It's the weekend. Because of the pretty extreme market action last week I'll probably be back late tomorrow to prep for the week.

Until then -- do anything except think about economics or the markets.

Capital One Financial Corp (NYSE:COF - News), a credit card issuer and banking company, posted a third quarter net loss after taking more than $800 million of charges from shuttering its GreenPoint Mortgage business.Delinquencies on U.S. credit card loans jumped, and the company's shares declined in thin after-hours trading.

The company is writing off more loans, particularly in its U.S. credit card business, but that is mainly because write-offs had previously been unusually low, CEO Richard Fairbank said on a conference call. Losses are normalizing rather than indicating serious underlying credit trouble, he added.

The company wrote off a total of $1.03 billion of loans on and off its balance sheet, for a managed loan charge-off rate of 2.86 percent, down from 2.92 percent the same quarter last year.Fairbank said Capital One would likely write down $1.2 billion of loans in the fourth quarter.

Total managed loan write-offs in 2008 are expected to be about $4.9 billion, he said.

The delinquency rate in its U.S. credit card loans jumped to 4.46 percent on a managed basis, from 3.53 percent in the third quarter of 2006. Higher delinquencies typically imply higher write-offs in the future.

The company said that it expects to write off U.S. credit card loans at an annualized 5.25 percent rate in the fourth quarter, compared with a 4.13 percent rate in the third quarter and a 3.39 percent rate in the third quarter of last year.

This is some of the best spin control I have seen yet from the financial companies. Write-offs are obviously increasing, but earnings are "normalizing". That is sheer corporate brilliance.

