We'll be back on Monday.

Overall, sales fell 0.3%, reversing the gains seen in September and October, according to the International Council of Shopping Centers. The trade group had cut its November forecast twice to a sales increase of 3% to 4%.Turning to the high-frequency weekly indicators, the BLS reported new jobless claims fell again, to 457,000. Together with today's NFP number, this does suggest that job growth may actually arrive this month.

Sales at U.S. retailers rose an estimated 1.6 percent during the U.S. Thanksgiving weekend, the start to the key holiday shopping season, according to ShopperTrakThe ICSC weekly seasonally adjusted weekly data on U.S. chain store retail sales were unchanged WoW, but up +3.1% YoY.

The unemployment rate edged down to 10.0 percent in November, and nonfarmpayroll employment was essentially unchanged (-11,000), the U.S. Bureau of Labor Statistics reported today. In the prior 3 months, payroll job losse had averaged 135,000 a month. In November, employment fell in construction manufacturing, and information, while temporary help services and health care added jobs.

The NFIB has teased Tuesday's release of its monthly SBET, and the picture is not pretty. Their economist, Bill Dunkelberg:

NFIB Jobs Statement: Expect Coal in Small Business StockingsAnd, to take a page from my playbook:“The job generating machine is still in reverse as November’s report represents the 22nd consecutive month with more small business owners reporting employment declines than employment increases. Sales are not picking up, so survival requires continuous attention to costs – and labor costs loom large.

“Eight percent (seasonally adjusted) of owners reported unfilled job openings, unchanged since August. Over the next three months, 17 percent plan to reduce employment (up one point), and 7 percent plan to create new jobs (down two points), yielding a seasonally adjusted net negative 3 percent of owners planning to create new jobs, two points worse than October. Still more firms are planning to cut jobs than planning to add.

“The consumer is the key to job creation, when businesses have more customers, they will hire more workers. Workers must generate enough sales to pay their salaries, or the firm loses money."More on this when the SBET is released on Tuesday and the data is fully available, but it appears that much of this report will actually be a downtick from last month's. If that is, in fact, the case, it's another very troubling development.

Reports from the twelve Federal Reserve Districts indicate that economic conditions have generally improved modestly since the last report. Eight Districts indicated some pickup in activity or improvement in conditions, while the remaining four--Philadelphia, Cleveland, Richmond, and Atlanta--reported that conditions were little changed and/or mixed.Consumer spending was reported to have picked up moderately since the last report, for both general merchandise and vehicles; a number of Districts noted relatively robust sales of used autos. Most Districts indicated that non-auto retailers were holding lean inventories going into the holiday season. Tourism activity varied across Districts. Manufacturing conditions were said to be, on balance, steady to moderately improving across most of the country, while conditions in the nonfinancial service sector generally strengthened somewhat, though with some variation across Districts and across industries. Residential real estate conditions were somewhat improved from very low levels, on balance, led by the lower end of the market. Most Districts reported some pickup in home sales, though prices were generally said to be flat or declining modestly; residential construction was characterized as weak, but some Districts did note some pickup in activity. Commercial real estate markets and construction activity were depicted as very weak and, in many cases, deteriorating.

Financial institutions generally reported steady to weaker loan demand, continued tight credit standards, and steady or deteriorating loan quality. In the agricultural sector, the fall harvest was delayed in the eastern half of the nation due to excessively wet conditions during October and early November. Most energy-producing Districts noted a slight uptick in activity in the sector since the last report. Labor market conditions remained weak since the last report, though there were signs of stabilization and scattered signs of improvement. While some Districts reported upward pressure on commodity prices, they saw little or no indication of upward wage pressures or of any significant increase in prices of finished goods.

Short version: things are moving in the right direction. The vast majority of districts sees improvement (8 of 11 districts saw things get better), but we have a long way to go. Let's break the data down into some smaller pieces.

