- by New Deal democrat

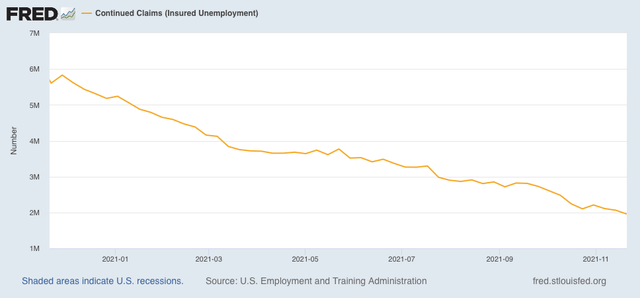

One month ago, we got very large upward revisions to previous data. This month the big questions I had were whether that would continue, and whether the bulge decrease in new jobless claims to a half century low would translate to another big top line number in the jobs report. Additionally, in view of the recent inflation numbers, I wanted to see if wage growth would hold up.

The 6 month average of monthly gains as of now is 612,000: less than one month ago, but still very goodnot bad. But we still have 3.9 million jobs to go to equal the number of employees in February 2020 just before the pandemic hit. The largest share of this is in jobs that employees and/or their potential customers consider still to be unsafe.

Here’s my synopsis of the report:

HEADLINES:

- 210,000 jobs added. Private sector jobs increased 235,000, but government shed -25,000 jobs. The alternate, and more volatile measure in the household report indicated a HUGE gain of 1,136,000 jobs, which factors into the unemployment and underemployment rates below.

- The total number of employed is still -3,912,000, or -2.6% below its pre-pandemic peak. At this rate jobs have grown in the past 6 months (which have averaged 612,000 per month), it will take another 6 or 7 months for employment to completely recover.

- U3 unemployment rate declined -0.4% to 4.2%, compared with the January 2020 low of 3.5%.

- U6 underemployment rate declined -0.5% to 7.8%, compared with the January 2020 low of 6.9%.

- Those not in the labor force at all, but who want a job now, declined 119,000 to 5.859 million, compared with 5.010 million in February 2020.

- Those on temporary layoff decreased -255,000 to 801,000.

- Permanent job losers declined -205,000 to 1,921,000.

- September was revised upward by 67,000, while October was revised upward by 15,000, for a net gain of 82,000 jobs compared with previous reports.

Leading employment indicators of a slowdown or recession

These are leading sectors for the economy overall, and will help us gauge how strong the rebound from the pandemic will be. These were positive:- the average manufacturing workweek, one of the 10 components of the Index of Leading Indicators, rose 0.1 hour to 40.4 hours.

- Manufacturing jobs increased 31,000. Since the beginning of the pandemic, manufacturing has still lost -253,000 jobs, or -2.0% of the total.

- Construction jobs increased 31,000. Since the beginning of the pandemic, -115,000 construction jobs have been lost, or -1.5% of the total.

- Residential construction jobs, which are even more leading, rose by 4,100. Since the beginning of the pandemic, 49,100 jobs have been *gained* in this sector, or +5.8%.

- temporary jobs rose by 6,200. Since the beginning of the pandemic, there have still been 153,000 jobs lost, or -5.2% of all temporary jobs.

- the number of people unemployed for 5 weeks or less decreased by -113,000 to 1,972,000, which is now *lower* than just before the pandemic hit.

- Professional and business employment increased by 90,000, which is still -69,000, or about -0.3%, below its pre-pandemic peak.

Wages of non-managerial workers

- Average Hourly Earnings for Production and Nonsupervisory Personnel: rose $0.12 to $26.40, which is a 5.9% YoY gain. This continues to be excellent news, considering that a huge number of low-wage workers have finally been recalled to work.

Aggregate hours and wages:

- the index of aggregate hours worked for non-managerial workers rose by 0.2%, which is a loss of -2.3% since just before the pandemic.

- the index of aggregate payrolls for non-managerial workers rose by 0.6%, which is a gain of 7.3% (before inflation) since just before the pandemic.

Other significant data:

- Leisure and hospitality jobs, which were the most hard-hit during the pandemic, gained 23,000 jobs, but are still -1,334,000, or -7.9% below their pre-pandemic peak.

- Within the leisure and hospitality sector, food and drink establishments gained 11,000 jobs, and is still -756,600, or -6.1% below their pre-pandemic peak.

- Full time jobs increased 954,000 in the household report.

- Part time jobs increased 42,000 in the household report.

- The number of job holders who were part time for economic reasons declined by -137,000 to 4,286,000, which is a *decrease* of -112,000 since before the pandemic began.

SUMMARY

Once again this month was a tale of two very different reports: a lackluster establishment report and a blockbuster household report! I will go out on a limb and state with great confidence that over the next two months the relatively poor establishment number is going to be revised considerably higher, just as the original lackluster reports of August and September were - and like almost every other report this year has been to some extent.

The biggest part of the disappointment in the establishment report was that food and drink, and more broadly leisure and hospitality, added almost no jobs, in contrast with the huge gains earlier this year. Temporary job gains were also lackluster. By contrast, gains in professional and business jobs and construction jobs were par for the last 12 months, while gains in manufacturing were a little light.

But the declines in the unemployment and underemployment rates were stellar, with the former only 0.7% above its pre-pandemic low and the latter only 1.0% above its pre-pandemic low as well. The even broader metric of those who are not in the labor force but want a job now is only about 1 million above its pre-pandemic low as well.

Wages continue to increase sharply. Aggregate payrolls are excellent compared with pre-pandemic levels.

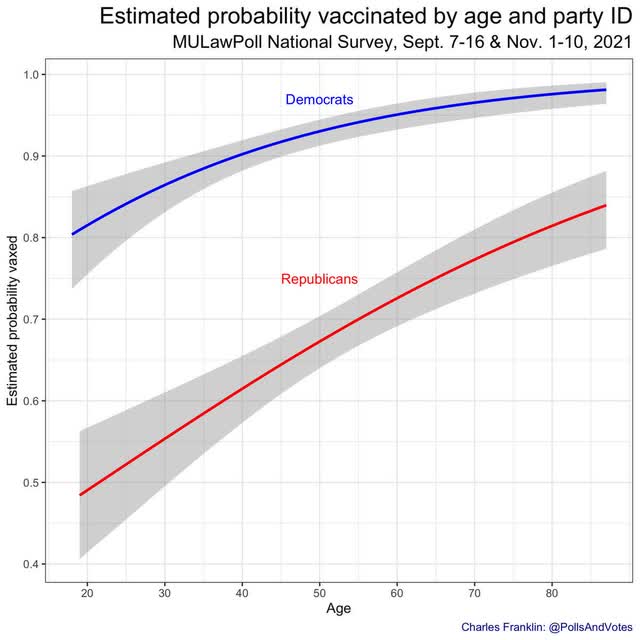

As I wrote yesterday in connection with jobless claims, at this point the *only* thing keeping employment from exceeding its pre-pandemic highs is the pandemic itself. With nearly 30% of American adults absolutely refusing to get vaccinated, congested indoor activities - especially unmasked ones like dining - continue to be viewed as unsafe by most other Americans. The final pieces of the employment picture will not resolve until the pandemic is resolved, and that won’t happen with a population of nearly 100,000,000 COVIDiots.