Saturday, April 11, 2015

Weekly Indicators for April 6 - 10 at XE.com

- by New Deal democrat

My Weekly Indicator post is up at XE.com.

That part of the US economy most intertwined with the global economy appears to be in recession. That part which is primarily domestic is almost universally positive.

Friday, April 10, 2015

Caterpillar Is A Buy At These Levels

This is not a solicitation to buy or sell this security. Do your own research and come to your own conclusions. I own this.

According to

Finviz.com, there are 14 companies in the farm and construction machinery

sector. With a $49 billion market cap,

Caterpillar is the largest. John Deere

is a distant second with a total valuation of ~$29 billion. Attesting to Cat's dominant position, the third and fourth largest companies are

much smaller at $11.3 and $4.1 billion, respectively. This industry faces a difficult international

environment. Not only is the strong

dollar hurting competitiveness, the commodities super cycle is slowing, which

lowers demand. Domestically, durable

goods orders have slowly decreased since mid-summer. This challenging environment is a primary

reason why most companies in this sector are trading at attractive levels.

Here is the

weekly chart, going back three years

The stock has fallen about 30%, moving from the 109 level in

mid-2014 to its current level in the lower 80s.

There is strong technical support at these levels from several years

ago. The chart may have formed a double

bottom in 1Q14. Finally, the low reading

of the MACD implies a move higher is possible.

Here is a table from

Morningstar of the relevant valuation metrics:

On a PE basis, the company is slightly overvalued relative to

the industry. Supporting this is the

slightly better than average return on assets and equity. However, the company’s growth is less than

the industry average. Although the company

is pretty fairly valued, its dominant industry position warrants a better than

average PE.

Caterpillar’s balance

sheet shows the company is financially well managed. Receivables decreased from 26% of assets in

2010 to 19% in 2014. Although the

receivables turnover ratio has increased from 2.77 in 2010 to 3.25 in 2014, the

size of the increase is statistically meaningless. Inventory increased from 14%/assets in 2010

to 17% in 2012, but returned to 14% over last two years. Since 2010, inventory turnover has slightly increased,

moving from 95.84 to 113.95. However,

these increases in inventory are very small and don’t detract from the

company’s overall attractiveness. The

current ratio is 1.39, indicating the company has ample liquidity. Finally, long term debt is a conservative 32%

of liabilities. With well-managed

receivables and inventory accounts along with a conservative debt structure, Caterpillar’s

balance sheet should appeal to any conservative investor.

The company’s

income statement, however, could be better.

The biggest problem is the two year drop in top line revenue, from $65.9

billion in 2012 to $55.1 billion in 2014.

While the COGS percentage has been stable for the last five years, there

has been a 2% increase in SGA expenses, leading to a 2% drop in the net margin

over the same period. The dividend payout

ratio of 44% firmly supports current dividend levels. Perhaps most importantly, the interest coverage

ratio stands at 12.79, indicating the company’s debt load is anything but a

problem.

And finally, we

turn to the cash slow statement, which dividend investors should cheer. The company has been cash flow positive for

the last five years. With the exception

of 2012, the dividend was funded entirely from operations. The company has the option of ending a stock buyback

program (which totaled $4.2 billion in 2012) to protect future dividend

payments if necessary. And with operations

investments steady between $1.7 and $1.9 billion for the last three years, there

is little reason to think any major change in dividend policy is on the

horizon.

Given the low

interest rate environment, Cat’s 3.35% dividend yield is very attractive. Their financial condition is solid, meaning

there is little reason to see a cut in the near future. The current price level, which is near the

lowest of the last three years, is attractive from a long-term investment

perspective. Adding all these factors

up, Cat is a buy at these levels.

This is the graph that scares me still

- by New Deal democrat

Three years ago I ran a post entitled, "This is the graph that scares me," featuring the graph of median wage growth, which I've updated below:

Below is an abbreviated version of what I wrote then:

----------------------

[Median wage growth] has been running at under 2% at all times since the financial collapse of 2008.

So, even if inflation runs at the very modest rate of only 2% ..., more than half of all workers fail to keep up.

