All that being said, if you've got a few bucks send it over to Baghdad Pups.

And now -- for our dogs.

Just this week, we learned that retail sales have fallen off a cliff, and so has industrial production. Unemployment claims are at steep-recession levels, and the Philadelphia Fed’s manufacturing index is falling at the fastest pace in almost 20 years. All signs point to an economic slump that will be nasty, brutish — and long.

How nasty? The unemployment rate is already above 6 percent (and broader measures of underemployment are in double digits). It’s now virtually certain that the unemployment rate will go above 7 percent, and quite possibly above 8 percent, making this the worst recession in a quarter-century.

And how long? It could be very long indeed.

Think about what happened in the last recession, which followed the bursting of the late-1990s technology bubble. On the surface, the policy response to that recession looks like a success story. Although there were widespread fears that the United States would experience a Japanese-style “lost decade,” that didn’t happen: the Federal Reserve was able to engineer a recovery from that recession by cutting interest rates.

But the truth is that we were looking Japanese for quite a while: the Fed had a hard time getting traction. Despite repeated interest rate cuts, which eventually brought the federal funds rate down to just 1 percent, the unemployment rate just kept on rising; it was more than two years before the job picture started to improve. And when a convincing recovery finally did come, it was only because Alan Greenspan had managed to replace the technology bubble with a housing bubble.

Now the housing bubble has burst in turn, leaving the financial landscape strewn with wreckage. Even if the ongoing efforts to rescue the banking system and unfreeze the credit markets work — and while it’s early days yet, the initial results have been disappointing — it’s hard to see housing making a comeback any time soon. And if there’s another bubble waiting to happen, it’s not obvious. So the Fed will find it even harder to get traction this time.

In other words, there’s not much Ben Bernanke can do for the economy. He can and should cut interest rates even more — but nobody expects this to do more than provide a slight economic boost.

Think about what happened in the last recession, which followed the bursting of the late-1990s technology bubble. On the surface, the policy response to that recession looks like a success story. Although there were widespread fears that the United States would experience a Japanese-style “lost decade,” that didn’t happen: the Federal Reserve was able to engineer a recovery from that recession by cutting interest rates.

But the truth is that we were looking Japanese for quite a while: the Fed had a hard time getting traction. Despite repeated interest rate cuts, which eventually brought the federal funds rate down to just 1 percent, the unemployment rate just kept on rising; it was more than two years before the job picture started to improve. And when a convincing recovery finally did come, it was only because Alan Greenspan had managed to replace the technology bubble with a housing bubble.

Consumer spending was softer in nearly all Districts. Retail sales were reported to have weakened or declined in Philadelphia, Cleveland, Richmond, Atlanta, Chicago, Minneapolis, and Kansas City; Dallas and San Francisco cited weak or sluggish sales; and Boston and New York indicated that sales were mixed and moderately below plan sales, respectively. Several Districts noted a reduction in discretionary spending by consumers and lower sales on big-ticket items. Several also reported increased activity at discount stores as consumers became more price conscious and shifted purchases toward less-expensive brands.

Manufacturing activity moved lower in most Districts, and contacts expressed heightened concern about the economic outlook. Several Districts noted that credit conditions were contributing to a high level of uncertainty on the part of contacts. Declines in manufacturing activity of varying degrees were reported in Boston, New York, Cleveland, Richmond, Chicago, St. Louis, Kansas City, San Francisco, and Dallas. Atlanta reported that production remained at a low level, while Minneapolis described conditions as mixed and Philadelphia noted a slight increase in activity.

Residential real estate and construction activity weakened or remained low in all Districts. Housing activity was reported to have moved lower in Boston, New York, Philadelphia, Chicago, St. Louis, Minneapolis, Dallas, and San Francisco. While still slow, residential markets showed some signs of stabilizing in Cleveland, Atlanta, and Kansas City. Several Districts noted continuing downward price pressures and an increasing supply of homes for sale due to rising foreclosures. However, the inventory of unsold homes was reported to have declined in areas of the Boston and Atlanta Districts as well as in Philadelphia and Cleveland.

One reliable proxy of housing values — the ratio of home prices to rents — indicates that in many cities prices are still too high relative to historical norms.

.....

The price-to-rent ratio, which provides one measure of how much of a premium home buyers place on owning rather than renting, spiked across the country earlier this decade.