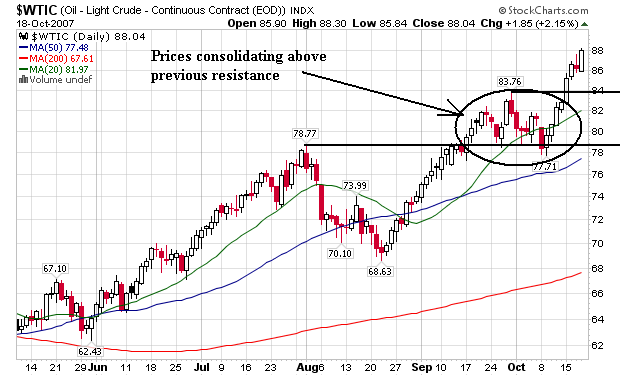

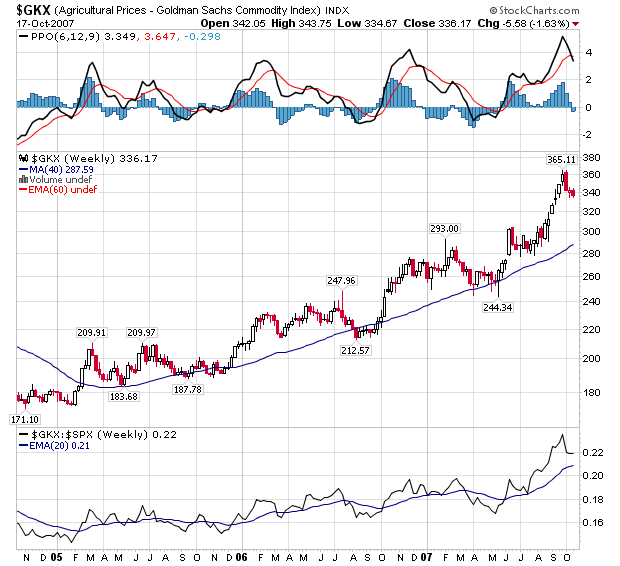

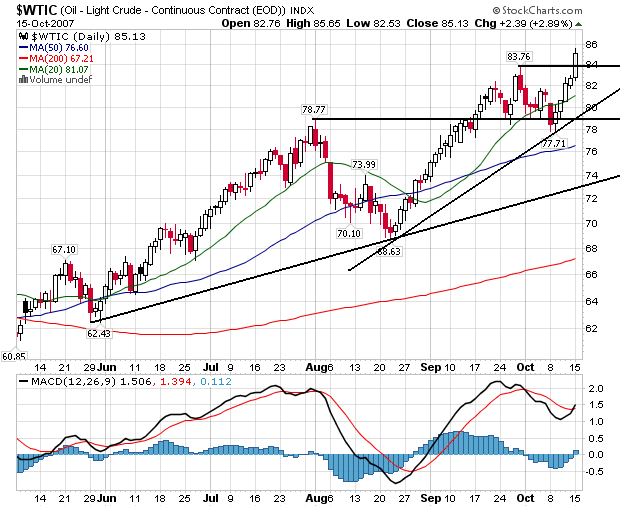

Remember this chart from This Week in Petroleum?Wal-Mart (WMT) is cutting prices on 15,000 more items this week — 20% more than last year — and plans to slash more prices in coming days to boost sales during the holiday season.The world's biggest retailer cut prices earlier this month on some of the hottest holiday toys, hard-to-resist deals that could help counter concerns about toy safety.

"Discounting is starting early and often this year," says retail strategist John Champion of global consulting firm Kurt Salmon Associates. "Wal-Mart is anxious about the Christmas season and trying to get an early jump with the consumers. Other retailers are going to follow suit."

The latest cuts come as consumers face continued economic pressure from a shaky real estate market and high energy costs, making it an especially good move for Wal-Mart, says Phil Rist, executive vice president at consumer insights firm BIGresearch.

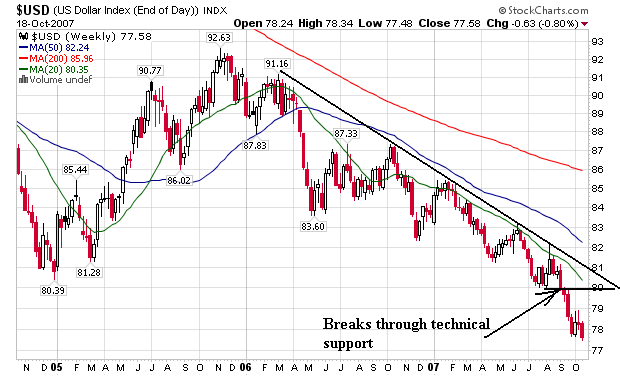

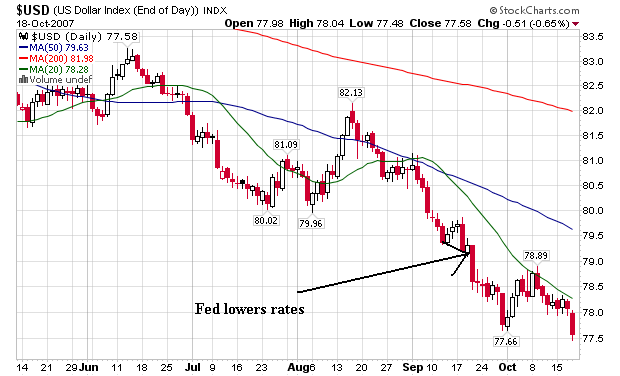

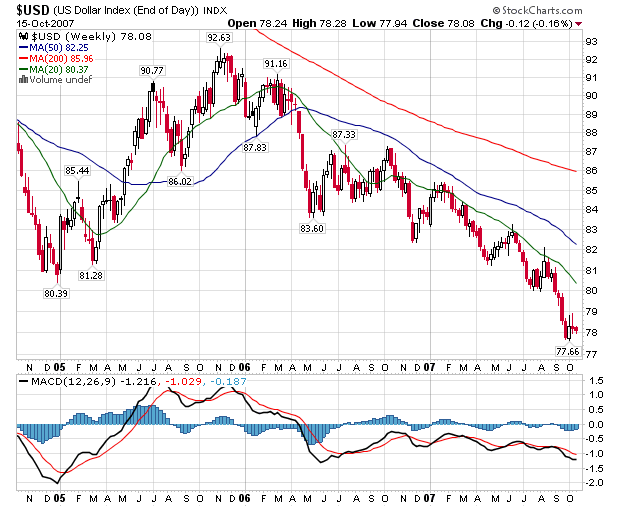

Oil prices held near an all-time high of $90 a barrel Friday, crossed for the first time in after-hours trading Thursday in New York, as a weakening U.S. dollar lifted prices.

Light, sweet crude for November delivery rose to $90.02 a barrel in Thursday evening electronic trading on the New York Mercantile Exchange. By midday Friday in Europe, the contract was trading at $89.92 a barrel.

Analysts said investors were buying more oil to hedge further losses in the currency. The dollar fell to a new low against the euro Friday and sagged against the yen.