You simply cannot have a durable economic expansion where most workers are consistently falling behind.

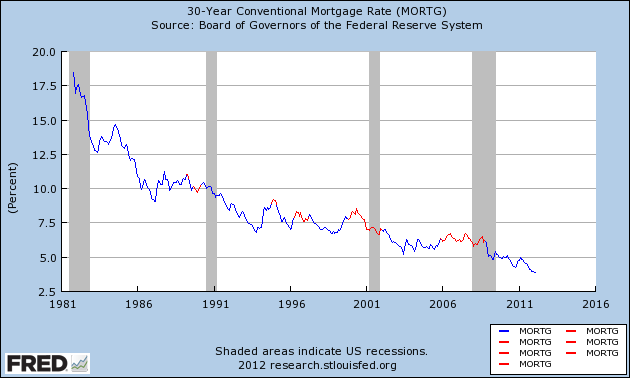

Lower mortgage rates in the last several years has enabled a huge number of consumers to refinance ... [and therefore] the average household has a lower carrying cost of debt, compared with their income, than at any point in the last 30 years.

In the past 30 years,as shown in this graph of mortgage rates, which highlights those periods where interest rates are higher than they were 3 years prior in red, once households have been able to refinance, it took at least 3 years without new lows being established, before the economy fell back into recession.

[in 2012 I continued:]

We just set new lows.

It's difficult to imagine any further round of refinancing once this one is done. Can rates really go much lower?

If median wage growth doesn't improve soon, there will be no escaping another recession once the effect of refinancing has run its course ....

[In the Great Recession], we managed to escape without actual wage deflation (although laid off workers may not have been able to find work at the same salary they were making previously). I doubt we will be so lucky a second time ....

--------------------------

One year ago I updated this post, saying the graph still scared me, and pointing out that YoY growth in median wages was still paltry.

So where are we now?

Here is mortgage refinancing through last week, courtesy of Bill McBride a/k/a Calculated Risk:

Refinancing all but died in mid-2013, and except for a mini-spike at the beginning of this year, has remained asleep ever since.

Refinancing had helped households lower their debt ratios to 30+ year lows:

That deleveraging has all but stopped.

Here is an update of the graph of mortgage rates, focused on the last 5 years:

Mortgage rates bottomed in December 2012. Eight months from now will mark 3 years since that time.

The good news is, the big decline in gas prices has meant that real median wages have increased to new highs, and most recently nominal median wages have grown at a 2.3% rate. If gas prices remain low, and if the economic expansion continues for awhile longer, hopefully real median wages will continue to rise.

But I remain very uncomfortable with paltry nominal wage growth. And the next recession is out there somewhere. When it hits, growth in nominal wages will decline.

We entered the Great Recession with wage growth as high as 3.5%, and ended it with 1.5% nominal wage growth. A similar decline from the current 2.3% nominal wage growth would tip us into outright wage decreases, with all of the horrors of debt-deflation that implies. This is still what scares me.

Thursday, April 9, 2015

What's the culprit behind recent retail sales and jobs weakness?

- by New Deal democrat

What is behind the recent slowdown in so much economic data? Candidates include the weak global economy and the related strong dollar, the West Coast ports strike, and unusually poor winter weather, among others. The issue is important because, while winter has given way to spring, and the ports dispute has been settled, the Oil patch weakness is continuing and may even intensify.

Breaking the reports down on a state by state basis helps us determine which of the potential issues was the primary driver of the data. To cut to the chase, it looks like Oil patch weakness is the prime ingredient in the punk March jobs report, although weather may have played a supporting role. By contrast, weather appears to have been the primary culprit in hiring in February, and poor retail sales in January. We will get further information on these later this month, with state-by-state breakdowns in the unemployment rate, and state revenue reports for March, which will reflect actual retail sales in February.

Ironman at Political Calculations offers supporting data that the March employment report reflected a particularly bad month in the Oil patch. As I pointed out the other day, there was a big increase to over 300,000 during the weeks ending February 7, 21, and 28. He shows us this graph of how much of that increase can be traced to the 9 states most impacted by fracking:

Note that the big increase starts in February, increasing to 15,000 per week. This showed up in the March employment report, which of course nets hires and fires.