It increased the most on the coasts and somewhat less in the middle of the country. Economy.com’s calculations show that while it remains elevated in many places, the ratio has fallen sharply to more normal levels in places like Sacramento, Dallas and Riverside, Calif.

.....

As of June, 2.8 percent of homes previously occupied by an owner were vacant. Nearly 1 in 10 rentals was without a tenant. Both numbers are near their highest levels since 1956, the earliest year for which the Census Bureau has such data.

.....

At the same time, Ms. Pestana said, her clients who are looking to buy are having a harder time lining up financing. One of her clients recently had to give up on a home after the lender that had offered a pre-approved loan changed its mind — a frequent occurrence, according to real estate agents and mortgage brokers.

“I am working harder than I have ever had to work to get a deal together and keep it together,” said Ms. Pestana, who has been a real estate agent for seven years.

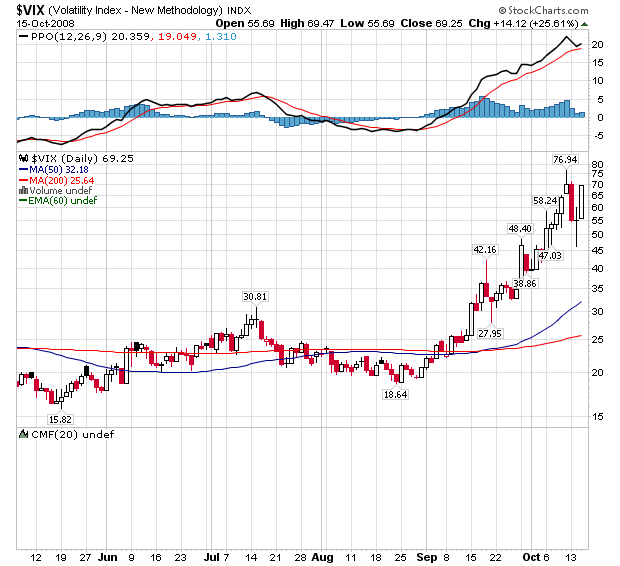

Troubles mounted for some of the world’s biggest hedge funds on Thursday as Highland Capital Management told investors it was shutting down two of its funds and details emerged of big losses at TPG-Axon.

The problems in the sector have set in motion a vicious cycle in the markets as hedge funds sell holdings to return money to worried investors, triggering further price declines and prompting more withdrawals. Investors pulled at least $43bn from hedge funds in September, according to TrimTabs Investment Research.

“Unfortunately, selling has begat selling as risk reduction and unwinding create spillover pressure on other funds with overlapping holdings,” Dinakar Singh, the founder of TPG-Axon said in a letter to investors at the end of September.

Banks and securities firms have reported more than $640 billion in losses, writedowns and credit provisions since the start of 2007 and raised $611 billion in capital to offset those losses, according to data compiled by Bloomberg. New York-based JPMorgan, the biggest U.S. bank by assets, reported third-quarter net income yesterday of $527 million and Wells Fargo in San Francisco earned $1.64 billion.

The U.S. Empire State index dropped to a -24.6 reading in October, following the September decline to -7.41. While the various components of the report were quite weak, one jumps out: The capital expenditure plans index moderated to 6.10 in October from 16.09, which unwinds the modest gains over the past two months and brings this measure to a new cycle-low. The drop raises the risk that businesses will indeed post the feared pullback in investment spending in the fourth quarter, following what appears to be a turn in the durable goods, factory goods, and nonresidential construction spending data starting in the middle of the third quarter.

The U.S. PPI report, with its 0.4% September headline drop but surprisingly firm 0.4% core (excluding food and energy prices) increase, revealed a year-over-year headline gain at the expected 8.7% from 9.6%, while the core year-over-year rate popped to 4.0% from 3.6%. The headline year-over-year rate is still well above what was the 26-year high of 7.4% as recently as January, hence showing how far the commodity price reversal still needs to go to reverse the price surge of the past year.

Retail sales fell 1.2 percent in September to a seasonally adjusted $375.5 billion, the Commerce Department said on Wednesday. It was the sharpest drop since August 2005 and far greater than the 0.7 percent decline economists had expected.

"We have an all-out consumer retrenchment under way," said National City Corp chief economist Richard DeKaser in Cleveland, adding he expected the economy to shrink in coming months.

House Speaker Nancy Pelosi is mulling recommendations from several economists that Congress act on an economic-recovery package that would cost taxpayers $300 billion, according to congressional aides, equivalent to about 2% of the country's gross domestic product.