Wachovia Corp.'s third-quarter net income dropped 10% as loan-loss provisions quadrupled and the company recorded $1.3 billion in losses and write-downs. Wachovia also signaled increasing credit troubles ahead.

.....

Loan-loss provisions surged to $408 million from $108 million amid growth in auto, commercial and consumer real estate lending. Net charge-offs were 0.19% of average net loans, compared with 0.16% a year earlier. Nonperforming assets, troubled loans that could turn into charge-offs, more than doubled to 0.63% of loans from 0.26%.

The U.S. average retail price for regular gasoline was lower by 0.8 cent last week to 276.2 cents per gallon as of October 15, 2007, but is still 53.6 cents higher than last year. All regions were lower except the West Coast which grew by 4.5 cents to 297.9 cents per gallon, the highest price in the country. The average price for regular grade in California was 305.3 cents per gallon, up 5.7 cents from last week and 51.3 cents per gallon over the previous year. The East Coast price fell 1.5 cents to 273.1 cents per gallon while the Gulf Coast declined by 2.5 cents to 264.2 cents per gallon, the lowest regional price. The Midwest price dropped 2.0 cents to 273.5 cents per gallon this week, plunging 24.4 cents since September 10. The Rocky Mountain region price decreased 0.7 cent to 279.5 cents per gallon.

Hershey Co., the largest U.S. candy maker, said third-quarter profit plunged 66 percent and sales unexpectedly fell as it lost market share and dairy costs rose.

.....

Nonfat dry milk prices rose 20 percent from the first quarter and are more than double what they were a year ago, according to Katzman. He is one of 15 analysts who have a ``hold'' rating on the stock. Three others recommend buying Hershey, and two say ``sell.''

PMI Group Inc., the second-largest U.S. mortgage insurer, estimated a third-quarter loss of $1.05 a share, as borrowers' ability to repay their home loans ``significantly worsened'' in September. The company fell as much as 7.3 percent in New York trading.

The cost to bail out lenders is expected to increase fivefold from the same period a year earlier to about $350 million, the Walnut Creek, California-based insurer said in a statement today. PMI also withdrew its earnings forecasts for the year.

Rival MGIC Investment Corp., the largest mortgage insurer, yesterday posted its first quarterly loss since it went public in 1991. The Milwaukee-based company said it won't be profitable in 2008 as foreclosures increase from a record and the housing market worsens in parts of California and Florida.

Bank of America Corp. posted a 32% drop in third-quarter net income amid a dismal performance by its investment bank and higher reserves to cover potential bad loans.

The combination of more than $1.4 billion in trading losses in its investment bank and about $2 billion in provisions for credit losses pushed the Charlotte-based bank's third-quarter profits down to $3.7 billion, or 82 cents a share, from $5.42 billion, or $1.18 a share, a year earlier. Revenue fell 12% to $16.3 billion. It was the first time since late 2005 that Bank of America has failed to boost its year-over-year profits.

While other banks have been struggling with the fallout from this summer's credit crunch, and analysts were bracing for a bad quarter, Bank of America's results fell far short of Wall Street's expectations of earnings of $1.06 a share on revenue of $18.3 billion.

Prices paid by U.S. consumers rose more than forecast in September as food and energy costs climbed, while core measures showed inflation remains contained.

The 0.3 percent increase followed a 0.1 percent decline in August prompted by falling oil prices, the Labor Department said today in Washington. So-called core producer prices, which exclude fuel and food costs, rose 0.2 percent for a second month in line with forecasts.

With inflation under control, Federal Reserve policy makers have leeway to consider cutting their benchmark rate again later this month to keep the economy growing in the face of a deepening housing recession. Fed Chairman Ben S. Bernanke this week reiterated the central bank would ``act as needed'' to foster sustainable growth along with price stability.

``A slower economy and additional slack in the labor market should help keep inflation under control,'' Ethan Harris, chief economist at Lehman Brothers Holdings Inc. in New York, said before the report. ``Tame inflation and weaker growth imply additional rate cuts.''

Economists had forecast consumer prices would rise 0.2 percent after a 0.1 percent decline the prior month, according to the median of 82 projections in a Bloomberg News survey. Estimates of the increase ranged from no change to a 0.5 percent gain.

