful of financial institutions that made bad bets on mortgages have evaporated. New fault lines are emerging beyond the original problem -- troubled subprime mortgages -- in areas like credit-default swaps, the credit insurance contracts sold by American International Group Inc. and others. There's also a growing sense of wariness about the health of trading partners.

For the longest time there were all sorts of juicy rationalizations going on. It was contained to subprime; most people were paying their mortgages so everything was OK, it was a few bad apples in the bunch, everything outside of the financial sector was doing well. There were many more. But the problem -- as correctly seen primarily by the blogs -- was simple: the US went on a debt acquisition spree the likes of which we haven't seen for a really long time. But all of that debt has to go somewhere. As a result, everybody owns a little piece of this problem.

The U.S. financial system resembles a patient in intensive care. The body is trying to fight off a disease that is spreading, and as it does so, the body convulses, settles for a time and then convulses again. The illness seems to be overwhelming the self-healing tendencies of markets. The doctors in charge are resorting to ever-more invasive treatment, and are now experimenting with remedies that have never before been applied. Fed Chairman Bernanke and Treasury Secretary Henry Paulson, walking into a hastily arranged meeting with congressional leaders Tuesday night to brief them on the government's unprecedented rescue of AIG, looked like exhausted surgeons delivering grim news to the family.

Who would have thought a year ago that the US would now basically be the biggest shareholder in AIG insurance? Or how about the massive bail-out of Freddie and Fannie? These are huge commitments of capital the likes of which we're just beginning to understand.

Fed and Treasury officials have identified the disease. It's called deleveraging, or the unwinding of debt. During the credit boom, financial institutions and American households took on too much debt. Between 2002 and 2006, household borrowing grew at an average annual rate of 11%, far outpacing overall economic growth. Borrowing by financial institutions grew by a 10% annualized rate. Now many of those borrowers can't pay back the loans, a problem that is exacerbated by the collapse in housing prices. They need to reduce their dependence on borrowed money, a painful and drawn-out process that can choke off credit and economic growth.

That's exactly what the problem is -- way too much debt that no one ever had any intention of paying back. Enter all sorts of great loan documentation schemes like "stated income loans" and the like. "Just tell us what you really want to make in your wildest dreams and we'll base out loan to you on that." Well, now we know what it has gotten us.

At least three things need to happen to bring the deleveraging process to an end, and they're hard to do at once. Financial institutions and others need to fess up to their mistakes by selling or writing down the value of distressed assets they bought with borrowed money. They need to pay off debt. Finally, they need to rebuild their capital cushions, which have been eroded by losses on those distressed assets.

But many of the distressed assets are hard to value and there are few if any buyers. Deleveraging also feeds on itself in a way that can create a downward spiral: Trying to sell assets pushes down the assets' prices, which makes them harder to sell and leads firms to try to sell more assets. That, in turn, suppresses these firms' share prices and makes it harder for them to sell new shares to raise capital. Mr. Bernanke, as an academic, dubbed this self-feeding loop a "financial accelerator."

The first issue is huge because assets that were hard to value to begin with are trading an an illiquid market. That means the value is incredibly low -- if the owner can find a value at all. In other words -- this is the exact worst time to be trying too figure out what these instruments are worth.

Then remember that paying down debt takes money. Earnings are way down at financial institutions. The money they are getting for their assets is way low. So paying down debt is incredibly difficult.

And then there is rebuilding balance sheets. Who in their right minds would inject cash into any of these institutions? Their stock charts are all terrible and indicate traders are looking for bankruptcies across the board. The early round of infusions came last fall. Anyone else who puts money into one of these companies is going to ask for a ton of conditions.

Goldman Sachs Group Inc. economist Jan Hatzius estimates that in the past year, financial institutions around the world have already written down $408 billion worth of assets and raised $367 billion worth of capital.

But that doesn't appear to be enough. Every time financial firms and investors suggest that they've written assets down enough and raised enough new capital, a new wave of selling triggers a reevaluation, propelling the crisis into new territory. Residential mortgage losses alone could hit $636 billion by 2012, Goldman estimates, triggering widespread retrenchment in bank lending. That could shave 1.8 percentage points a year off economic growth in 2008 and 2009 -- the equivalent of $250 billion in lost goods and services each year.

"This is a deleveraging like nothing we've ever seen before," said Robert Glauber, now a professor of Harvard's government and law schools who came to Washington in 1989 to help organize the savings and loan cleanup of the early 1990s. "The S&L losses to the government were small compared to this."

Short version: this is going to take a lot longer than anyone wants to admit. Sometime over the last few weeks, Paul Krugman wrote he thought the next president will simply be going from financial crisis to financial crisis. I think that's about right.

Hedge funds could be among the next problem areas. Many rely on borrowed money to amplify their returns. With banks under pressure, many hedge funds are less able to borrow this money now, pressuring returns. Meanwhile, there are growing indications that fewer investors are shifting into hedge funds while others are pulling out. Fund investors are dealing with their own problems: Many have taken out loans to make their investments and are finding it more difficult now to borrow

Wouldn't that just be wonderful -- a new set of problems with an entire financial sector that is far more opaque than any publicly traded sector. That will just be a joy -- I simply can't wait for that shoe to drop.

Here's the shortest version of all: this isn't over by a long shot. And it stands a decent possibility of getting worse.

Central Banks Take Coordinated Action

From the WSJ:

Here's what's really going on:

The world's major central banks banded together Thursday to flood global money markets with massive amounts of U.S. dollars, in hopes of taming a major source of the tensions rocking the financial system.

The U.S. Federal Reserve said Thursday it will expand or introduce measures to shuttle dollars to major European central banks, the Bank of Canada and the Bank of Japan, so these central banks can provide financial institutions in their respective markets with short-term dollar funding. Among commercial banks' general scramble for short-term cash in recent days, tensions in dollar-denominated money markets have been particularly fierce.

.....

The Fed boosted its U.S. dollar swap line with foreign central banks by $180 billion. The European Central Bank, which has had a swap line with the Fed in place since December, increased its line to up to $110 billion from $55 billion. The Swiss central bank swap line also got a boost to $27 billion from $12 billion before. With the expanded swap lines, the ECB and Swiss National Bank will up the amount of dollars they offer for 28 and 84 days in auctions they hold every other week.

Here's what's really going on:

And Yet More Shit Hits the Fan

From the NY Times:

And that's not all:

I have to admit that at this point I am breathless. It feels like the dam has burst and all the bad news is flooding into the streets. The struggling financial players -- which is practically everybody -- are all desperately trying to find the chair to sit in now that the music has stopped. However, the person who will eventually wind up paying for all of this is the US taxpayer.