Meanwhile, on Tuesday we got the JOLTS data for February. Here is Doug Short's graph of the monthly numbers and 6 month moving averages for openings, hires, and discharges:

Note that, through February, there has been virtually no upward movement in discharges. what has changed is that, while job openings are growing at an increased pace since early 2014, the growth in actual hires, which had accelerated even more than openings, has decelerated in the last few months.

This suggests that, through February, the Oil patch and the West Coast ports strike, which would have increased discharges, were not significant. That conclusion is buttressed when we look at the breakdown of openings and hires broken out by job sector:

Note that openings in February increased vs. January in virtually all job sectors. Meanwhile, hires for those openings decreased in virtually all job sectors, although the biggest percentage decrease was in construction (which is where we would expect the Oil patch weakness to be most felt. In other words, while Oil patch weakness played a role, the primary driver of hiring softness in February was probably the weather, since almost all job types were affected.

Finally, there is the anomalous decline in retail sales, which has happened in the face of a big increase in real personal income due to savings on gas purchases. Thus it is hard to assign this to importing global weakness or concentrated declines in the Oil patch.

And looking at reports of state tax revenues appears to confirm that weather is the big culprit behind the recent weakness in retail sales. Below is a chart of reports through February of sales tax revenues (recall the businesses typically pay sales tax receipts in the month after the goods or services are sold, so the February reports are primarily January sales):

| State | Dec | Jan | Feb | ||

|---|---|---|---|---|---|

| CA | +3.8 | -12.4 | +34.8 | ||

| TX | 4.3 | +11.2 | +11.7 | ||

| NY | +3.1 | +4.2 | -0.3 | ||

| MA | +0.9 | +0.5 | +0.2 | ||

| NJ | -1.6 | +2.9 | +2.6 | ||

| VA | -1.0 | +11.2 | +4.2 | ||

| GA | +5.2 | +8.2 | +5.7 |

If the West Coast ports strike was the big culprit, California should be faring the worst. Instead in February it reported a large YoY increase.

If the Oil patch were the primary driver, Texas should be faring poorly. Instead Texas also reported large YoY gains in February.

But look at the northeast, especially New York. Alone among all states, New York reported an actual YoY decline in February. New Jersey and Massachusetts also saw declines in positive comparisons between January and February, and even Virginia saw a similar decline. Georgia was unaffected.

The slew of winter snowstorms that broke Boston's record of annual snowfall started at the end of January. New York City, for the first time in over 100 years, shut down its subway system due to a (blown) blizzard forecast, which even at the time was estimated to cost in excess of $750 Million in revenue.

The Fed's Beige Book also points to weather as the main culprit in February. Here are a sample of the observations:

New York District: [some] contacts say that early 2015 sales continued the positive trajectory in place by the end of 2014, but business dropped off noticeably in late January, when the first of four (to date) significant winter storms hit. One retailer reports that over the last month, about 200 of their stores based in New England had been closed for a few days because of the severe weather

Retail sales have improved somewhat, on balance, since the last report. A major general merchandise chain indicates that sales were up strongly from a year ago and also above plan in January but slowed a bit and were on plan in the first half of February. Similarly, a major retail contact in upstate New York describes January as a solid month and February as fairly strong. In both cases, harsh winter weather was said to have hindered business somewhat. In general, retailers report that inventories are in good shape and that discounting remains prevalent.

Philadelphia: A Pennsylvania contact described sales levels throughout the state as being strong overall through mid-February despite the typically softer seasonal levels. New Jersey contacts reported strong statewide sales for January; however, weather was taking a toll on early February sales. Auto dealers expect growth to continue in 2015 as it had in 2014.

Richmond: Retail activity slowed in the weeks since our previous report. Sales of cars and light trucks were generally flat, according to dealers in Virginia, North Carolina, and South Carolina. A dealer in the eastern panhandle of West Virginia reported slightly slower sales. Grocery and convenience stores reported a decline in food sales in in the past month. According to the manager at a Virginia chain of discount stores, holiday and post-holiday sales were softer than expected, but still higher than a year ago.

