We'll be back on Tuesday.

Intel Corp., the world’s largest maker of computer chips, is increasing production and commanding higher prices as an export boom puts American manufacturing at the forefront of the economic recovery.Santa Clara, California-based Intel’s factories are operating at 80 percent of capacity, up from a record low of about 50 percent last year in the midst of the recession. The average selling prices of personal computer processors have risen a total of 12 percent over the past two quarters.

Overseas demand for U.S.-made goods from semiconductors to printers is boosting the fortunes of manufacturing, which has been shrinking as a proportion of the economy in 13 of the past 14 years. As a result, trade may add to growth for the first time in a post-recession year since World War II, says Morgan Stanley economist Richard Berner.

“U.S. manufacturing has really seen a renaissance of sorts driven by improved competitiveness and strength in global markets,” said Joseph Carson, director of economic research at AllianceBernstein LP in New York. “Exports have been the key driver of growth. We think it’s a new trend.”

Net exports, or the difference in value between what the U.S. sends overseas and what it buys from abroad, will add about 0.3 percentage point to gross domestic product this year, according to Berner, Morgan Stanley’s co-head of global economics in New York. He forecasts economic growth of 3.4 percent in 2010 after last year’s 2.4 percent contraction.

We noted this trend in several places:

Consumer delinquency rates are dropping at U.S. retailers and banks such as American Express Co. and Bank of America Corp., signaling an incipient lending thaw that may spur economic growth.Past-due loans at Bank of America, the second-largest card lender, fell for a fifth month in April and by the most in four years, while AmEx’s delinquencies were down 34 percent from a year earlier. Target Corp., the second-largest U.S. discount retailer, last week reported its lowest delinquency rate in the latest quarter since the second quarter of 2008.

Let's look at some data:

Starting in 2008, households started to decrease their debt holdings. Considering the overall level (there was nearly as much household debt as GDP) this was a healthy development.

As a result, debt service payments decreased, as did

The household financial obligations as a percent of disposable income.

Analysts said there was a heightened belief that Asian economies and the US could decouple from the problems in Europe.

“The theory of a decoupling of the rest of the world from the problems in the eurozone seems to be taking hold, following the theory frequently heard in 2008 of the emerging markets decoupling themselves from the recession of the industrialised world,” said Ulrich Leuchtmann at Commerzbank.

He said the reasoning was obvious: the exposure of the financial systems in Asia and the US to the stricken countries of the eurozone was small and economic effects were small as Asia, not Europe, was the engine of the global recovery.

“It makes no difference short-term whether the decoupling theory is correct or not,” said Mr Leuchtmann.

I agree the selling was overdone. The EU has proposed a $1 trillion dollar package to help with the situation. Governments are cutting spending (which is good and bad at the same time). In short -- action is being taken.

HOWEVER, anytime I see the word "decoupling" I laugh. The reality is the world is incredibly inter-connected now; there is no way the impact of one region does not impact another region. It's just not possible. Witness the inverse trading relationship between the dollar and the euro.

U.S. stock markets are oversold and may rally strongly in the next few days, said investor Barton Biggs, who runs New York-based hedge fund Traxis Partners LP.“I think they’re going to stabilize in this general area, and then we’re going to have a significant move to the upside,” Biggs, whose flagship fund returned three times the industry average last year, said in a Bloomberg Television interview.

Biggs recommended buying U.S. stocks last year when benchmark indexes sank to the lowest levels since the 1990s. The Standard & Poor’s 500 Index rallied 23 percent in 2009 as governments worldwide mounted stimulus programs to counter a recession. On March 22 this year, Biggs told Bloomberg TV U.S. stocks had the potential to rally a further 10 percent. The S&P 500 has since declined 8.4 percent.

.....

His views are at odds with Eric Sprott, manager of the best-performing Canadian mutual fund with at least $1 billion in assets in the past 10 years. The S&P 500’s month-long slump is the beginning of a collapse that will drive the measure below its weakest level of 2009 in the next year, Sprott said.