Washington Mutual, the struggling savings and loan, has been working on several efforts to save itself, including a potential sale, people briefed on the matter said Wednesday.

Goldman Sachs, which Washington Mutual has hired, started the process several days ago, these people said. Among the potential bidders that Goldman has talked to are Wells Fargo, JPMorgan Chase and HSBC. But no buyers may materialize. That could force the government to place Washington Mutual into conservatorship, like IndyMac, or find a bridge-bank solution, which was extended to thrifts in the new housing regulations.

Citigroup is also considering an offer, but would likely be able to buy Washington Mutual only if it emerged from a receivership, according to a person close to the situation. JPMorgan is maintaining its posture that it will not bid unless it receives government support, according to another person briefed on the matter.

And that's not all:

Morgan Stanley, one of the two last major American investment banks, is considering a merger with the Wachovia Corporation or another bank, according to people briefed on the discussions.

The Morgan Stanley chief executive, John J. Mack, received a telephone call on Wednesday from Wachovia expressing interest in the Wall Street bank. Morgan Stanley is considering other options as well. Other banks have also expressed interest in Morgan Stanley.

The talks are preliminary and no deal may emerge.

Wachovia declined to comment.

Shares of Wachovia fell 20.76 percent, or $2.39, to $9.12; Morgan Stanley declined 24.22 percent, or $6.95, to $21.75.

I have to admit that at this point I am breathless. It feels like the dam has burst and all the bad news is flooding into the streets. The struggling financial players -- which is practically everybody -- are all desperately trying to find the chair to sit in now that the music has stopped. However, the person who will eventually wind up paying for all of this is the US taxpayer.

Today's Markets

A few days ago I noted that 120 was an important technical level. When prices moved below that level we needed to fine other technical levels where possible support might exist. So, here is a 7 year chart in weekly increments to locate technical support. Notice the following:

-- The 50% retracement level for the rally that lasted from '03 - '07 is above the current level. I've always used the 50% level as an approximate level -- meaning 118.231 is plus or minus a few points. So today's close at $116.59 is still close enough to the 118 level to be in the 50% retracement ballpark for me. However, another day like today and we've got major problems.

-- We have a fair amount of technical support around 115.

-- After 115 we've got 110 to look forward tool.

-- In a recent look at the markets I pointed out that the really long-term view of the SPYs is the 2007 peak was in fact the second top in a 10 year double top formation. Assuming that to be the technical case in combination where an economy clearly going into another fundamental downturn and we've got serious problems.

On the daily chart, notice the following:

-- All the SMAs are moving lower

-- The shorter SMAs are below the longer SMAs

-- Prices are below all the SMAs

Bottom line: this chart in combination with the multi-year chart and the underlying fundamentals indicates we've got serious problems.

My Bad -- It's $900 Billion We're On the Hook For

From CNBC:

- $200 billion for Fannie Mae [FNM 0.42 -0.061 (-12.68%) ] and Freddie Mac [FRE 0.26 --- UNCH (0) ]. The Treasury will inject up to $100 billion into each institution by purchasing preferred stock to shore up their capital as needed. The deal puts the two housing finance firms under government control.

- $300 billion for the Federal Housing Administration to refinance failing mortgage into new, reduced-principal loans with a federal guarantee, passed as part of a broad housing rescue bill.

- $4 billion in grants to local communities to help them buy and repair homes abandoned due to mortgage foreclosures.

- $85 billion loan for AIG [AIG 2.06 -1.69 (-45.07%) ], which would give the Federal government a 79.9 percent stake and avoid a bankruptcy filing for the embattled insurer. AIG management will be dismissed.

- At least $87 billion in repayments to JPMorgan Chase [JPM 38.12 -2.62 (-6.43%) ] for providing financing to underpin trades with units of bankrupt investment bank Lehman Brothers [LEH 0.11 -0.19 (-62.37%) ]. U.S. Treasury Secretary Henry Paulson said over the weekend he was adamant that public funds not be used to rescue the firm.

- $29 billion in financing for JPMorgan Chase's government-brokered buyout of Bear Stearns in March. The Fed agreed to take $30 billion in questionable Bear assets as collateral, making JPMorgan liable for the first $1 billion in losses, while agreeing to shoulder any further losses.

- At least $200 billion of currently outstanding loans to banks issued through the Fed's Term Auction Facility, which was recently expanded to allow for longer loans of 84 days alongside the previous 28-day credits.

Just When You Thought It Couldn't Get Any Worse...

From Reuters:

Let's look at the stock chart:

That chart says one thing: traders think Washington Mutual is heading for bankruptcy. Period.

According to Reuter's WAMU has lost money the last three quarters. According to the publicly available balance sheet, there are $241 billion in loans, which comprise 73.70% of the company's assets. And that is where the problem is. Consider the following graphs from the latest Quarterly Banking Profile from the FDIC:

Those charts say the trend will get worse. Which means WAMU may be the next company on the chopping block. Or any other bank that still has loans outstanding....

U.S. federal regulators recently called a number of banks asking if they would consider buying Washington Mutual Inc (WM.N) should it eventually falter, the New York Post said, citing sources.

Federal banking regulators, in recent days, contacted Wells Fargo & Co (WFC.N), JPMorgan Chase & Co (JPM.N), HSBC (HSBA.L) and several other financial institutions to gauge their interest in a possible acquisition of WaMu, the paper said.

No merger discussions are currently under way between the Seattle-based bank and anyone else, the sources told the paper.

Let's look at the stock chart:

That chart says one thing: traders think Washington Mutual is heading for bankruptcy. Period.

According to Reuter's WAMU has lost money the last three quarters. According to the publicly available balance sheet, there are $241 billion in loans, which comprise 73.70% of the company's assets. And that is where the problem is. Consider the following graphs from the latest Quarterly Banking Profile from the FDIC:

Those charts say the trend will get worse. Which means WAMU may be the next company on the chopping block. Or any other bank that still has loans outstanding....

The AIG Deal In Detail

First, please see the article I wrote yesterday on AIG, titled "Is AIG Too Big To Fail?" The short version is, well, yes it is. Let's look at the deal specifics.

