- by New Deal democrat

The week's headline numbers were the 216,000 jobs added in March and the continued decline in the unemployment rate to 8.8%. As usual, I'll have more to say in the coming week, including at least one finding that contradicts the conventional wisdom. For now, we can just note that it was a good number - just not good enough for all the ground we have to make up. Other monthly numbers continued to show an economy that is slowing due to the choke collar of high Oil prices. The manufacturing workweek declined (-.1), as did new factory orders. There are two more of the 10 leading indicators that have turned down. Residential and non-residential spending also declined. New cars sold in March also declined slightly from February, although at 13.1 million vehicles, this is still the second best showing in over two years. On the plus side, manufacturing as measured by the Chicago PMI and the ISM continued on a tear. BUT the leading components of that index - new orders and vendor deliveries - declined. Vendor deliveries declined sharply - the third of the 10 leading indicators to show a decline this week.

Did I mention that Oil was like a choke collar constricting economic growth?

Turning now to the high-frequency weekly indicators:

The BLS reported that Initial jobless claims last week were 388,000. The 4 week average is 394,250. This is the sixth week in a row that this number has been initially reported below 400,000. On the other hand, this series has not made a new low in the last month. Will the downward momentum continue or has it stalled?

On the other hand, Oil was trading at about $107.94 a barrel Friday, the fourth full week it has been above $100. It remains at a level above 4% of GDP. I believe we have started to see the economic damage from that shock. Gas at the pump increased to $3.60 a gallon. Gasoline usage at 8866 M gallons was 2% lower than last year. As I expected, this YoY comparison is deteriorating and has now turned negative.

Railfax was up 3.5% YoY. Baseline traffic for the second week is no higher than last year's levels, and both cyclical and intermodal traffic are only slightly higher. Waste materials continued below last year's levels (this may be fallout from municipal funding cuts for recycling). Shipments of motor vehicles remained the bright spot, continuing to improve YoY. With the exception of motor vehicles, rail freight is now also signalling a significant slowdown (but not an outright reversal).

The Mortgage Bankers' Association reported a decrease of 1.7% in seasonally adjusted mortgage applications last week. This series has meandered generally in a flat range since last June. Refinancing decreased 10.1%, and remains near its lows since last July. The silver lining is that neither series has hit a new low in almost 9 months.

The American Staffing Association Index remained at 91 for yet another week. This series has stalled at the 90-91 level for 7 weeks. It is signalling stagnation, not growth, and is stalled relative to its pre-recession peak.

The ICSC reported that same store sales for the week of March 26 rose 2.6% YoY, and increased 0.2% week over week. Shoppertrak reported a 4.3% YoY gain for the week ending March 19, and a WoW gain of 0.5%. Unlike almost every other series, these two series' YoY comparisons have been remaining steady or improving over the last month.

Weekly BAA commercial bond rates increased.02% to 6.00%. This compares with a 09% increase in the yields of 10 year treasuries to 3.38%. Both series are down from recent highs.

Adjusting +1.07% due to the recent tax compromise, the Daily Treasury Statement showed that for all of March 2011, $163.8 B was collected vs. $164.9 B a year ago, for a loss of -1.1 B YoY. This is the first month with an outright YoY decline compared with last year. For the last 20 days, $136.6 B was collected vs. $128,4 B a year ago, for a gain of $8.2B, or +6.4%. I suggest using this series with extra caution, because the adjustment for the withholding tax compromise is only a best guess, and may be significantly incorrect.

M1 was up 1.3% w/w, down -0.4% M/M, and up a strong 9.9% YoY, so Real M1 is up 7.7%. M2 was unchanged w/w, up 0.2% M/M and up 4.3% YoY, so Real M2 is up 2.1%. Although Real M1 is still strongly in the "green zone" where it has been since before the end of the "great recession," Real M2 has been fading back into the "yellow zone" below 2.5%. Additionally, the weak +0.2% M/M reading means that, depending on inflation, it could become yet another of the 10 components of the LEI to go negative in March.

Last week I noted that the LEI may have a negative month in March. Consumer confidence, durable goods, and (Feb.) housing permits were all down strongly. This week ISM vendor supplies, the manufacturing workweek, and new factory orders also turned down. As noted just above, M2 could also be a negative. Only the bond spread yield, the stock market, and initial unemployment claims look like positives. In sum, that's 6 components down, 1 neutral (possibly negative), and only 3 positive. (OTOH, ECRI's growth indicator continues to be positive).

Did I mention that OIl was like a choke collar constricting economic growth?