The $1 trillion European rescue package announced May 10 has failed to stop the global equity slump, indicating investors are skeptical that efforts to address the debt crisis will work, said Sprott, who manages the Sprott Canadian Equity Fund. He’s buying gold and betting against stocks.

“The European concerns are serious, and I take them seriously,” Biggs said. “I just don’t think that the worst is going to happen.”

Initial jobless claims fell in the May 22 week but not by much. Claims were down 14,000 to a higher-than-expected level of 460,000. In a partial offset, the prior week was revised 3,000 higher to 474,000. Improvement in the latest week fails to offset prior increases, reflected in the four-week average which rose for a second week, up 2,250 to 456,500. The month-to-month look is mixed with the four-week average showing marginal improvement while the latest week shows a marginal increase.

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 3.0 percent in the first quarter of 2010, (that is, from the fourth quarter to the first quarter), according to the "second" estimate released by the Bureau of Economic Analysis. In the fourth quarter, real GDP had increased 5.6 percent.

The GDP estimates released today are based on more complete source data than were available for the "advance" estimate issued last month. In the advance estimate, the increase in real GDP was 3.2 percent (see "Revisions" on page 3).

The increase in real GDP in the first quarter primarily reflected positive contributions from personal consumption expenditures (PCE), private inventory investment, exports, and nonresidential fixed investment that were partly offset by negative contributions from state and local government spending and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The deceleration in real GDP in the first quarter primarily reflected decelerations in private inventory investment and in exports, a downturn in residential fixed investment, a larger decrease in state and local government spending, and a deceleration in nonresidential fixed investment that were partly offset by an acceleration in PCE and a deceleration in imports.

THE STOCK MARKET STAGED an impressive recovery from steep early losses Tuesday, but was it a case of the symptoms being relieved while the underlying cause of the malady remains?Reports that North Korea had put its military on alert last week supposedly in preparation for a confrontation with the South over the North's alleged sinking of a South Korean only served to upset markets already anxious about the European debt situation.

The latter was encapsulated in a single interest rate, three-month Libor, or the London interbank offered rate. This money market benchmark continued its upward creep, rising another three basis points (.03 percentage points) and a total of seven basis points over the past five trading sessions.

That sounds trivial, but in percentage terms that's significant, given the rise brought Libor to 0.53625%. That's roughly double Libor's level early in the year and the highest since early 2009, when the worst of the credit crisis was fading. Remember that the federal funds target set by the Federal Reserve has remained unchanged throughout at 0-0.25%.

The widening in the spread between the Fed-set overnight funds rate and three-month Libor, which is set by a survey of major international banks by the British Bankers Association at late morning in London, reflects the higher rates that some European banks are having to pay. The money market is demanding a premium from banks, especially those that own lots of bonds from the weak-credit governments of Greece, Portugal, Spain, Ireland and Italy.

Here's why this is an issue. Consider this chart of the a2/p2 spread from the US

Notice the huge jump in the short-term rates in the US at the height of the financial crisis. While Libor is nowhere near those levels, a sharp increase in short-term rates is indicative of problems in the financial market. That's what the real issue is here.

Orders for durable goods rose in April for the fourth time in five months, pointing to strength in U.S. manufacturing at the start of the second quarter.

The 2.9 percent increase in bookings for goods meant to last at least three years was the biggest in three months and followed little change in March, figures from the Commerce Department showed today in Washington. Orders excluding transportation unexpectedly fell after revisions showed even bigger increases in prior months.

Rising exports and lean inventories are prompting companies to place more orders with factories, keeping factories at the forefront of the recovery from the worst recession since the 1930s. Corporate and consumer demand that stokes more job growth may help the expansion weather the European debt crisis.

I use to joke they should report this number ex-Boeing, but that hasn't caught on.