First, the government is making a loan valued at $85 billion. This is on top of a loan of up to $200 billion for Freddie and Fannie and backstopping the Bear Stearns deal for $30 billion. That's a total of a possible $315 billion the government has put on the line so far. That's 11.54% of the 2007 federal budget. This at a time when the federal government has been bleeding money since 2003:

09/30/2007 $9,007,653,372,262.48

09/30/2006 $8,506,973,899,215.23

09/30/2005 $7,932,709,661,723.50

09/30/2004 $7,379,052,696,330.32

09/30/2003 $6,783,231,062,743.62

09/30/2002 $6,228,235,965,597.16

09/30/2001 $5,807,463,412,200.06

09/30/2000 $5,674,178,209,886.86

The current total is $9,634,090,464,815.55

SO -- the US government which is already run about as incompetently as possible -- is now loaning more money. What's a few more billion when you can pawn off the problems on the US taxpayer.

The government is getting a 79.9% interest -- clearly a majority interest. As Bloomberg noted:

In short -- the government is now the owner of an insurance company. Great. They've done such a great job so far with everything else.

AIG is paying a hefty insurance rate:

This is probably in line with where AIG should be paying interest rates for a loan. They bottom line is they should be forced into bankruptcy at this point, which is essentially the business plan for the foreseeable future:

So, to sum up --

1.) The deal makes the US government the owner of an insurance company

2.) The US government has already promised outlays of 11% of the 2007 budget at a time when the government is bleeding money

3.) AIG is at paying a fair interest rate given their condition, and

4.) AIG is essentially in bankruptcy.

AIG made a ton money in the good times and now we're paying for their excesses.

The U.S. negotiators drove a hard bargain. Under terms hammered out Tuesday night, the Fed will lend up to $85 billion to AIG, and the U.S. government will effectively get a 79.9% equity stake in the insurer in the form of warrants called equity participation notes. The two-year loan will carry an interest rate of Libor plus 8.5 percentage points. (Libor, the London interbank offered rate, is a common short-term lending benchmark.)

The loan is secured by AIG's assets, including its profitable insurance businesses, giving the Fed some protection even if markets continue to sink. And if AIG rebounds, taxpayers could reap a big profit through the government's equity stake.

"This loan will facilitate a process under which AIG will sell certain of its businesses in an orderly manner, with the least possible disruption to the overall economy," the Fed said in a statement.

It puts the government in control of a private insurer -- a historic development, particularly considering that AIG isn't directly regulated by the federal government. The Fed took the highly unusual step using legal authority granted in the Federal Reserve Act, which allows it to lend to nonbanks under "unusual and exigent" circumstances, something it invoked when Bear Stearns Cos. was rescued in March.

As part of the deal, Treasury Secretary Henry Paulson insisted that AIG's chief executive, Robert Willumstad, step aside. Mr. Paulson personally told Mr. Willumstad the news in a phone call on Tuesday, according to a person familiar with the call.

First, the government is making a loan valued at $85 billion. This is on top of a loan of up to $200 billion for Freddie and Fannie and backstopping the Bear Stearns deal for $30 billion. That's a total of a possible $315 billion the government has put on the line so far. That's 11.54% of the 2007 federal budget. This at a time when the federal government has been bleeding money since 2003:

09/30/2007 $9,007,653,372,262.48

09/30/2006 $8,506,973,899,215.23

09/30/2005 $7,932,709,661,723.50

09/30/2004 $7,379,052,696,330.32

09/30/2003 $6,783,231,062,743.62

09/30/2002 $6,228,235,965,597.16

09/30/2001 $5,807,463,412,200.06

09/30/2000 $5,674,178,209,886.86

The current total is $9,634,090,464,815.55

SO -- the US government which is already run about as incompetently as possible -- is now loaning more money. What's a few more billion when you can pawn off the problems on the US taxpayer.

The government is getting a 79.9% interest -- clearly a majority interest. As Bloomberg noted:

The Federal Reserve will provide a two-year loan, take 79.9 percent of the New York-based company's stock and replace its management because ``a disorderly failure of AIG could add to already significant levels of financial market fragility,'' according to a statement by the central bank late yesterday

In short -- the government is now the owner of an insurance company. Great. They've done such a great job so far with everything else.

AIG is paying a hefty insurance rate:

The government is lending AIG the money at 8.5 percentage points above the three-month London interbank offered rate, or a current rate of about 11.5 percent.

This is probably in line with where AIG should be paying interest rates for a loan. They bottom line is they should be forced into bankruptcy at this point, which is essentially the business plan for the foreseeable future:

The agreement will give the company, which sells insurance in more than 130 countries, time to sell assets ``on an orderly basis,'' AIG said in a statement. Chief Executive Officer Robert Willumstad, 63, will be replaced by former Allstate Corp. CEO Edward Liddy, 62, according to a person familiar with the plans, who declined to be identified because the change hadn't been formally announced

So, to sum up --

1.) The deal makes the US government the owner of an insurance company

2.) The US government has already promised outlays of 11% of the 2007 budget at a time when the government is bleeding money

3.) AIG is at paying a fair interest rate given their condition, and

4.) AIG is essentially in bankruptcy.

AIG made a ton money in the good times and now we're paying for their excesses.

Tuesday, September 16, 2008

Today's Markets

Earlier today I noted that prices had moved below 120 which is a technically important level. Prices increased from below the 120 level to above the 120 at the close. They did this on incredibly high volume, which is technically a good sign. However, note the following:

-- Prices are below all the SMAs

-- All the SMAs are headed lower

-- Shorter SMAs are below longer SMAs

-- Prices are below the 200 day SMA

Bottom line, this is still a pretty ugly chart.

The main issue gong forward is AIG. While there have been plenty of rumors, nothing firm has emerged. When that is solved, I would expect a relief rally.

Is AIG Too Big to Fail?

From Bloomberg:

Let's back-up a bit and look at this situation in a bit more detail.

Wall Street's top firms, and the biggest companies in Europe and Asia, have bought protection on $441 billion of fixed-income assets from AIG to guard their investments against potential bankruptcies.

These are "credit default swaps". While they sound exotic they aren't. They are essentially insurance on corporate bonds. Suppose you manage a bond portfolio and you want to hedge your risk. If you were an equity trader you would sell an out of the money put.

But no such option exists for bond managers. This led to the rise of the "credit default swap" (CDS) market. These are simply options on bonds, or an option to sell x amount of bonds at a certain price at a certain time. They are a great development because they allow fixed income managers to hedge downside risk. But (and here's the big but) the market is off balance sheet and unregulated. Because the market is private there is no way to limit it's size to an appropriate size. Put another way, suppose you had $10,000,000 in bonds that you wanted to insure. There is no reason for there to be numerous contracts on this bond position -- one will do. But because this is a private market there is no way to know if there are multiple options on the same bonds. This is one of the reasons why the CDS market is currently dangerous. Because AIG is so intimately involved with this market they have essentially become "too big to fail".