Let's break the data down into smaller pieces:

Consumer spending strengthened since the last report, with sales of both general merchandise and autos improving across much of the country. Non-auto sales were reported to have picked up in the New York, Philadelphia, Cleveland, Richmond, Atlanta, Kansas City, and San Francisco Districts; sales were described as steady or mixed in the Boston, Chicago, Minneapolis, and Dallas Districts. St. Louis described retail sales as below expectations and down from a year earlier. Auto sales generally improved since the last report, in some cases rebounding from a brief dip after the "cash-for-clunkers" program ended. Increased vehicle sales were reported from New York, Philadelphia, Richmond, Chicago, St. Louis, and Dallas, while sales were described as flat or mixed in the Cleveland, Minneapolis, Kansas City, and San Francisco Districts. A number of Districts reported that used vehicles have been selling better than new ones.

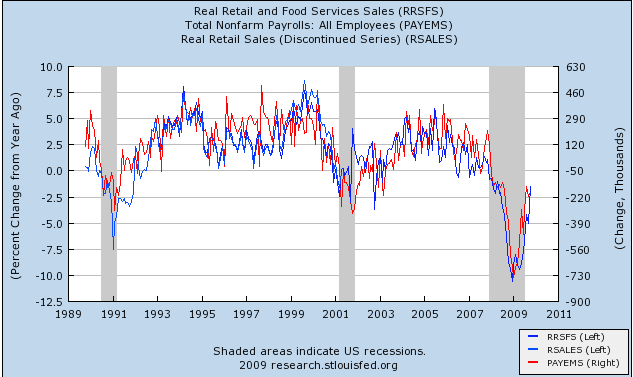

Here is a chart of the relevant data:

Notice the year over year number has been increasing all year. This is to be expected as the number is coming off of an incredibly low bottom. However, also note the gray lines on the chart. These represent month to month increases and decreases. We've had nine monthly reports this year. Three have shown a decrease. That's not bad for an economy that was in a recession for most of the year. While I would like to see the month to month numbers increase, that's not going to happen in the near future.

Most Districts reported mixed to moderately improving manufacturing conditions since the last report. New York, Philadelphia, Cleveland, Minneapolis, Kansas City, and San Francisco all noted modest increases in manufacturing activity within their Districts. Manufacturing conditions in the Boston and Dallas Districts were characterized as mixed, with some improvement noted for biopharmaceuticals companies in Boston and high-tech manufacturing firms in Dallas. By contrast, Richmond and Chicago both reported that manufacturing activity had leveled off since the last report, while activity continued to decline in the Atlanta and St. Louis Districts, although at a somewhat slower pace than the last report. Tighter credit limited the ability of customers to place new orders in the Richmond District, while in the Chicago District, contacts noted a slowdown in the restocking of inventories. Increases in activity related to the transportation industry were cited in the Chicago, St. Louis, Cleveland, and Kansas City Districts, although such activity was mixed in the Dallas District and reported as declining in the San Francisco District. Several Districts noted an uptick in food-related production.

Here is a chart of the relevant data:

The ISM manufacturing index has rebounded from incredibly low levels to print numbers in the expansion area (plus 50) over the last four months. Looking back before recession, these numbers are in line with what we were seeing pre-recession. Also note these numbers are consistent the the continual improvement we've witnessed in the various regional Federal Reserve surveys (the Empire State index etc...). Bottom line: manufacturing has rebounded.

Activity in the service sector generally picked up since the last report, though results were mixed across Districts and across service industries. New York and Philadelphia reported that service-sector activity overall remained steady to up slightly, while St. Louis noted expanding activity. The information technology industry was reported to be showing improvement in the Boston, Minneapolis, and Kansas City Districts. A pickup in activity at staffing firms was reported by Boston and Dallas, whereas New York noted that activity remained sluggish. Strength in health services was noted in the Boston and Richmond Districts. Shipping activity was characterized as flat in the Cleveland, Atlanta, and Kansas City District, while Dallas reports some gain; however, Dallas and Atlanta both noted particular weakness in rail shipping activity. Professional and business support firms reportedly registered some improvement in the St. Louis and Minneapolis Districts but flat to declining activity in Richmond and San Francisco.

Here is a chart of the relevant data:

Like the manufacturing sector, this number has rebounded from low levels to show expansion. This index (like the manufacturing number), has been steadily increasing sign October of last year.