The good news is the overall number us up, but it was disproportionately effected by durable goods. However, this is not the only reason for the overall increase over the last year or so:

Instability in sovereign debt markets poses another serious risk. It has highlighted the need for the euro area to strengthen its institutional and operational architecture. Bolder measures need to be taken to ensure fiscal discipline, says the Outlook.Several countries are already taking early action to enhance the credibility of their fiscal consolidation plans and this is very welcome.

“This is a critical time for the world economy,”said OECD Secretary-General Angel Gurría. “Coordinated international efforts prevented the recession from becoming more severe but we continue to face huge challenges. Many OECD countries need to reconcile support to a still fragile recovery with the need to move to a more sustainable fiscal path. We also need to take into account the international spill-overs of domestic policies. Now more than ever, we need to maintain co-operation at an international level.” (Read the full speech).

With a huge debt burden weighing on many OECD countries and the strengthening recovery, the emergency fiscal measures provided by governments to tackle the crisis must be removed by 2011 at the latest, the Outlook says. It adds that the pace of such action must be appropriate to particular conditions and the state of public finances in each country.

| 09/30/2009 | 11,909,829,003,511.75 |

| 09/30/2008 | 10,024,724,896,912.49 |

| 09/30/2007 | 9,007,653,372,262.48 |

| 09/30/2006 | 8,506,973,899,215.23 |

| 09/30/2005 | 7,932,709,661,723.50 |

| 09/30/2004 | 7,379,052,696,330.32 |

| 09/30/2003 | 6,783,231,062,743.62 |

| 09/30/2002 | 6,228,235,965,597.16 |

| 09/30/2001 | 5,807,463,412,200.06 |

| 09/30/2000 | 5,674,178,209,886.86 |

One of the data points that has been getting some attention is the total withholding tax receipts, as reported by the IRS.[emphasis mine]

According to the table below, it is down year over year. Some are interpreting this to contradict BLS, and likely means that the improving jobs data are bogus. Bill King specifically noted that“as of May 20, IRS data shows Withheld Income & Employment Taxes declined 3.36% y/y. This means income is still declining and by extension, meaningful jobs are still decreasingThat certainly is a possibility. Might there be a better, higher probability explanation?

I am less sure of that conclusion. While I have been skeptical over the years about BLS model changes, I do not believe they are simply making up numbers to please their political masters. Before jumping to conclusions, I suggest we consider other possibilities: If the Employment data is okay, then what might explain the change in withholding?:- The 2009 tax cut that impacted the vast majority of salaried workers.

- A shift down the payscale by workers;

- Changes in with holding rules as part of the Stimulus package;

- Start up business founders working for little or no pay;

- Hours worked continues to get cut

Data through March 2010, released today by Standard & Poor's for its S&P/Case-Shiller Home Price Indices, the leading measure of U.S. home prices, show that the U.S. National Home Price Index fell 3.2% in the first quarter of 2010, but remains above its year-earlier level. In March, 13 of the 20 MSAs covered by S&P/Case-Shiller Home Price Indices and both monthly composites were down although the two composites and 10 MSAs showed year-over-year gains. Housing prices rebounded from crisis lows, but recently have seen renewed weakness as tax incentives are ending and foreclosures are climbing.

Consumers gained more confidence in May than projected as a recovering U.S. economy raised expectations hiring will pick up in coming months.The Conference Board’s confidence index rose to 63.3, exceeding all estimates of economists surveyed by Bloomberg News and the highest level in two years, according to a report from the New York-based private research group. Other figures showed home prices rose less than projected in the year through March.

Employment gains in five of the past six months may be helping overcome the damage from slumping stock prices as investors fret the European debt crisis will slow global growth. Meantime, the looming end of a government homebuyer tax credit signals property values may stagnate for the rest of the year as foreclosures mount.

“I’m relatively optimistic that we’ll get through the European debt crisis without dire economic consequences, but the jury is still out on that one,” said Stephen Stanley, chief economist at Pierpont Securities LLC in Stamford, Connecticut. Home prices “are going to drag along the bottom for a while until we get a better handle on the overhang” of inventories.