Saturday, April 2, 2011

Friday, April 1, 2011

Is Inflation Really An Issue?

Consider the following charts.

The above chart is the year over year percentage change in core inflation. It is currently showing one of the lowest readings of the last 40 years.

Above is a chart of total inflation on a YOY basis. Notice that the YOY percentage change is also at very low historical levels.

As I've noted before, the data indicates that manufacturing has the ability to absorb high crude prices, thereby preventing raw material increases from being passed on to consumers.

In short, the data does not support the idea that inflation is anywhere near out of control right now.

The above chart is the year over year percentage change in core inflation. It is currently showing one of the lowest readings of the last 40 years.

Above is a chart of total inflation on a YOY basis. Notice that the YOY percentage change is also at very low historical levels.

As I've noted before, the data indicates that manufacturing has the ability to absorb high crude prices, thereby preventing raw material increases from being passed on to consumers.

In short, the data does not support the idea that inflation is anywhere near out of control right now.

BLS + 216,000; Unemployment at 8.8%

From the BLS:

=============

NDD here with a few additional comments:

Two months ago, when we got the “disappointing” January report, noting the relentless upward revisions to the BLS’s initial payroll reports for the last year, I said that

Two months later, the final revision puts January’s report at +68,000.

I have also been pointing out that, averaging by quarter, it is obvious that the jobs picture has been continually improving. Here is how that trend stands with the first quarter of 2011 behind us:

As I said a month ago, the jobs recovery is proving to be a long, slow, hard slog, but we are still improving.

Government layoffs continue to be the one big black eye. Over the last 3 months, 86,000 government jobs have been lost.

Finally, a month ago I noted that something is going on with the Latino population - possibly including substantial repatriation back to the home countries of many immigrants - noting that the unemployment rate for this group is dropping like a stone (from 13.2% in November to 11.6% in February), but almost entirely due to dropping out of the labor force. On a preliminary reading, that trend continued in March, with Latino unemployment dropping to 11.3%.

I share Bonddad’s overall assessment – this was a good report.

Nonfarm payroll employment increased by 216,000 in March, and the unemployment rate was little changed at 8.8 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in professional and business services, health care, leisure and hospitality, and mining. Employment in manufacturing continued to trend up.From Bloomberg:

The U.S. economy added more jobs than forecast in March and the unemployment rate unexpectedly declined to a two-year low of 8.8 percent, a sign the labor- market recovery is gathering speed.Payrolls increased by 216,000 workers last month after a revised 194,000 gain the prior month, the Labor Department said today in Washington. Economists projected a March gain of 190,000, according to the median estimate in a Bloomberg News survey. The jobless rate dropped from 8.9 percent in February, the fourth straight decrease.

Record exports and gains in business and consumer spending are prompting companies like Chrysler Group LLC and Kohl’s Corp. (KSS) to boost staff, helping the U.S. weather the highest energy prices in more than two years. The improving economy encouraged Federal Reserve policy makers last month to signal they were unlikely to extend bond purchases beyond June.

“This is consistent with a labor market recovery that is broadening,” Robert Dye, a senior economist at PNC Financial Services Group Inc. in Pittsburgh, said before the report. “We’re starting to see more and more small businesses participating in hiring. That’s providing the foundation of a self-sustaining recovery.”

Payroll estimates in the Bloomberg survey of 83 economists ranged from gains of 150,000 to 295,000. February was revised up from a previously reported gain of 192,000, while January payrolls increased 68,000 after a prior estimate of 63,000. The unemployment rate was projected to hold at 8.9 percent, according to the survey median.

While companies stepped up hiring, earnings and hours stagnated.

I want to highlight some points not made in the articles.

In the last year, the civilian labor force ("The labor force includes all persons classified as employed or unemployed in accordance with the definitions contained in this glossary.") has decreased by 489,000. Over the same period, the civilian non-institutional population has increase by 1.8 million. This is very important from a mathematical perspective as it indicates people are leaving the labor force, or are "not in the labor force." This DOES NOT MEAN THEY HAVE GIVEN UP LOOKING FOR WORK. They could be back in school or retired (considering the baby boomers are now retiring at a pace of 10,000 day this is a very interesting number). What I find interesting about the statistic is the numerator has decreased, indicating the total number of people employed and unemployed over the last year has decreased.

According to the household survey, total employment has increase by 912,000 over the last year or a pace of 76,000/month. Over the same period, the establishment survey has increased by 1.3 million or 108,000 month. Neither of these paces is particularly inspiring. However, remember at the end of last Spring the economy experienced a slowdown caused by the BP oil spill and the EU situation.

