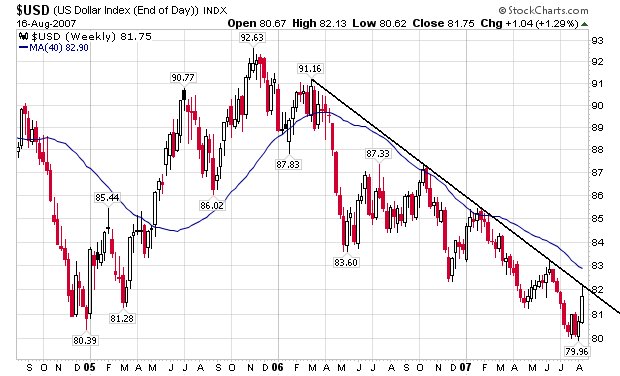

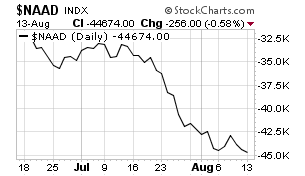

That being said, let's begin. Let's start with the last chart from yesterday's post of the SPYs -- a 3-month chart. The same observations apply. All of the moving averages are moving lower. The short-term SMA are below the longer term SMAs which will exert downward pressure for now. The trend since the last week of July has been down. Most importantly, the average is flirting around the 200 day SMA, which is usually the line that separates bull and bear markets.

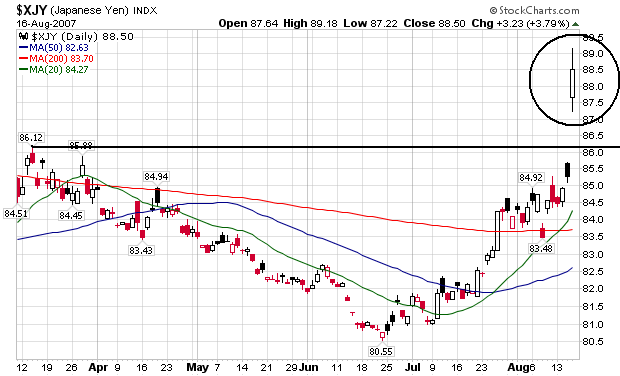

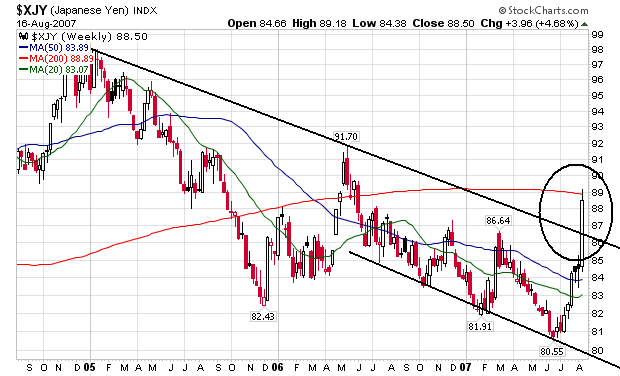

Here's the two year, weekly chart. Notice the SPYs have rallied since early July 2006. They have since broken their trendline on heavy volume.

Here are three weekly charts, which all have Fibonacci fans. Notice that:

On the one year chart, we are below the first line of support, which is now acting as upside resistance.

On the two year chart we have downside room of about 2 to 2.5 points before we get to support.

On the three year chart we have about 6-7 points before we get to support.

The 1-year daily MACD is very oversold:

But on the weekly 3-year MACD we have both upside and downside room.

So -- what does all of this mean?

1.) Most short-term indicators are very negative -- downward sloping SMAs, shorter SMAs below longer SMAs and the average is moving through the 200 day SMA at a downward trajectory.

2.) Longer-term indicators also weigh bearish. We're below the 1-year Fibonacci resistance with downside room on the 2 and 3 year charts. We've also broken a two year trend line to the downside. While the short-term MACD is oversold, it seems the market is rally reacting to the longer-term bull run right now and correction three years of upside moves.