The California Democrat envisions a bill that would include new spending on highways and bridges, extended benefits to unemployed workers, aid to cash-strapped states and a tax cut, congressional aides said. She has asked several House committees to examine details of a possible plan. And as part of the effort, Federal Reserve Chairman Ben Bernanke is expected to testify next week before the House Budget Committee on the state of the economy. Ms. Pelosi is expected to call lawmakers back to Washington in late November to take up the issue.

As bad as 2008 was, the current fiscal year, which began Oct. 1, is widely expected to be far worse. The director of the Congressional Budget Office recently estimated the annual deficit could hit $750 billion given the potential impacts from a possible recession and the financial markets' problems. Some private economists put the 2009 deficit at as much as $1 trillion.

On Tuesday, the White House budget office said the hole will look much deeper because accounting rules will force the administration to include all $250 billion of its bank recapitalization plan in the annual deficit as well. Under the Treasury's original plan -- focused on buying up troubled mortgage-related debt instruments from banks -- the government was expected to be able to exclude much of its spending from the annual deficit.

In economics, a public good is a good that is non-rivaled and non-excludable. This means, respectively, that consumption of the good by one individual does not reduce availability of the good for consumption by others; and that no one can be effectively excluded from using the good.[1] In the real world, there may be no such thing as an absolutely non-rivaled and non-excludable good; but economists think that some goods approximate the concept closely enough for the analysis to be economically useful.

First, Treasury is announcing a voluntary capital purchase program. A broad array of financial institutions is eligible to participate in this program by selling preferred shares to the U.S. government on attractive terms that protect the taxpayer. Second, after receiving a recommendation from the boards of the FDIC and the Federal Reserve, and consulting with the President, Secretary Paulson signed the systemic risk exception to the FDIC Act, enabling the FDIC to temporarily guarantee the senior debt of all FDIC-insured institutions and their holding companies, as well as deposits in non-interest bearing deposit transaction accounts. Regulators will implement an enhanced supervisory framework to assure appropriate use of this new guarantee.

Third, to further increase access to funding for businesses in all sectors of our economy, the Federal Reserve has announced further details of its Commercial Paper Funding Facility (CPFF) program, which provides a broad backstop for the commercial paper market. Beginning October 27, the CPFF will fund purchases of commercial paper of 3 month maturity from high-quality issuers.

Some of the big banks were unhappy about the government taking equity stakes, but acquiesced under pressure from Treasury Secretary Henry Paulson in a meeting Monday. During the financial crisis, the government has steadily increased its involvement in financial markets, culminating with a move that rivals the breadth of the government's response to the Great Depression. It intertwines the banking sector with the federal government for years to come and gives taxpayers a direct stake in the future of American finance, including any possible losses.

France, Germany, Spain, the Netherlands and Austria committed 1.3 trillion euros ($1.8 trillion) to guarantee bank loans and take stakes in lenders, racing to prevent the collapse of the financial system.

The announcements came as Britain took majority stakes today in Royal Bank of Scotland Group Plc and HBOS Plc. The coordinated steps followed a pledge yesterday by European leaders to bolster market confidence as the global economy slides toward recession.

``What it should do is stabilize the banking system,'' said Peter Hahn, a fellow at London's Cass Business School and former managing director at Citigroup Inc. ``Will it stop us from having a recession? No, nothing is going to stop us from having a recession.''

The agreement among heads of the 15 countries using the euro helped trigger a rally in stocks and the euro after a market rout. The Dow Jones Stoxx 600 Index rebounded a record 10 percent today, after slumping 22 percent to the worst drop in its two-decade history last week. The currency had its biggest gain in three weeks, climbing 0.9 percent to $1.3526.

1) Mortgage-backed securities purchase program: This team is identifying which troubled assets to purchase, from whom to buy them and which purchase mechanism will best meet our policy objectives. Here, we are designing the detailed auction protocols and will work with vendors to implement the program.

2) Whole loan purchase program: Regional banks are particularly clogged with whole residential mortgage loans. This team is working with bank regulators to identify which types of loans to purchase first, how to value them, and which purchase mechanism will best meet our policy object

.....

4) Equity purchase program: We are designing a standardized program to purchase equity in a broad array of financial institutions. As with the other programs, the equity purchase program will be voluntary and designed with attractive terms to encourage participation from healthy institutions. It will also encourage firms to raise new private capital to complement public capital.