Home sales and construction activity improved across much of the nation, though prices were generally said to be flat or still declining somewhat. A majority of Districts reported that the lower-priced segment of the housing market has outperformed the high end. Increases in sales activity were reported in the Boston, Cleveland, Richmond, Atlanta, Chicago, Minneapolis, Kansas City, Dallas, and San Francisco Districts, whereas sales were described as steady or mixed in the New York and Philadelphia Districts. Multifamily housing markets deteriorated further in the New York and Chicago Districts. More broadly, a number of eastern Districts reported continued declines in home prices--specifically, Boston, New York, Philadelphia, and Richmond. In contrast, prices were said to have firmed somewhat in the Dallas and San Francisco Districts and stabilized in the Chicago and Kansas City Districts. Most reports maintained that the lower end of the market has outperformed the higher end: New York, Philadelphia, Richmond, Atlanta, Minneapolis, and Kansas City all noted relative weakness at the high end of the market, with relative strength at the lower end; in most cases, this strength was largely attributed to the homebuyer tax credit (which was recently reinstated and expanded to include existing owners).

Existing home sales have clearly bottomed and are now moving higher.

New home sales have bottomed, although they are not as strong as existing home sales.

And while home prices are still declining, we're seeing clear improvement in the pace of the decline.

Short version: housing is getting better as well.

And then there is employment:

Labor market conditions remained weak since the last report, with further layoffs, sluggish hiring, and high levels of unemployment in most Districts. However, contacts in the Atlanta, Cleveland, and Richmond Districts reported that the pace of job cuts generally slowed in their regions, and most contacts in the Dallas District reported stable employment levels. Despite generally weak employment conditions, some signs of improvement were noted. For example, contacts in Boston reported that they were beginning to hire and reverse pay cuts or freezes that were implemented earlier in the year, and contacts in the St. Louis District reported that the service sector had started to expand recently. Expectations for the holiday season were mixed across Districts, with contacts in the New York and Dallas Districts reporting lighter-than-normal seasonal hiring and/or increases in the hours of existing employees, as opposed to hiring temporary workers, to meet the seasonal demand. On the other hand, most retailers in the Richmond District have hired the usual number of seasonal workers this year.

The good news is the front end of the labor market -- initial unemployment claims -- continues to decrease:

The 4-week moving average has been dropping since the Spring.

However, there is still no job creation. However, the rate of establishment job losses continues to decrease indicating we should start seeing job creation within the next 3-6 months.

Overall, the Beige Book indicates things are moving in the right direction.

“The NMI (Non-Manufacturing Index) registered 48.7 percent in November, 1.9 percentage points lower than the 50.6 percent registered in October, indicating contraction in the non-manufacturing sector after two consecutive months of expansion. The Non-Manufacturing Business Activity Index decreased 5.6 percentage points to 49.6 percent, reflecting contraction after three consecutive months of growth. The New Orders Index decreased 0.5 percentage point to 55.1 percent, and the Employment Index increased 0.5 percentage point to 41.6 percent. The Prices Index increased 4.8 percentage points to 57.8 percent in November, indicating an increase in prices paid from October. According to the NMI, six non-manufacturing industries reported growth in November. Respondents’ comments remain cautious about business conditions and reflect concern over the length of time for economic recovery.”

....

WHAT RESPONDENTS ARE SAYING …

“Capital markets remain very tight; lenders are not releasing funds for development projects, limiting expansion.” (Accommodation & Food Services)

“Fourth quarter still looking grim, but potential upturn for Q1 2010.” (Professional, Scientific & Technical Services)

“No one trusts that the recovery is real. Seems everything and everyone is in a holding pattern.” (Public Administration)

“Business is still flat.” (Wholesale Trade)

“U.S. business remains better than 2007 levels, although it’s been through personnel and cost reductions that we are now profitable. Business continues to be about 8 percent below 2008 levels.” (Real Estate, Rental & Leasing)

So first, to try to demonstrate that I'm not Chicken Little, here are some excerpts that I think portray a balanced point of view (in response to NDD's challenge):

Dec 1And on C4C:Industrial Production appears to have carved out at least (let's hope) a temporary bottom, and is one metric we can look at as a positive, notwithstanding that it's taken a whole lot of government largesse to get us there.