Kansas City: Consumer spending activity was flat in January and early February, but remained higher than a year ago with solid expectations for the coming months. Retail sales declined from the previous survey but were around year-ago levels. Several retailers noted a drop in sales of luxury products, although sales of winter and lower-priced items were steady.

Dallas: Retail sales rose during the reporting period, but the pace of growth was mixed. Demand continued to be up year over year, and a few retailers noted slight improvement in foot traffic since the last report. Two national retailers said Texas' sales performance was in line with the nation overall, while a third national retailer noted Texas was outperforming the national average. Outlooks were positive, and contacts expect modest sales growth over the next three months.

San Francisco: Overall retail sales activity grew moderately during the reporting period.... Merchants in some areas showed very strong holiday sales and would have seen even larger volumes if not for delays receiving merchandise caused by labor disputes at West Coast ports. In other regions, holiday sales were not quite as strong as expected, and, as a result, retailers in those areas still have a little excess inventory.

The beige book shows that, with the exception of Kansas City, all of the slowing was in the Northeast and Mid-Atlantic. Meanwhile, Texas was strong, and the only impact of the West Coast ports strike in California was a decline in inventory, not sales.

To summarize:

- retail sales through January into February appear to have suffered primarily due to the unusually poor winter weather.

- hiring in February was also primarily affected by the weather, although Oil patch weakness played a contributing role.

- jobs in March so far look like they were primarily affected by Oil patch weakness.

I will update this once we get further information by the end of this month.

Wednesday, April 8, 2015

Corporate profits vs. stock prices: an update

- by New Deal democrat

I have a new post up at XE.com. Since corporate profits are a long leading economic indicator, and the stock market is a short leading indicator, it makes sense that, contrary to common investor wisdom, stock prices follow rather than lead corporate profits.

So what does that mean now?

Tuesday, April 7, 2015

Monday, April 6, 2015

The punk March jobs report looks primarily like an Oil patch story

- by New Deal democrat

At first blush, the relatively poor March jobs report looks like an Oil patch story, not a weather story or a West coast port strike story.

Changes in initial jobless claims during a month have a pretty good correlation with the same/next month's jobs report (since the reference week is the one including the 13th of each month). Here's the relevant scattergraph and regression line for this expansion:

We had 3 bad weeks in February of new jobless claims over 300,000 a month. To find out if the weather was a big factor, or if the primary weakness was the Oil patch, I compared TX and OK with NY and Mass, going back to the first of the year. This can be done using the Department of Labor's state-by-state breakdown of initial jobless claims, which is reported with a one week delay.

The result was that NY and Mass. had lower claims on average in 2015 in the reference weeks compared with the same week in 2014. TX and OK, by contrast, had about 15% more initial claims in those weeks during 2015 vs. 2014 during the reference weeks for the March report.

Oklahoma's jobless claims increased YoY starting at the end of November. Texas turned negative YoY in late January.

Massachusetts had one week wherein 2015 claims equalled 2014 claims. All other weeks were lower. New York had two weeks in 2015 slightly higher than 2014, but the other two weeks were significantly lower than 2014.

Massachusetts had one week wherein 2015 claims equalled 2014 claims. All other weeks were lower. New York had two weeks in 2015 slightly higher than 2014, but the other two weeks were significantly lower than 2014.

While the since-resolved West coast ports strike could have nationwide impacts, one state where it would surely have an impact is California. California did have one negative YoY week of jobless claims, all the way back in early January. It also had comparatively small decreases in jobless claims in 2015 vs. 2014 during the weeks ending January 31 and February 7. During the 4 reference weeks for the March jobs report, however, it went back to strongly positive YoY readings (i.e., steep declines in jobless claims in 2015 vs. 2014).

Tomorrow's JOLTS report will be for February, so it will give us little insight into March. State-by-state unemployment rate changes won't get reported until the end of this month. For now, what we can say is that the relatively poor March jobs report looks primarily like an Oil patch story and only secondarily a weather story, and not a West coast ports strike story.

Subscribe to:

Posts (Atom)