Over the last year (March 2010 to March 2011), average weekly earnings have increased 2.33% (increasing from $766.57 to $784.44). This has occurred because of an increase in wages (from $22.48 to $22.87) and an increase in hours worked (from 34.1 to 34.3).

Consider these two charts from the report (click for a larger image):

The employment situation is clearly improving.

=============

NDD here with a few additional comments:

Two months ago, when we got the “disappointing” January report, noting the relentless upward revisions to the BLS’s initial payroll reports for the last year, I said that

There is thus every reason to believe that January's "disappointing" +36,000 job report will be less disappointing in two months' time

Two months later, the final revision puts January’s report at +68,000.

I have also been pointing out that, averaging by quarter, it is obvious that the jobs picture has been continually improving. Here is how that trend stands with the first quarter of 2011 behind us:

| Quarter | Average Job gain/loss |

|---|---|

| 4Q 2009 | -135 |

| 1Q 2010 | +15 |

| 2Q 2010 | +97 |

| 3Q 2010 | +60 |

| 4Q 2010 | +139 |

| 1Q 2011 | +159(p) |

As I said a month ago, the jobs recovery is proving to be a long, slow, hard slog, but we are still improving.

Government layoffs continue to be the one big black eye. Over the last 3 months, 86,000 government jobs have been lost.

Finally, a month ago I noted that something is going on with the Latino population - possibly including substantial repatriation back to the home countries of many immigrants - noting that the unemployment rate for this group is dropping like a stone (from 13.2% in November to 11.6% in February), but almost entirely due to dropping out of the labor force. On a preliminary reading, that trend continued in March, with Latino unemployment dropping to 11.3%.

I share Bonddad’s overall assessment – this was a good report.

Thursday, March 31, 2011

Is It About the Productivity -- Or is There Something More?

From the AP:

Yet the exact opposite has happened. The pace of job creation has been at best lackluster; it's almost as though the US has cut off 10% of its workforce. Those still employed are OK, but those who are not are essentially locked out from getting back in. I think the article -- which notes that productivity gains in the US have been very large -- explains a very important fundamental reason: if you can do more with less, why hire more?

Consider the following chart, which shows five years of productivity gains in the US:

Notice the very large increase starting in 2009 -- increases which clearly outpaced the gains from 2006-2009. Despite the mass firings, the US became far more productive. In the above environment, businesses aren't in a position where they have to hire.

Let me add another wrinkle to this idea that I have not worked out in any detail. Consider this chart of the labor force participation rate:

The participation rate measures "[t]he labor force as a percent of the civilian noninstitutional population." The chart above shows that number has been decreasing as the baby boomers start to retire. The boomer retirement has been a back story for some time; however, it's effect on employment decisions has not been measured that I know of. Now -- hypothetically -- let's assume that starting in roughly 2000 (or maybe earlier) those who were responsible for hiring decisions started to think to themselves, "with the upcoming baby boomer retirement coming, we need to be prepared for fewer job applicants. So, we need to be ready to make do with less." If that was the underlying premise of human resources for the last 15+ years, the lack luster, post recession employment situation would make more sense. In effect, US business was acknowledging the decreasing number of individuals available for work caused by the upcoming baby boomer retirement wave by increasing productivity and hiring fewer workers.

The United States is out of step with the rest of the world's richest industrialized nations: Its economy is growing faster than theirs but creating far fewer jobs.This is something I've been mulling over for some time -- with no clear idea on the answer. During the worst part of the recession, companies were laying off over 600,000 people/month. Eventually, the economy lost more or less all the jobs created during the previous expansion. A rate of attrition that large would lead to the conclusion that companies cut too many employees and would need to hire them back quickly (at least, that's the intuitive logic).

The reason is U.S. workers have become so productive that it's harder for anyone without a job to get one.

Companies are producing and profiting more than when the recession began, despite fewer workers. They're hiring again, but not fast enough to replace most of the 7.5 million jobs lost since the recession began.

Measured in growth, the American economy has outperformed those of Britain, France, Germany, Italy and Japan — every Group of 7 developed nation except Canada, according to The Associated Press' new Global Economy Tracker, a quarterly analysis of 22 countries representing more than 80 percent of global output.

Yet the U.S. job market remains the group's weakest. U.S. employment bottomed and started growing again a year ago, but there are still 5.4 percent fewer American jobs than in December 2007. That's a much sharper drop than in any other G-7 country. The U.S. had the G-7's highest unemployment rate as of December.

Canada and Germany have actually added jobs since the recession ended in June 2009.

U.S. companies aren't acting the way economists had expected them to.

