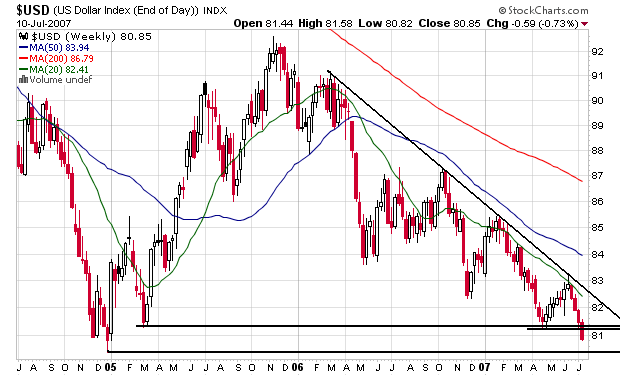

John Mauldin has provided an excellent analysis of exactly what the controversy is and more importantly provides a very readable explanation.

To start with, let's dissect the employment numbers. The official headline number for June was 132,000 new jobs. Since we need about 150,000 new jobs just to stay even with population growth, that is hardly a robust number, but not too far off from what would be a good number. Except that there are some problems with the headline number.

The employment numbers come from a survey of established businesses. But obviously the Bureau of Labor Statistics (BLS) cannot call every business in the US, so they simply survey the larger businesses. But that means they miss the growth in the small-business sector of the economy, which is where the largest amount of new jobs are created.

The BLS surveys about 160,000 businesses in its sample model. There is an unavoidable lag between an establishment opening for business and its appearing on the sample frame and being available for sampling. Because new firm "births" generate a significant portion of employment growth each month, non-sampling methods must be used to estimate this growth. To make up for this, they add or subtract a certain number of jobs, called the birth/death (of new businesses) ratio.

They use the actual births and deaths of real businesses for the last five years to make their estimates of new jobs created from new business. This is quite a legitimate methodology, but it does have one problem. It is backward-looking data. BLS knows that and states the following on its web site:

"The most significant potential drawback to this or any model-based approach is that time series modeling assumes a predictable continuation of historical patterns and relationships and therefore is likely to have some difficulty producing reliable estimates at economic turning points or during periods when there are sudden changes in trend. BLS will continue researching alternative model-based techniques for the net birth/death component; it is likely to remain as the most problematic part of the estimation process."

Remember the jobless recovery of the first Bush term and the constant criticism about the poor economy? Why was the economy doing so well and yet job creation was so poor? It turns out that a great deal of the explanation is that the BLS underestimated the number of new jobs being created by small business. In the early years of the recovery, rather badly.

Likewise, the BLS data will overestimate jobs when the economy is slowing down. Is there some evidence that may be the case today? I think there is.

To the credit of the BLS, they are very transparent about their data. There are massive amounts of data available at www.bls.gov and the data on the birth/death ratio is at http://www.bls.gov/web/cesbd.htm. Now, let's examine the contribution of the birth/death ratio to the employment numbers.

Last month, the BLS estimated that there were 156,000 new jobs in the birth/death ratio category, which was 24,000 more jobs than they estimated were created for the month. OK, maybe no problem. Looking back over five years, the economy has created about that many new jobs during the month.

Except that they estimated 26,000 new small-business construction jobs. With home construction dropping, do we really think that the same number of new jobs was created in construction as in June of 2006 and 2005? Or that 153,000 new jobs in small-business construction have been created this year? Really?

In fact, since January, the BLS estimates for the birth/death ratio have added 747,000 new jobs of a total projected growth of 871,000 jobs, or 86% of the total of the jobs estimated supposedly created for the first half of the year.

Is there any other reason to believe that the birth/death ratio may be overstating employment as the economy slows? The always astute Paul Kasriel of Northern Trust thinks there is. He notes that in 2005 the contribution of the birth/death ratio (12-month average) to the overall employment numbers was well under 35%. Today it is over 56%. Given the recent numbers, that ratio is likely to rise.

"What has been happening to the relative contribution of birth/death estimates as the economy has slowed in the past year? The chart below shows that it has been rising. In the 12 months ended March 2006, the birth/death adjustment was contributing only 30.9% of the jobs to the change in nonfarm payrolls. The birth/death relative contribution has been trending higher since then. Notice that as the birth/death contribution to nonfarm payrolls has been trending higher, the percentage of small businesses saying that now is a good time to expand their operations has been trending lower. If existing small business managers do not think now is a good time to expand their operations, does it make sense that there are a lot of new small businesses starting up and hiring?