Barry over at the Big Picture noted one of the reasons why the Fed bailed out Bear Stearns is because the firm got so large it was too vital to the economy. That's essentially the case right now with AIG. It's too big to fail. This wasn't a deliberate strategy, but it is the result of a company getting really really big in an economy that is incredibly dependent on finance.

Mish described this situation as "Fed Sponsored Poker Party Morphs Into "Old Maid"". That's exactly what is happening. All the parties are deciding who will be stuck with the check for this thing.

A collapse of American International Group Inc., the insurer seeking to raise as much as $80 billion, would have consequences for financial firms around the globe, analysts and investors said.

Wall Street's top firms, and the biggest companies in Europe and Asia, have bought protection on $441 billion of fixed-income assets from AIG to guard their investments against potential bankruptcies. A failure by New York-based AIG may cause those protections to vanish. AIG also insures some of the largest assets in the world, doing business in more than 100 countries.

``They have tentacles into everything, and they are certainly critical to the ongoing health of the financial markets, or lack of health,'' Anton Schutz, president of Mendon Capital Advisors Corp. in Rochester, New York, said in an interview today with Bloomberg Television.

Wall Street's largest firms met at the New York Federal Reserve for a fifth day today, discussing ways to save AIG, said a spokesman for the New York Fed. AIG, with $1 trillion in assets, piled up net losses totaling $18.5 billion in the past three quarters on writedowns tied to the collapse of the U.S. subprime mortgage market.

``If AIG goes under, there could be a domino effect,'' said Andrea Cicione, a credit strategist at BNP Paribas SA in London. ``AIG is very connected to the financial system and it is very connected to the real economy.''

Let's back-up a bit and look at this situation in a bit more detail.

Wall Street's top firms, and the biggest companies in Europe and Asia, have bought protection on $441 billion of fixed-income assets from AIG to guard their investments against potential bankruptcies.

These are "credit default swaps". While they sound exotic they aren't. They are essentially insurance on corporate bonds. Suppose you manage a bond portfolio and you want to hedge your risk. If you were an equity trader you would sell an out of the money put.

Options are financial instruments that convey the right, but not the obligation, to engage in a future transaction on some underlying security, or in a futures contract. In other words, the holder does not have to exercise this right, unlike a forward or future.

For example, buying a call option provides the right to buy a specified quantity of a security at a set strike price at some time on or before expiration, while buying a put option provides the right to sell. Upon the option holder's choice to exercise the option, the party who sold, or wrote, the option must fulfill the terms of the contract.[1][2]

But no such option exists for bond managers. This led to the rise of the "credit default swap" (CDS) market. These are simply options on bonds, or an option to sell x amount of bonds at a certain price at a certain time. They are a great development because they allow fixed income managers to hedge downside risk. But (and here's the big but) the market is off balance sheet and unregulated. Because the market is private there is no way to limit it's size to an appropriate size. Put another way, suppose you had $10,000,000 in bonds that you wanted to insure. There is no reason for there to be numerous contracts on this bond position -- one will do. But because this is a private market there is no way to know if there are multiple options on the same bonds. This is one of the reasons why the CDS market is currently dangerous. Because AIG is so intimately involved with this market they have essentially become "too big to fail".

``They have tentacles into everything, and they are certainly critical to the ongoing health of the financial markets, or lack of health,'' Anton Schutz, president of Mendon Capital Advisors Corp. in Rochester, New York, said in an interview today with Bloomberg Television.

Barry over at the Big Picture noted one of the reasons why the Fed bailed out Bear Stearns is because the firm got so large it was too vital to the economy. That's essentially the case right now with AIG. It's too big to fail. This wasn't a deliberate strategy, but it is the result of a company getting really really big in an economy that is incredibly dependent on finance.

Wall Street's largest firms met at the New York Federal Reserve for a fifth day today, discussing ways to save AIG, said a spokesman for the New York Fed. AIG, with $1 trillion in assets, piled up net losses totaling $18.5 billion in the past three quarters on writedowns tied to the collapse of the U.S. subprime mortgage market.

Mish described this situation as "Fed Sponsored Poker Party Morphs Into "Old Maid"". That's exactly what is happening. All the parties are deciding who will be stuck with the check for this thing.

Manufacturing Taking A Hit

Amidst all of yesterday's turmoil two key pieces of economic data were lost. The Empire State index and Industrial Production.

Why is this information important? It's one of the four economic areas the NBER looks at when they are dating a recession:

Let's start with the Empire State Index, which is from the NY Fed:

Here's a chart from econoday:

This number (the gray line on the chart) has been weak for the last year. That's 8 months of sketchy reads which is not good. The only good news in this release is the current and future prices component which dropped. In conjunction with yesterday's CPI release, we're getting more and more indications inflation is becoming less of an issue.

As for industrial production:

Here are the relevant charts from econoday:

Note the year over year decline has been going on for the last 8 months and has been negative since the beginning of the year.

Also note that capacity utilization is still dropping, indicating the country is using less and less of its manufacturing capacity:

The bottom line is this is terrible news. Exports -- which have been an important growth component for the last year or so -- haven't been strong enough to keep these readings anywhere except stagnant. And domestic demand is obviously not strong enough to keep things humming. The capacity utilization drop indicates manufacturing is slowing shutting down what it can to remain profitable.

Why is this information important? It's one of the four economic areas the NBER looks at when they are dating a recession:

The committee places particular emphasis on two monthly measures of activity across the entire economy: (1) personal income less transfer payments, in real terms and (2) employment. In addition, we refer to two indicators with coverage primarily of manufacturing and goods: (3) industrial production and (4) the volume of sales of the manufacturing and wholesale-retail sectors adjusted for price changes. We also look at monthly estimates of real GDP such as those prepared by Macroeconomic Advisers (see http://www.macroadvisers.com). Although these indicators are the most important measures considered by the NBER in developing its business cycle chronology, there is no fixed rule about which other measures contribute information to the process.

Let's start with the Empire State Index, which is from the NY Fed:

The Empire State Manufacturing Survey indicates that manufacturing activity in New York State weakened in September. The general business conditions index slipped 10 points, to -7.4. The new orders and shipments indexes rose modestly and were slightly above zero. Current employment indexes were negative. Current and future price indexes, though still elevated, retreated noticeably—particularly for prices paid. Indexes for future business conditions and most future activity measures remained close to last month’s levels or rose moderately in September.