November 24

This [referring to FOMC minutes excerpt], to me, encapsulates exactly where we are right now -- still on life support without a clue as to how the patient might fare if it were withdrawn. In all, I think the FOMC minutes were another "things are less bad" report, but there are still very real concerns about the fragility of whatever recovery we may experience and the ease with which it might jump the tracks.

November 24

Though not necessarily cause for concern, the decline [in the CFNAI 3-mo MA] is certainly worth keeping an eye on. As one data point does not a trend make, I'll simply suggest this could be a yellow flag.

November 9

There were, in my opinion, only two needles to be found in Friday’s NFP haystack:

1) The previous two months’ revisions were positive to the tune of about 91k

2) There was a 34k add in temp help (often a leading indicator for the labor market)November 2

To be crystal clear on where I stand:

1) My primary concern is -- and always has been -- about the "handoff" or sustainability of growth. I think we can all agree that the government can't -- and shouldn't -- prop up the economy indefinitely. I get all the Keynesian stuff, but the government "bridge," such as it is, has to let you off on the other side at some point. My visibility as to where that might be is still extremely hazy.

2) I was for the stimulus package. In fact, I was for a bigger stimulus package. And while I'm not bemoaning -- only pointing out -- that last week's 3.5 print was largely government subsidized, I always seem to be left wondering, "Where do we go from here?" What is going to be the driver, the growth catalyst, to get GDP back up the sustainable trend (~3.0 or so) we require to get to fuller employment and see some wage growth? This is something that could have been -- should have been -- under discussion six months ago and is, as best I can see, still not.

3) My concern about sustainability is focused on the consumer.Sept. 19

I’d be a fool not to acknowledge that most of the recent economic releases have been better than expected, particularly as relates to the [sic] most of the headline numbers. However, I’m still not sold on the sustainability, and in some cases I don’t necessarily like what I see lurking beneath the surface. I continue to believe that when it comes time for the government to hand-off the spending baton to the American consumer, the transition might not go as smoothly as everyone seems to think it will.

The question needs to be asked: How many more vehicles/driver are we going to put on the road? How many cars/driver do we really need? Further, I will respectfully disagree with Bonddad and state for the record that there’s little doubt in my mind that Cash for Clunkers pulled forward some (perhaps unquantifiable) amount of future sales. The run rate didn’t go from ~9MM annually to ~13MM annually on its own. Unfortunately, it appears we’re headed back down toward ~9MM again, so it’s hard to believe the Clunker program didn’t cannibalize some Q4 sales. Keep in mind, too, that scrappage is about 12MM vehicles/year so we are, in fact, taking cars off the road, which would be consistent with the trend of the chart above beginning to turn down.I think my Sept. 19 comment -- 2 1/2 months later -- is beginning to play out, and as NDD mentioned, Paul Krugman invoked the specter of a double-dip on his blog just yesterday.

To me, it really all boils down -- as I've said countless times -- to the consumer and jobs, jobs, jobs. To that end, I intend to have some employment-related posts (with what I hope will be some nifty chart work) up fairly soon. (Let's just say I don't think we need to debate whether or not this will be a jobless recovery -- it already is.)

Dubai World began talks with banks to restructure $26 billion of debt, including $3.5 billion owed by property unit Nakheel, and said the remainder of its liabilities are on “a stable financial footing.”

Debt from subsidiaries including Infinity World Holding, Istithmar World and Ports & Free Zone World will be excluded from the negotiations, Dubai World, one of the emirate’s three main state-related holding companies, said in a statement. The cost to protect Dubai debt against default fell to the lowest since Nov. 25. Dubai’s main equity index dropped 6.6 percent.

Dubai is seeking to delay payments on less than half its $59 billion of liabilities, easing the potential damage to banks recovering from $1.7 trillion of losses and writedowns from the global crisis. Shares worldwide recovered some of the losses suffered since Dubai announced it would seek a “standstill” agreement on all of Dubai World’s debt as the Dow Jones Euro Stoxx 600 gained 1.2 percent and the MSCI Emerging Markets Index showed the first back-to-back gains in two weeks.

While there is concern with commodity prices, also note that the last three comments deal with increased activity in three different areas. These comments are included because they are representative of what people are hearing. Simply put, this is more good news.