Consumer prices increased at a seasonally adjusted annual rate (SAAR) of 1.0 percent in the third quarter of 2007, following increases in the first and second quarters at annual rates of 4.7 and 5.2 percent, respectively. This brings the year-to-date annual rate to 3.6 percent and compares with an increase of 2.5 percent for all of 2006. The index for energy, which advanced at annual rates of 22.9 and 32.9 percent in the first two quarters, declined at a 14.8 percent rate in the third quarter of 2007. Thus far this year, energy costs have risen at an 11.7 percent SAAR after increasing 2.9 percent in all of 2006. In the first nine months of 2007, petroleum-based energy costs (energy commodities) advanced at a 20.6 percent rate and charges for energy services (gas and electricity) increased at a 1.3 percent rate. The food index rose at a 5.7 percent SAAR in the first nine months of 2007 after advancing 2.1 percent in all of 2006. Grocery store food prices increased at a 6.7 percent annual rate in the first nine months of 2007, reflecting acceleration over the last year in each of the six major groups. These increases ranged from annual rates of 4.0 percent in the index for other food at home to 17.7 percent in the index for dairy products.

The CPI-U excluding food and energy advanced at a 2.5 percent SAAR in the third quarter, following increases at rates of 2.3 percent in each of the first two quarters of 2007. The advance at a 2.3 percent SAAR for the first nine months of 2007 compares with a 2.6 percent rise in all of 2006. The deceleration largely reflects a smaller increase in the index for shelter and a downturn in the index for apparel. Shelter costs, which rose 4.2 percent in all of 2006, have risen at a 3.2 percent annual rate in the first nine months of 2007. The index for apparel, which last year registered its first annual increase since 1997, has declined at an annual rate of 1.7 percent thus far in 2007. The annual rates for selected groups for the last seven and three-quarter years are shown below.

This brings the year-to-date annual rate [of total consumer prices] to 3.6 percent and compares with an increase of 2.5 percent for all of 2006.

Thus far this year, energy costs have risen at an 11.7 percent SAAR after increasing 2.9 percent in all of 2006.

Grocery store food prices increased at a 6.7 percent annual rate in the first nine months of 2007, reflecting acceleration over the last year in each of the six major groups.

Wells Fargo's (WFC) Q3 profit rose 6% as revenue climbed 10%, but both missed analyst estimates. Ongoing home and loan woes would hurt its Q4 results. KeyCorp (KEY) also missed Q3 views and warned on Q4. US Bancorp (USB) topped EPS views by a penny as it lifted loan-loss reserves by 47%. Its shares edged down; KeyCorp fell 5% and Wells Fargo 4%.

The confidence of U.S. home builders has been shaken to its lowest point since records began 22 years ago, a housing trade group said Tuesday.

The National Association of Home Builders' index for sales of new, single-family homes decreased to 18 this month from 20 in September. Builders are worried about mortgage market problems and bloated inventory. The reading was the lowest since the series began in January 1985, the NAHB said.

"Builders in the field are reporting that, while their special sales incentives are attracting interest among consumers, many potential buyers are either holding out for even better deals or hesitating due to concerns about negative and confusing media reports on home values," said NAHB President Brian Catalde, a home builder from El Segundo, Calif.

D.R. Horton Inc (NYSE:DHI - News), the largest U.S. home builder, said on Tuesday quarterly net orders for new homes plunged 39 percent and cancellations spiked as the U.S. housing market continued to deteriorate.

......

D.R. Horton said net orders for its fiscal fourth quarter that ended September 30 fell to 6,374 from 10,430 a year earlier. The value of the orders dropped 48 percent to $1.3 billion from $2.5 billion.

"The 48 percent year over year decline in orders is very weak, especially considering it is off of an easy comparison with last year's fourth quarter orders down 33 percent," Wachovia analyst Carl Reichardt wrote in a research note.

Prospective buyers canceled outstanding orders at a rate of 48 percent during the quarter, up from 40 percent a year ago.

Mortgage originations will fall next year to the lowest levels since 2000, forcing job losses for at least 30,000 more home finance professionals, according to a forecast released on Wednesday by the Mortgage Bankers Association.

Inventories of homes for sale will remain high as tighter lending standards across the industry reduce available credit for prospective home-buyers, said Doug Duncan, the MBA's chief economist. Foreclosures as a result of increasing payments on adjustable-rate loans or poor underwriting will exacerbate the problem, he said.