Here's a chart from econoday:

This number (the gray line on the chart) has been weak for the last year. That's 8 months of sketchy reads which is not good. The only good news in this release is the current and future prices component which dropped. In conjunction with yesterday's CPI release, we're getting more and more indications inflation is becoming less of an issue.

As for industrial production:

Industrial production decreased 1.1 percent in August and was revised down in June and July to show smaller gains of 0.2 percent and 0.1 percent respectively. After little movement over the previous three months, factory output was down 1.0 percent in August, in part because of a drop of 11.9 percent in the production of motor vehicles and parts. Excluding motor vehicles and parts, the index for manufacturing decreased 0.3 percent. The output of mines declined 0.4 percent, and the output of utilities fell 3.2 percent, as temperatures in August were unseasonably mild.

Here are the relevant charts from econoday:

Note the year over year decline has been going on for the last 8 months and has been negative since the beginning of the year.

Also note that capacity utilization is still dropping, indicating the country is using less and less of its manufacturing capacity:

The bottom line is this is terrible news. Exports -- which have been an important growth component for the last year or so -- haven't been strong enough to keep these readings anywhere except stagnant. And domestic demand is obviously not strong enough to keep things humming. The capacity utilization drop indicates manufacturing is slowing shutting down what it can to remain profitable.

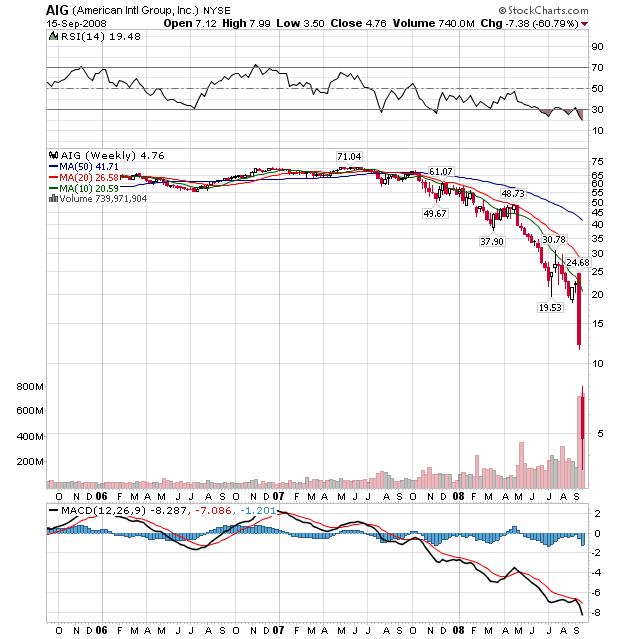

AIG -- Not Looking Good

From the WSJ:

Let's take a closer look at AIG:

The chart says traders think AIG is heading failure. Note the incredibly sharp drop that occurred in the latest week.

According to Reuter's income statement, AIG has lost money in the last two quarters.

According to Reuter's balance sheet, AIG has a positive net worth. However -- and as with all financial companies -- there is the issue of valuation of a long-term portfolio. For the last three quarters AIG has reported "long-term investments" of approximately $702 billion. The question is are these appropriate values for the investments involved? Considering all that we have seen over the last year, I would have to say these are not valued appropriately. I have no proof of that. However, I think the record of the entire financial sector is clear.

I should also add that I think the ratings agencies have absolutely no credibility right now. They gave great ratings to a lot of the paper that is currently blowing up all over the world. Simply put, the ratings system is completely broken.

Who is their right mind would want to loan money to this company? They are losing money. Their ratings are being cut. The street thinks they will fail as evidenced in the stock price charts. Also note that Goldman and JPM are seeking to raise -- there is no mention of these companies contributing.

The bottom line, there is no way this happens without government back-stopping the deal.

American International Group Inc. was facing a severe cash crunch as ratings agencies cut the firm's credit ratings, forcing the giant insurer to raise $14.5 billion to cover its obligations.

With AIG now tottering, a crisis that began with falling home prices and went on to engulf Wall Street has reached one of the world's largest insurance companies, threatening to intensify the financial storm and greatly complicate the government's efforts to contain it. The company is such a big player in insuring risk for institutions around the world that its failure could shake the global financial system.

Shares of AIG fell 42% to $2.70 in recent premarket activity Tuesday after earlier in the premarket session rising 5% to $5. The stock tumbled 61% on Monday amid the U.S. stock market's worst daily point plunge since the first day of trading after the Sept. 11, 2001, terrorist attacks. In addition to AIG's woes, the financial markets were rattled by the rushed sale Sunday of Merrill Lynch & Co. to Bank of America Corp. and the bankruptcy-court filing of Lehman Brothers Holdings Inc.

Let's take a closer look at AIG:

The chart says traders think AIG is heading failure. Note the incredibly sharp drop that occurred in the latest week.

According to Reuter's income statement, AIG has lost money in the last two quarters.

According to Reuter's balance sheet, AIG has a positive net worth. However -- and as with all financial companies -- there is the issue of valuation of a long-term portfolio. For the last three quarters AIG has reported "long-term investments" of approximately $702 billion. The question is are these appropriate values for the investments involved? Considering all that we have seen over the last year, I would have to say these are not valued appropriately. I have no proof of that. However, I think the record of the entire financial sector is clear.

I should also add that I think the ratings agencies have absolutely no credibility right now. They gave great ratings to a lot of the paper that is currently blowing up all over the world. Simply put, the ratings system is completely broken.

The Federal Reserve hosted a meeting to discuss AIG's prospects at the central bank's offices in New York on Monday with company executives, bankers as well as state and federal officials

With strong encouragement from the Fed, Goldman Sachs Group Inc. and J.P. Morgan Chase & Co. are seeking to raise $70 billion to $75 billion in loans to help prop up AIG, according to people familiar with the situation. Word of AIG's efforts to borrow that much sent the stock market tumbling in the last hour of trading.

Who is their right mind would want to loan money to this company? They are losing money. Their ratings are being cut. The street thinks they will fail as evidenced in the stock price charts. Also note that Goldman and JPM are seeking to raise -- there is no mention of these companies contributing.

The bottom line, there is no way this happens without government back-stopping the deal.

Wednesday Commodities Roundup

I'm going to combine the commodities round-up with today's CPI release because the two are very inter-related.