- "Becoming concerned about the value of the U.S. dollar." (Apparel, Leather & Allied Products)

- "Low value of the dollar driving commodity costs higher." (Food, Beverage & Tobacco Products)

- "Demand from automotive manufacturers remains strong and building." (Fabricated Metal Products)

- "Capital construction seems to be picking up, and we are seeing more jobs that are bid out." (Electrical Equipment, Appliances & Components)

- "Steady increase in business." (Primary Metals)

Sunday's New York Times had two Page 1 above-the-fold stories that, in my opinion, cast serious doubts on what type of "recovery," for lack of a better word, we're in store for. First up is "Food Stamp Use Soars Across U.S., and Stigma Fades." The lede: "With food stamp use at record highs and climbing every month, a program once scorned as a failed welfare scheme now helps feed one in eight Americans and one in four children." As concerned as I've been for some time about what's going with our economy, these numbers startled even me. This story is a real eye-opener, and should be a wake-up call for us all.

The other noteworthy story appeared right beside the food stamp story: "U.S. To Pressure Mortgage Firms for Loan Relief." Lede: "The Obama administration on Monday plans to announce a campaign to pressure mortgage companies to reduce payments for many more troubled homeowners, as evidence mounts that a $75 billion taxpayer-financed effort aimed at stemming foreclosures is foundering."

We continue to see an ever-increasing number of homeowners underwater on their mortgages, and there's concern that another wave of defaults and/or foreclosures is headed our way in 2010. So you'll excuse my muted reaction to the fact that initial claims for unemployment insurance dropped into the mid-400k range. The government has stepped in and to fill the spending void created by the tightening of purse-strings on the part of both businesses and consumers. But there are underlying, structural issues at play here (like our collective debt-to-income ratio) that the government simply cannot address.

But let's shift gears and look at the stuff that matters in actually making the recession call.

Employment is still a mess, although we know it's less of a mess and a lagging indicator.

Industrial Production appears to have carved out at least (let's hope) a temporary bottom, and is one metric we can look at as a positive, notwithstanding that it's taken a whole lot of government largesse to get us there.

Real Income continues to go nowhere fast. With unemployment as high as it is and record slack in the labor market, it's hard to envision a scenario any time soon wherein workers will have any leverage to seek higher wages. Just too many people looking for work now to get any wage inflation.

Retail Sales are flatlining for some time now, and early reports (as of Sunday night) for Black Friday seem to indicate heavier foot traffic, a very modest increase in spending, and a laser-like focus on the part of the consumer for discounted goods.

In a nutshell, we may technically be out of recession by virtue of what will likely be two consecutive quarters of GDP growth (although frankly I think the NBER is going to ponder this recession-end call long and hard before they make it), but it is clear that tens of millions of Americans don't much care what economists or the NBER are -- or aren't -- calling it, as they're still feeling significant distress.

I started this post on Sunday night, and intended to finish it up on Monday night with some final thoughts. Little did I know that Paul Krugman would finish it for me in his Monday column:

"There’s a pervasive sense in Washington that nothing more can or should be done [to promote job growth], that we should just wait for the economic recovery to trickle down to workers.

"This is wrong and unacceptable.

"Yes, the recession is probably over in a technical sense, but that doesn’t mean that full employment is just around the corner. Historically, financial crises have typically been followed not just by severe recessions but by anemic recoveries; it’s usually years before unemployment declines to anything like normal levels."

And, finally, it looks like Black Friday sales might not have been up at all.

Mr. Crane is part of a growing group of underemployed -- people in part-time jobs who want full-time work or people in jobs that don't employ their skills. Since the recession began two years ago, the number of people involuntarily working part-time jobs has more than doubled to 9.3 million, according to the federal Bureau of Labor Statistics, the highest number on record.

The proliferation of underemployed could represent a profound reordering of the employment structure. Many people who had comfortable full-time jobs with benefits and advancement opportunities now are cobbling together smaller jobs often at lower pay, in a shift that economists say could become permanent for many individuals stuck in the cycle. Underemployment, along with unemployment, is widely seen as a force slowing the economic recovery.

The trend has been building for years, says Robert Reich, who served as labor secretary under President Bill Clinton and now is a professor of public policy at the University of California, Berkeley. "For decades, workers have been watching their salaries and benefits erode," says Mr. Reich, who took an 8% pay cut last week, along with the rest of the Berkeley faculty.