The three-month U.S. dollar London interbank offered rate, or Libor, was fixed at 0.5363% Tuesday, up from 0.5097% on Monday. The rate is the highest since early July of last year and has been on the rise since the spring on growing worries over sovereign debt problems in the euro zone. The spread between Libor and overnight index swaps have also widened, a move that's viewed as a sign of banks growing more reluctant to lend to each other

The Obama administration made a strong plea to Congress on Monday to grit its teeth and pass a new set of spending measures – dubbed the “second stimulus” by some economists – in order to help dig the economy “out of a deep valley”.The call for action, which was made by Lawrence Summers, Barack Obama’s senior economic adviser, who urged Congress to pass up to $200bn (£138.9bn) in spending measures, came at the same time as Mr Obama asked Capitol Hill to grant him powers to cut “unnecessary spending”.

The combined announcements were made amid rising concern that centrist Democrats, or those representing marginal districts, might vote against the spending measures, which include more loans for small businesses, an extension of unemployment insurance and aid to states to prevent hundreds of thousands more teachers from being laid off.

The move comes at a time when last year’s $787bn stimulus is wearing off. Mr Summers argued that it would be a premature move at this stage in the cycle to move to fiscal discipline. “I cannot agree with those who suggest that it somehow threatens the future to provide truly temporary, high-bang-for-the-buck jobs and growth measures,” he said. “Spurring growth, if we can achieve it, is by far the best way to improve our fiscal position.”

Let's hope Congress can do the right thing and pass this with a heavy emphasis on infra-structure spending.

In a setback for the May payroll outlook, initial jobless claims jumped 25,000 in the May 15 week to 471,000. The disappointment includes a 2,000 upward revision to the prior week. There are no special factors to explain the latest week's jump. The 471,000 level is the highest in five weeks, the second highest since February, and 12,000 higher vs. mid-April. But in an important offset, the four-week average of 453,500 does show improvement from mid-April's 461,000.

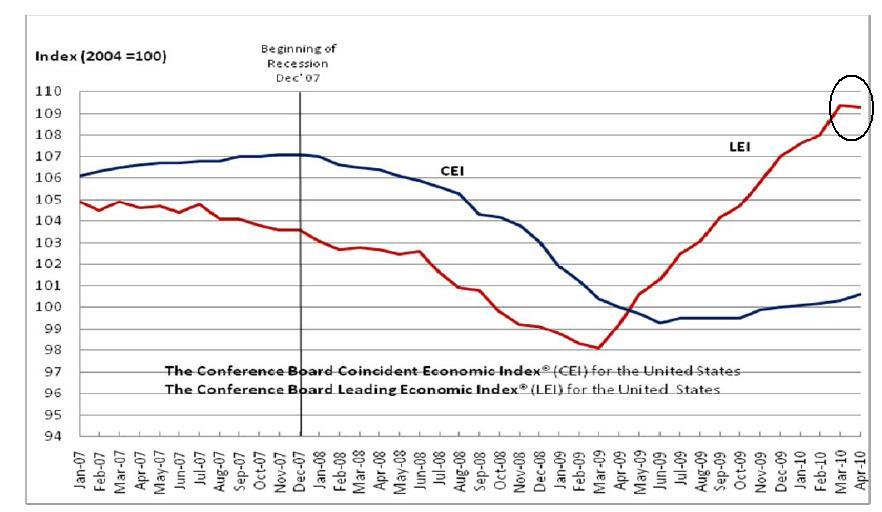

The Conference Board Leading Economic Index®(LEI) for the U.S. declined 0.1 percent in April, following a 1.3 percent gain in March, and a 0.4 percent rise in February.

Says Ken Goldstein, economist at The Conference Board: "These latest results suggest a recovery that will continue through the summer, although it could lose a little steam. The U.S. LEI declined slightly for the first time in more than a year, and its six-month growth rate has moderated since December. Meanwhile, the coincident index, a measure of current economic activity, has been improving since mid-2009."

{kind=link}

{kind=link}