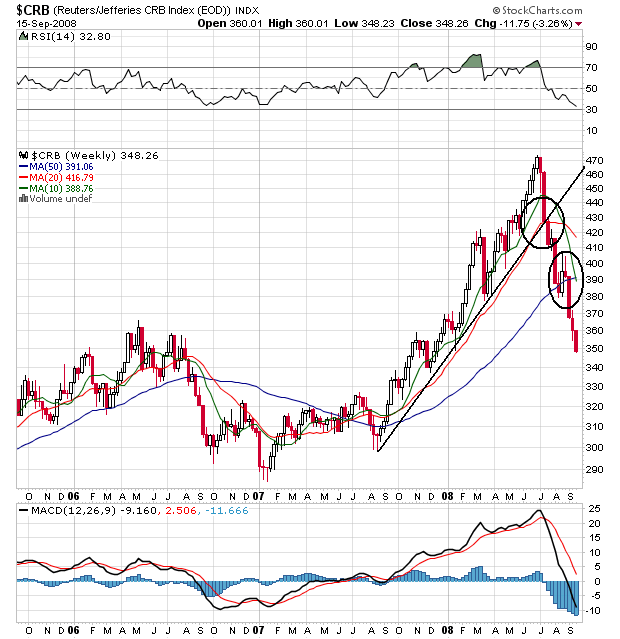

On the weekly chart of the CRB index, note the following:

-- Prices broke the year-long uptrend at the beginning of July

-- Price broke through the 50 week SMA three weeks ago with a very large downward moving candle.

-- The 10 week SMA has moved through the 20 and 50 week SMA

-- The 20 week SMA is now moving lower in a convincing fashion

-- Prices are below all the SMAs

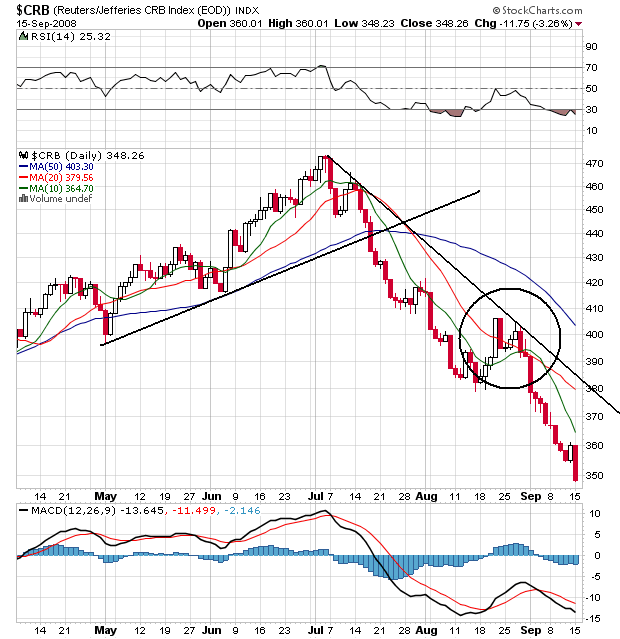

On the daily chart, note the following:

-- Prices are below all the SMAs

-- All the SMAs are heading lower

-- The shorter SMAs are below the longer SMAs

-- Prices have been in a downward trend for two and a half months

-- Prices are now using the SMAs as resistance rather than support

Short version: this chart is now very bearish in both the weekly and daily time frames. Also note because this has been happening for some time, we are starting to see some effects in the CPI:

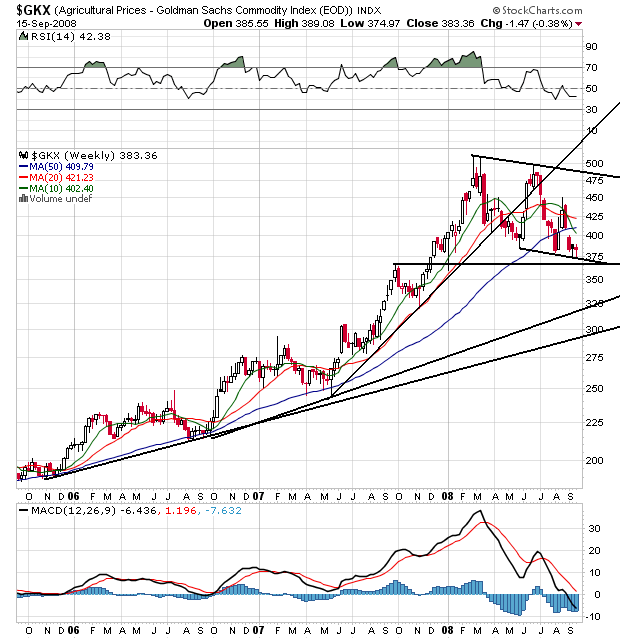

Note that decreases in all the energy numbers are a primary reason for last month's drop. Considering oil is still dropping that trend is likely to continue. Also note that food and gas are a primary reasons for this year's increase. While energy is down (I will cover oil tomorrow morning but the short version it's now in a bear market) food is topping:

Notice the following on the weekly agricultural price chart:

-- There are two primary long-term trends still in place. These started at the end of 2005 and about two-thirds of the way through 2006. It will be some time before these trends are gone.

-- The trend started in mid-2007 is clearly broken.

-- Prices are now moving sideways with a slight downward bias

-- Although the SMAs are bunched up there are two important developments

1.) The 10 week SMA is now below the 50 week and SMA, and

2.) Prices are below the 50 week SMA

All of this adds up to a situation where inflation may be topping or in fact dropping.

On the weekly chart of the CRB index, note the following:

-- Prices broke the year-long uptrend at the beginning of July

-- Price broke through the 50 week SMA three weeks ago with a very large downward moving candle.

-- The 10 week SMA has moved through the 20 and 50 week SMA

-- The 20 week SMA is now moving lower in a convincing fashion

-- Prices are below all the SMAs

On the daily chart, note the following:

-- Prices are below all the SMAs

-- All the SMAs are heading lower

-- The shorter SMAs are below the longer SMAs

-- Prices have been in a downward trend for two and a half months

-- Prices are now using the SMAs as resistance rather than support

Short version: this chart is now very bearish in both the weekly and daily time frames. Also note because this has been happening for some time, we are starting to see some effects in the CPI:

The Consumer Price Index for All Urban Consumers (CPI-U) decreased 0.4 percent in August, before seasonal adjustment, the Bureau of Labor Statistics of the U.S. Department of Labor reported today. The August level of 219.086 (1982-84=100) was 5.4 percent higher than in August 2007.