"We have not yet seen fully the impact of the credit shock to the U.S. and world economies, and the severity of that impact will depend on how long it takes for the markets to return to normal functioning," Duncan said at the annual meeting of the Mortgage Bankers Association.

Total mortgage originations will likely decline 18 percent to $1.89 trillion, the lowest volume of purchase and refinance loans since $1.14 trillion in 2000, according to the forecast. Loan volume will slide another 6 percent in 2009, it said.

The ongoing housing correction is not ending as quickly as it might have appeared late last year.

And it now looks like it will continue to adversely impact our economy, our capital markets, and many homeowners for some time yet. Even so, I believe we have a healthy, diversified economy that will continue to grow.

Of the approximately 50 million outstanding mortgages in the U.S. today, approximately 10 million are subprime loans. Many have cited the statistic that 2 million of those subprime mortgages will reset to higher rates in the next 18 months. That statistic is true, relevant, and troubling, but it is not the complete picture of the risk going forward. Many of those borrowers will be able to afford their new mortgage payment or they will be able to refinance into another more affordable mortgage. Yet, the problem today is not limited to subprime mortgages as the number of homeowners having trouble making payments on prime mortgages is also increasing. And finally, the wide geographic variation in home price trends adds to the complexity of sizing this problem with any certainty.

Slumping demand and higher fuel costs continued to weigh on truckload carriers throughout the third quarter, and analysts suggest that earnings may fall below expectations as a result.

Truckload carriers typically dedicate an entire trailer to one customer and move the freight directly from the shipper to the receiver.

Morgan Keegan & Co. analyst Art W. Hatfield said the market is continuing to slow at a time when demand usually ramps up toward a pre-holiday peak.

"Generally speaking, the demand environment has been marked by inconsistency week to week and has yet to show signs of any building momentum," he said.

In fact, Hatfield said current conditions may be as severe as those seen in 2001, when the market was hit by the effects of an economic recession.

Another factor that hurt the sector in the third quarter is the price of fuel, with a gallon of diesel climbing 7.7 percent over the quarter to as high as $3.05, from $2.83 per gallon last year.

Forward Air Corp., a contractor to the air cargo industry, on Wednesday issued third-quarter profit guidance below Wall Street estimates, citing a slumping economy.

The news sent Forward Air shares down $2.32, or 7.9 percent, to $27 in aftermarket trading. Earlier, they fell 27 cents to $29.32 in the regular session.

Forward Air said it expects to post a profit of 35 cents to 37 cents per share for the quarter, while analysts polled by Thomson Financial expect a profit of 42 cents per share.

Trucking and logistics company Werner Enterprises Inc. on Monday said its third-quarter profit fell 11 percent, but still beat Wall Street estimates.

Net income for the three months ended Sept. 30 fell to $21.9 million, or 30 cents per share, from $24.6 million, or 31 cents per share, during the same period a year earlier.

J.B. Hunt Transport Services Inc., which provides truckload and intermodal shipping services, said Thursday its third quarter profit fell 12 percent because of higher interest expenses and lower revenue in its trucking division.

For the quarter ended Sept. 30, net income fell to $50.8 million, or 38 cents per share, from $57.8 million, or 39 cents per share, in the prior year quarter. The company had about 133.7 million shares outstanding at the end of the quarter compared with 148.7 million at the end of the same quarter last year.

U.S. housing prices will continue to decline at least through the end of next year and may not begin creeping upward again until 2010, executives from the biggest mortgage financiers said Monday.

Officials with government-sponsored mortgage companies Fannie Mae and Freddie Mac and CEOs from two major mortgage banks told the Mortgage Bankers Association's annual convention that the continuing spike in foreclosures and a glut of unsold homes will prevent any quick price rebound.

"It's going to be a long time before we see it bottom out and recover," said David Lowman, chief executive of JPMorgan Chase. "There's too much inventory already in the marketplace."

A weakening U.S. dollar, low U.S. crude inventories and increased buying by investment funds also supported prices, counterbalancing expectations of higher inventories in the weekly U.S. supply report.

Iraq's Vice President Tareq al-Hashemi arrived in Ankara Tuesday in an apparent attempt to convince Turkey not to stage a cross-border offensive to fight separatist Kurdish rebels based in Iraq. Mr. Hashemi, a Sunni Arab, was scheduled to meet with Prime Minister Recep Tayyip Erdogan and other senior officials. The Turkish Parliament was expected to approve a motion Wednesday allowing the government to order a cross-border attack over the next year.