In the past, when the U.S. economy fell into recession, companies typically cut jobs but often kept more than they needed. Some might have felt protective of their staffs. Or they didn't want to risk losing skilled employees they'd need once business rebounded.

Among manufacturers, for example, some tended to hoard workers during downturns by giving them make-work assignments — sweeping factory floors, counting inventory, painting warehouses.

The result is that productivity — output per workers — has typically decelerated or even dropped as the economy has weakened.

Japan and Europe have been following that script. At the depth of the recession in 2009, productivity shrank 3.7 percent in Japan and 2.2 percent in Europe.

The United States has proved the exception. U.S. productivity growth doubled from 2008 to 2009, then doubled again in 2010, according to the Organization for Economic Cooperation and Development.

Panicked by the 2008 financial crisis and deepening recession, U.S. employers cut jobs pitilessly. They slashed an average of 780,000 jobs a month in the January-March quarter of 2009.

"My sense is there was much more weeding out of the weakest workers — the ones they didn't want," says Harvard economist Kenneth Rogoff.

Yet the exact opposite has happened. The pace of job creation has been at best lackluster; it's almost as though the US has cut off 10% of its workforce. Those still employed are OK, but those who are not are essentially locked out from getting back in. I think the article -- which notes that productivity gains in the US have been very large -- explains a very important fundamental reason: if you can do more with less, why hire more?

Consider the following chart, which shows five years of productivity gains in the US:

Notice the very large increase starting in 2009 -- increases which clearly outpaced the gains from 2006-2009. Despite the mass firings, the US became far more productive. In the above environment, businesses aren't in a position where they have to hire.

Let me add another wrinkle to this idea that I have not worked out in any detail. Consider this chart of the labor force participation rate:

The participation rate measures "[t]he labor force as a percent of the civilian noninstitutional population." The chart above shows that number has been decreasing as the baby boomers start to retire. The boomer retirement has been a back story for some time; however, it's effect on employment decisions has not been measured that I know of. Now -- hypothetically -- let's assume that starting in roughly 2000 (or maybe earlier) those who were responsible for hiring decisions started to think to themselves, "with the upcoming baby boomer retirement coming, we need to be prepared for fewer job applicants. So, we need to be ready to make do with less." If that was the underlying premise of human resources for the last 15+ years, the lack luster, post recession employment situation would make more sense. In effect, US business was acknowledging the decreasing number of individuals available for work caused by the upcoming baby boomer retirement wave by increasing productivity and hiring fewer workers.

The Housing Bust updated: Lo and behold, supply and demand works!

-by New Deal democrat

A few months ago I had the temerity to ask: Is it time to start looking for the end of the housing bust? That's because, in talking about the housing market, it is important to differentiate between housing sales and housing prices. Housing sales have been bouncing along the bottom for over two years. Housing prices, after being temporarily propped up by the housing credit in 2009 and early 2010, have resumed their downward trajectory.

Why does it matter? So long as houses are being built for people who will actually live in them (as opposed to being flipped in real estate deals), increasing new home sales in particular are an unalloyed good. More homes being built means more construction employment, and more employment in all of the sectors of the economy that have to do with furnishing, landscaping, adding to and maintaining the home.

The renewed fall in housing prices is a much more nuanced proposition. Is that good or bad? That, dear reader, depends on whether you are a buyer or a seller. The simple fact is, the more house prices fall, the more potential buyers - especially first time buyers - are able to afford them. The more affordable houses become, the more get sold, eventually working through the overhang of inventory. And the sooner the overhang of inventory is sopped up, the sooner the new home building market can start to recover. While the high rate of unemployment and underemployment means that process is taking longer and is more painful than it should be, the fact is, the process is still taking place. In fact, as we will see, in at least one hard-hit metropolitan area, the price bottom may also already be in.

First, let's look at sales. Below is a graph of housing permits (blue) and new single home sales (red)(this latter series from the NAR):

Both of these plummeted by 75% from their peak at the end of 2005 until early 2009. With a mild temporary assist from the $8000 housing credit, permits have bounced along that bottom for two full years - but the 2009 bottom has held. Single family homes have gradually declined 5% more in the last two years. February set a new low for this latter series.

But before you leap to the conclusion that yet another leg down in sales may be starting, consider the following data from each series from the last 6 months, including averages for each of the three month periods:

Housing permits:

2010-09-01 547

2010-10-01 552

2010-11-01 544 (average 547)

2010-12-01 627

2011-01-01 563

2011-02-01 534 (average 575)

New home sales:

2010-09-01 317

2010-10-01 280

2010-11-01 286 (average 294)

2010-12-01 333

2011-01-01 301

2011-02-01 250 (average 295)

Why average over the three month period? Because for now, February's poor number simply looks like payback for the sudden, big upward jump in December. As commentary at that time noted:

If March continues February's downtrend, maybe there is something more. Otherwise, the good news is, the bottom in housing sales is still in. The bad news is, there's no upward push whatsoever.