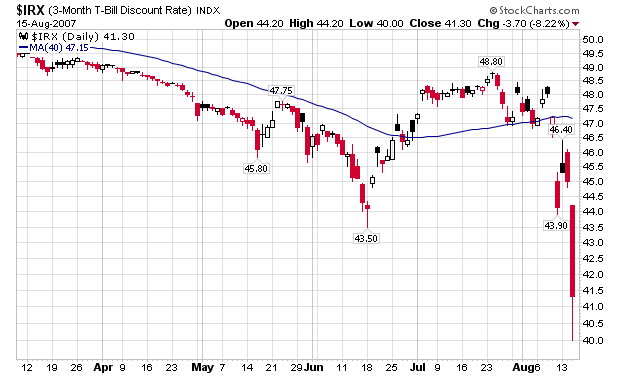

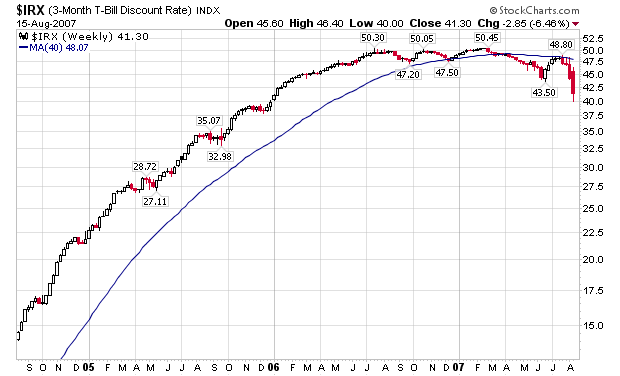

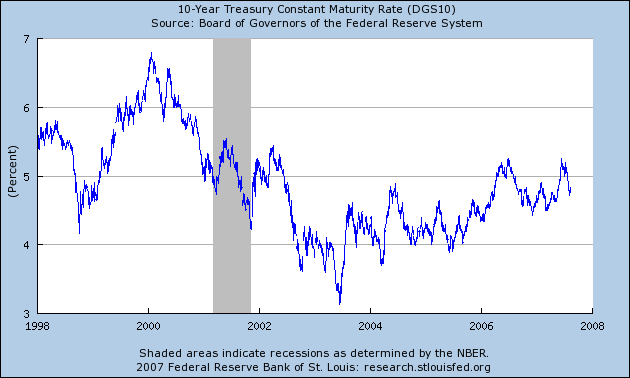

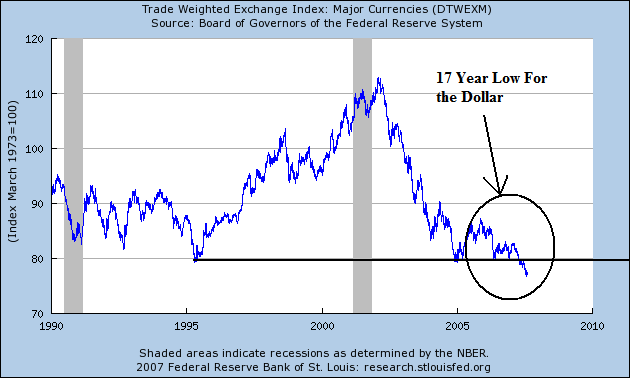

3.) The one wild card is the Fed. Here is the best summation I have found:

Federal-funds contracts traded on CME Group suggest market participants see the Fed cutting rates by a half-percentage point at the September 18 meeting. But don’t put that in the bank just yet. Though the actions taken by the Fed were meant to bolster confidence in the financial system — and the Fed encouraged banks to use the discount window, which normally carries a bit of stigma – some believe the move today is a way for the monetary committee to buy itself more time, and perhaps even lessens the possibility of a rate cut in September. “We believe the action reduces the overriding worry that the mortgage market would grind to a halt,” says Standard & Poor’s chief economist David Wyss. “It also buys the Fed time to assess the situation and possibly not act on the Fed funds rate until September.”