The Turkish government's decision Monday to ask Parliament for permission to pursue Kurdish rebels into Iraq stoked the worries about potential interruptions to oil supplies. "Whenever there is any escalation in political tensions in the Middle East, oil markets become concerned," said David Moore, a commodity strategist at the Commonwealth Bank of Australia in Sydney. "There is production and there are pipelines that people worry may be affected if there are any issues in Iraq."

There have been several skirmishes along the Turkey-Iraq border already. Although oil coming out of the region has been erratic, a total disruption would send prices higher, analysts said.

Nov. oil futures shot up $2.44 to $86.13 a barrel as Turkey appeared to move close to military action vs. Kurdish guerrillas in northern Iraq. That threatens the Kirkuk-Ceyhan pipeline, which supplies half-a-million barrels a day. Meanwhile, OPEC said noncartel output would be less than expected. That comes as rich-world inventories have declined in recent weeks.

Citigroup Inc., the biggest U.S. bank, said mortgage delinquencies and consumer lending will deteriorate for the rest of the year after earnings fell 57 percent in the third quarter.

Citigroup had its biggest drop in two months in New York trading after Chief Financial Officer Gary Crittenden said on a conference call that borrower defaults are ``accelerating.''

Chief Executive Officer Charles Prince, who has overseen a 17 percent drop in the company's stock this year, said momentum ``continues very strong'' in most of the company's businesses. Since Prince became CEO in 2003, Citigroup shares are virtually unchanged, compared with a 29 percent jump at Bank of America Corp., the second-largest U.S. bank by assets.

``They certainly had a lot of troubles and to some extent have been tripping over themselves the last couple of years,'' Jeffery Harte, an analyst at Sandler O'Neill & Partners LP in Chicago, said in an interview. Prince is ``doing the right things strategically. It's become more of an execution problem lately.''

A managed investment vehicle that holds mainly highly rated asset-backed securities and funds itself using the short-term commercial paper market as well as the medium-term note (MTN) market. Because of the rolling nature of its funding, an SIV is highly dependent on maintaining the highest possible short-term and long-term credit ratings. SIVs differ from cash CDOs of asset-backed securities in that their portfolios are marked-to-market, with their ratings based on capital models agreed with the rating agencies. SIVs also have simpler capital structures than CDOs, usually comprising a junior tranche of capital notes beneath a block of senior liabilities with the same seniority. They have smaller liquidity facilities than commercial-paper conduits - which also invest in high grade ABS. SIV managers include both commercial banks such as Citigroup and Bank of Montreal, and investment managers such as Gordian Knot.

Encouraging the talks that led to the creation of the fund is the latest effort by officials to help restore liquidity to credit markets, a campaign started by the Federal Reserve in August, when it cut the interest rate on direct loans from the central bank. Fed officials have said this month that while there are signs of improvement, some markets remain under stress.

``Some markets have been experiencing illiquidity,'' San Francisco Fed President Janet Yellen said in an Oct. 9 speech in Los Angeles, referring to mortgage-backed securities and asset- backed commercial paper. ``This illiquidity has become an enormous problem for companies that specialize in originating mortgages and then bundling them to sell as securities.''

As losses in securities linked to subprime mortgages started to spread in July, investors retreated from high-risk assets. SIVs that issued commercial paper to buy the securities found they could no longer roll over the debt, forcing them to sell about $75 billion of their assets.

The popularity of SIVs has boomed since two Citigroup bankers, Nicholas J. Sossidis and Stephen Partridge-Hicks, invented the strategy in London in the late 1980s. (They later left to form their own company, London-based Gordian Knot, which operates the world's largest SIV.)

Behind Treasury's concern were banks like Citigroup, whose affiliates owned $80 billion in assets backed by mortgages and other securities. The world's biggest bank, by market value, held the assets off its balance sheet and was facing the prospect of either having to unload them in a disorderly fire-sale fashion or moving them onto its books.

Either scenario would have hurt financial markets and could have damped the economy by curtailing banks' ability to make new loans to consumers and corporations. Treasury envisioned a potentially "disorderly" unwinding of assets that could worsen the credit crunch, said a person familiar with the matter.