.....

On a seasonally adjusted basis, the CPI-U decreased 0.1 percent in August, following a 0.8 percent increase in July. The index for energy fell 3.1 percent in August after three consecutive sharp increases. The gasoline index declined by 4.2 percent in August but is 35.6 percent higher than in August 2007. The index for household energy, which was up 3.8 percent in July, declined 1.6 percent in August. The food index advanced 0.6 percent in August after rising 0.9 percent in July. The index for food at home rose 0.8 percent in August after a 1.2 percent increase in July and is up 7.5 percent over the past year.

.....

During the first eight months of 2008, the CPI-U rose at a 5.1 percent seasonally adjusted annualized rate (SAAR). This compares with a 4.1 percent increase for the 12 months ending December 2007. The energy index rose at a 22.4 percent SAAR in the first eight months of 2008 after increasing 17.4 percent in 2007. Gasoline prices increased at a 22.1 percent SAAR in 2008 after a 29.6 percent increase in 2007, while natural gas prices rose at a 46.3 percent SAAR after decreasing 0.4 percent in 2007. The food index increased at a 7.5 SAAR for the first eight months of 2008 after increasing 4.9 percent in 2007. Excluding food and energy, the CPI-U has advanced at a 2.5 percent SAAR in 2008 following a 2.4 percent increase in 2007.

Note that decreases in all the energy numbers are a primary reason for last month's drop. Considering oil is still dropping that trend is likely to continue. Also note that food and gas are a primary reasons for this year's increase. While energy is down (I will cover oil tomorrow morning but the short version it's now in a bear market) food is topping:

Notice the following on the weekly agricultural price chart:

-- There are two primary long-term trends still in place. These started at the end of 2005 and about two-thirds of the way through 2006. It will be some time before these trends are gone.

-- The trend started in mid-2007 is clearly broken.

-- Prices are now moving sideways with a slight downward bias

-- Although the SMAs are bunched up there are two important developments

1.) The 10 week SMA is now below the 50 week and SMA, and

2.) Prices are below the 50 week SMA

All of this adds up to a situation where inflation may be topping or in fact dropping.

Monday, September 15, 2008

Keep Your Eyes Open

Keep the following companies in your thoughts (and prayers).

AIG:

Wachovia:

Washington Mutual:

Oh yeah -- keep your eyes on every other financial company out there.

AIG:

Insurer American International Group Inc struggled for survival a day after a financial tsunami swept away investment bank Lehman Brothers and forced the sale of rival Merrill Lynch in the biggest financial industry shake-up since the Great Depression.

AIG (NYSE:AIG - News) scrambled for a financial lifeline on Monday after investment bank Lehman Brothers Holdings Inc (NYSE:LEH - News) failed to find a rescuer, and Merrill Lynch & Co Inc (NYSE:MER - News) agreed to be taken over by Bank of America Corp (NYSE:BAC - News).

Wachovia:

Shares of Wachovia Corp. dropped dramatically Monday as the investment community’s concerns over the exposure of big banks to bad mortgage loans intensified.

Wachovia, the fourth-largest bank in the country, saw its stock price fall by $3.12, or 21.9 percent, to $11.15 in afternoon trading. Wachovia’s stock price has already dropped by more than 70 percent from a year ago.

Washington Mutual:

Standard & Poor's on Monday cut its ratings on Washington Mutual Inc (NYSE:WM - News) into junk territory, citing exposures the bank has to bad mortgage debt and volatile markets.

"The company's weak equity pricing in the markets is also a concern, and it increasingly appears that market conditions could overtake credit fundamentals and leave the company with greatly diminished financial flexibility," S&P said in a statement.

Oh yeah -- keep your eyes on every other financial company out there.

Today's Markets

While I'm sure they're still looking at all those little slips of paper on the floor of the exchange, the bottom line is the day is over and the damage is pretty severe:

The markets formed a triangle pattern from the open until about 12:30. Then prices crashed through lower support from both the triangle and the low point during the day. Note the increasingly higher volume at the end of the day along with the gap down 10 minutes before close.

See the post below for a complete reason this is a very scary chart.

It's Monday, which means there are four more trading days. AIG is on the ropes and there is plenty of reason to be deeply concerned about the future of the financial sector. And the market -- in one day -- traded to just a hare above an important technical level. If prices move through 120 we've got a lot of downward ground to cover.

The markets formed a triangle pattern from the open until about 12:30. Then prices crashed through lower support from both the triangle and the low point during the day. Note the increasingly higher volume at the end of the day along with the gap down 10 minutes before close.

See the post below for a complete reason this is a very scary chart.

It's Monday, which means there are four more trading days. AIG is on the ropes and there is plenty of reason to be deeply concerned about the future of the financial sector. And the market -- in one day -- traded to just a hare above an important technical level. If prices move through 120 we've got a lot of downward ground to cover.

A Look At the Markets

Below are three different perspectives on the SPYs

Above is a long-term (10-year) chart in weekly increments. Notice the following:

-- The market clearly formed a double top. The first one corresponds to the top of the last economy and the second one occurred right before the credit crisis started. Currently the market has touched the 50% retracement level for the rally that started at the beginning of 2003. From a technical perspective this would be a level where things should happen.

But let's assume we're about to make another downward move because the economy is about to start a second wave of downward movement (consider that employment is dropping, the rest of the world is slowing down which will slow the US export market, year over year retail sales are now negative, personal income has been dropping and manufacturing is hovering around 0). That means the double top could be a portend of a far worse market.'

On the yearly chart, notice we are clearly in a down, up down movement. Also note we've had a total series of lower lows and lowers highs.

On the daily look, notice the following:

-- All the SMAs are moving lower

-- Prices are below all the SMAs

-- The 10 day SMA has moved through the 50 day SMA

-- The 20 day SMA is about to move through the 50 day SMA

-- There is key technical support at 120

Above is a long-term (10-year) chart in weekly increments. Notice the following:

-- The market clearly formed a double top. The first one corresponds to the top of the last economy and the second one occurred right before the credit crisis started. Currently the market has touched the 50% retracement level for the rally that started at the beginning of 2003. From a technical perspective this would be a level where things should happen.

But let's assume we're about to make another downward move because the economy is about to start a second wave of downward movement (consider that employment is dropping, the rest of the world is slowing down which will slow the US export market, year over year retail sales are now negative, personal income has been dropping and manufacturing is hovering around 0). That means the double top could be a portend of a far worse market.'