"We are subjecting millions of people to a standard of living below that which they could achieve if the economy were at full capacity," he says. "Underemployment means that many more people who can't spend as much as they otherwise would."

This is from today's research note from David Rosenberg:

Click for a larger image.

Adding, for the record: Rosie's piece wasn't published until hours after this post printed, lest anyone wonder who was ripping off whom.

[t]he worry is that not as many people are being laid off because there aren't as many people at work in construction and Christmas rush goods-producing jobs to be laid off, and that we should be at the very least cautious in interpreting one-week movements in unemployment insurance claims. Perhaps we want to argue that the labor market is improving in a sense, but we should be clear on what sense that improvement is. It is: in a normal year new weekly unemployment insurance claims rise by about 100,000 in the month before Thanksgiving; this year they have risen by only about 50,000. So things are getting better.

Reading blogs that in any way write about economics has generally become an exercise in utter futility. According to most good news is either propagated by corporate whores who are blind to the realities around them or presented without considering "all" the facts. All government statistics and all economists are wrong -- unless they support or present a bearish viewpoint. Then the facts are treated as irrefutable truths presented by intellectual gods. And Goldman Sachs or the Federal Reserve manipulated everything to further some plot. In other words, ridiculous conspiracy theories are far more common than simple factually based analysis. How did things get so out of line?

There are several reasons. The first and most obvious is, "if it bleeds it leads." This is a saying from the days when newspapers were the predominant form of presenting and communicating information. Bloody pictures and sensationalistic headlines simply sold more newspapers. Translate that to the blogsphere and proclamations that the economy is going to hell will probably attract more readers. For reasons that I still don't understand, train wrecks are fun to watch. I'm reminded here of the album by Megadeath titled Peace Sells ... But Who's Buying?

Then there is the issue that many people in the blogsphere were right about the economy. Over the last three or so years, the only people who issued any warnings about the US' economic trajectory were blogs. At first they were the lunatic fringe, the voice in the wilderness. But after the crash happened more people tuned into blogs to get their financial information. Readership increased. But as the facts changed -- as we saw economic indicators start to bottom and then turn positive -- blogs did not change their opinions. The reasons here are two fold. First, many people made a name for themselves by being bearish. Changing their perception would mean giving up the quality that made them famous in the first place and thereby threaten their readership. The second is many people have a preconceived perspective -- that is, some people are fundamentally bearish regardless of the economic environment. Just as importantly, there are some who want things to be bad in order to create an environment where fundamental change is more likely. In other words, these people have a clear political agenda; they simply use economics to accomplish these ends. There is nothing wrong with this. But their bias should be understood and clearly made.

Third, there is the simple fact that people who write about the economy don't understand the economy. Here is a classic example. The unemployment rate is a lagging economic indicator. This means it goes down after the economy starts growing. The intuitive reason for this is simple. During a recession businesses cut production and lay people off. As the economy starts to grow, businesses first increase production and the hours that their existing work force works. Then, as demand picks up more and more, businesses start to hire again. However, reading the economic blogsphere it becomes very obvious that people writing about the economy don't know about this relationship. I'd love to tell you that unemployment will suddenly drop to 5% next quarter. But that's just not going to happen because that's not the way the economy works. Certain things happen at certain times in economic cycles.

And finally there are the conspiracy theories floating around the Internet. According to some the entire crash was orchestrated by Goldman Sachs. According to others, the Federal Reserve is part of a secret plot to do ... something. The reality is the economic meltdown was caused by numerous, inter-related events coming together in what is literally a once-in-a-lifetime perfect economic storm. It's going to take a long time to sort through the mess to figure out what went wrong and how all of those pieces fit together. In difficult times it's easy to scapegoat parties and institutions. The reality is it's a lot more complicated.

So, here's the reality of where we are. The economy is back from the brink; we're no longer falling off a cliff. Last quarter the economy grew by 2.8%. Yes, that was the result of the stimulus -- which is exactly what is supposed to happen at the end of a recession. However, we have a lot of work to do. The unemployment rate is still over 10.2%. Unemployment benefits must be increased and extended. And plans to get the unemployment rate down should be initiated.