On the yearly chart, notice we are clearly in a down, up down movement. Also note we've had a total series of lower lows and lowers highs.

On the daily look, notice the following:

-- All the SMAs are moving lower

-- Prices are below all the SMAs

-- The 10 day SMA has moved through the 50 day SMA

-- The 20 day SMA is about to move through the 50 day SMA

-- There is key technical support at 120

Lehman's Story

From Marketwatch:

Let's go to the balance sheet as presented on Reuters. On their February 29 balance sheet, Lehman had $695 million of "long-term investments." By May that was $563 million. Some of the assets were probably sold. But, that's still a big drop. However, now Lehman is declaring Chapter 11 bankruptcy, which is:

They say they are doing this to "protect their assets" during the reorganization. But something doesn't add up here. They still have a positive book value -- unless there is a certain amount of gross value overstatements on their balance sheet. This means the value of their portfolio of mortgage related products (or any securitized product) is nowhere near what they say it's worth. That would make the most sense as to why they are declaring bankruptcy. In other words, their publicly stated books are pure fiction.

Lehman on Monday filed for Chapter 11 bankruptcy protection, ending the 158-year-old Wall Street firm's run and rattling the foundation of the global financial system.

Lehman said that it will continue business while it explores the sale of its broker and investment-management units and other strategic alternatives.

.....

The filing shows that Lehman is closing its doors with more than $600 billion of debt. The bank has total debts of $613 billion against total assets of $639 billion. Its filing with the Bankruptcy Court of the Southern District of New York shows that Lehman had more than 100,000 creditors.

The announcement came after a frantic weekend of negotiations in which potential acquirers backed away from a deal and federal officials balked at committing taxpayer funds to help save the Wall Street giant.

In a statement on its Web site, Lehman said the filing would affect only the parent, Lehman Brothers Holdings, and that its subsidiaries, including Neuberger Holdings LLC, would continue to operate and customers could make trades.

Let's go to the balance sheet as presented on Reuters. On their February 29 balance sheet, Lehman had $695 million of "long-term investments." By May that was $563 million. Some of the assets were probably sold. But, that's still a big drop. However, now Lehman is declaring Chapter 11 bankruptcy, which is:

Chapter 11 is a chapter of the United States Bankruptcy Code, which permits reorganization under the bankruptcy laws of the United States. Chapter 11 bankruptcy is available to any business, whether organized as a corporation or sole proprietorship, or individuals with unsecured debt of at least $336,900.00 or secured debt of at least $1,010,650.00, although it is most prominently used by corporate entities. In contrast, Chapter 7 governs the process of a liquidation bankruptcy, while Chapter 13 provides a reorganization process for the majority of private individuals with unsecured debts of less than $336,900.00 and secured debts of less than $1,010,650.00 as of April 1, 2007.

They say they are doing this to "protect their assets" during the reorganization. But something doesn't add up here. They still have a positive book value -- unless there is a certain amount of gross value overstatements on their balance sheet. This means the value of their portfolio of mortgage related products (or any securitized product) is nowhere near what they say it's worth. That would make the most sense as to why they are declaring bankruptcy. In other words, their publicly stated books are pure fiction.

From One Disaster To Another

This has been one hell of a weekend. On Friday night my wife and I were in Houston, Texas. We survived Ike intact; I'm fine, Mr$. Bonddad is fine, all three dogs are fine and the house is fine. However, I am currently in Austin, Texas for the week.

Then I wake up and find out Lehman and Merrill Lynch are no longer going concerns on Wall Street. And this is a few weeks after the "free market" US nationalizes it's mortgage industry.

Let's back up a bit and see how we got here. Advance warning: this will be long and fairly complicated, so get a cup of coffee now (actually, get the pot ready).

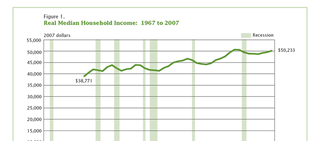

A few weeks ago, I wrote an article titled, "An extended shallow near recession." This was a riff off a comment made by one of the people who writes at Angry Bear. The point is this expansion has not felt like a real expansion. Job growth has been the weakest of any expansion since 1960. Real median household income is now at the same level it was in 2001. (Please see The Bush Boom Was A Complete Bust.) Combined these elements tell us the economy is doing very poorly. These two points also tell us there is at least one fundamental problem with the economy if not more.

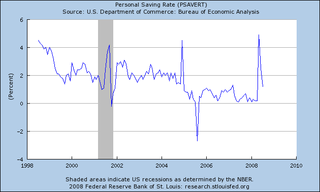

So -- let's look at am important fundamental issue with the US economy. At the beginning of this expansion the US savings rate was right around 2%. Here's a graph from the St. Louis Federal Reserve:

Here's what this figure means. An economist defines savings as all the money left over after a person spends money on everything else. In other words, after a person has paid their bills and mortgage and bought all their other stuff (clothes, restaurants etc...) the left over money is "savings". The assumption here is people buy stuff and then save whatever is left. The point with this data is at the beginning of this expansion people were already spending just about everything they made.

Let's add in two more data points. Personal consumption expenditures increased for the duration of this expansion. According to the Bureau of Economic Analysis, real personal consumption expenditures increased from a level of 104.128 to 123.931. So people kept spending. At the same time, incomes have been stagnant for the vast majority of the US population.

This same data is born out in the Census Bureau's real median household income:

So let's sum up. Real (inflation adjusted) incomes for the vast majority of Americans declined this expansion. At the same time, people were already spending most of their incomes at the beginning of this expansion yet they continued to increased their spending for the duration of this expansion. Where did all of the new money for increased spending come from?

Tons of debt. At the beginning of this expansion total household debt outstanding stood at $7.6 trillion. That current figure is $13.9 trillion. That's an increase of 82%. To place that figure in perspective, total household debt outstanding is now almost as large as total US GDP. All of that does not exist in a vacuum; it has to go somewhere. And that's where we get to the current problems in the markets.

As the figures above shows, the US went on a debt orgy primarily concentrated in mortgages. First, the Federal Reserve lowered interest rates to 0% after adjusting for inflation. Then the financial system had to increase the number of people who could access the debt market and increase the amount of money they could get access too. However early on it was obvious this would cause problems:

All of this debt was cut into a large amount of securitized debt -- collateralized mortgage obligations (CMOs), collateralized debt obligations and the like. The belief among everybody was securitization so spread out risk that possible problems (like the ones we are currently having) were non-existent.