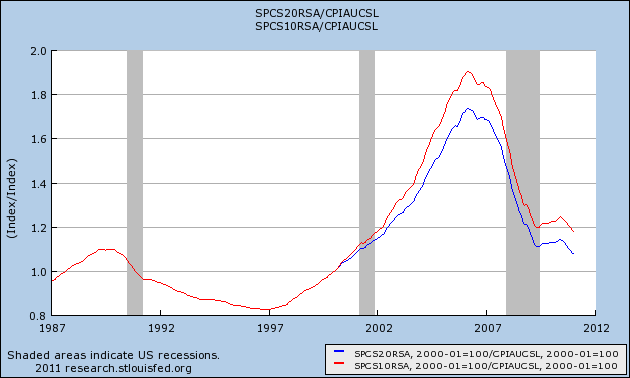

Now let's turn to housing prices. In real, inflation adjusted terms, the 10 and 20 city Case Schiller index of house prices is as low as it has been for 10 years:

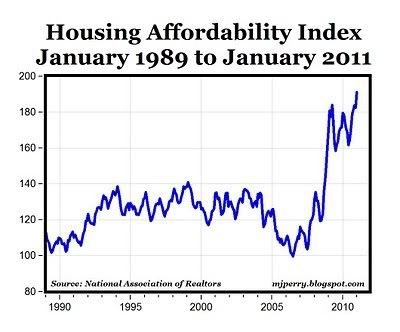

This decline in housing prices, along with the decline in mortgage rates in the last few years, has meant that typical mortgage payments are now smaller as a share of household income than they have been in several decades:

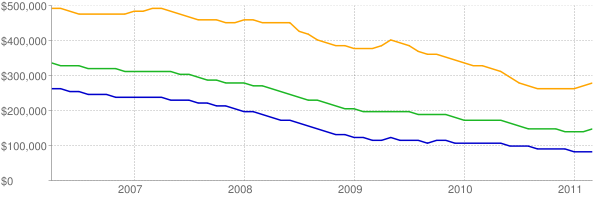

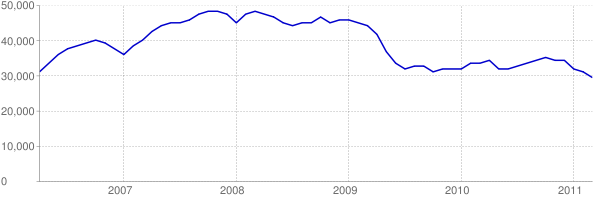

Let me focus in on a couple of hard-hit metropolitan areas that were epicenters of the bubble and then of the bust: Phoenix, AZ and Fort Myers, FL. As in the past, I will be relying on data from Housing Tracker.net - the same data that allowed me to call the top in the housing market in real time in 2006. In 2005 at the height of the bubble, the median asking price for a house in Phoenix was $380,000. As of this month it is $145,000, as shown in this graph of the 25th (blue), 50th (green), and 75th (gold)percentile asking prices of houses in the Phoenix metro area:

Anyone who bought a house in Phoenix in the last eight years who is selling it now, is probably taking a bath - the house is worth less than they paid for it. But for a first time home buyer in particular, paying $145,000 as opposed to $380,000 is a miracle. And the asking price on the type of house first time buyers would be looking at - one at about the 25th percentile, has fallen from $259,000 in early 2006 to $85,000 now -- a 2/3 decline. Indeed, house prices in Arizona generally are now more affordable compared with median income than they have been in over a decade:

As a result, in the Phoenix area in particular, the housing inventory for sale, which peaked at 48,340 in November 2007, is now back down to 29,656. This is the lowest inventory in 5 years.

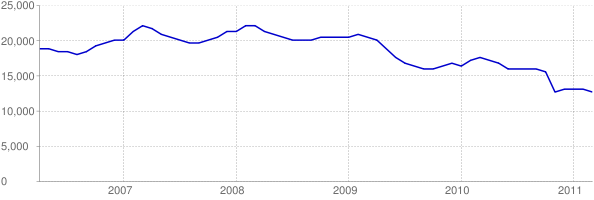

But I've saved the best for last. Let's now look at southwestern Florida (Fort Myers):

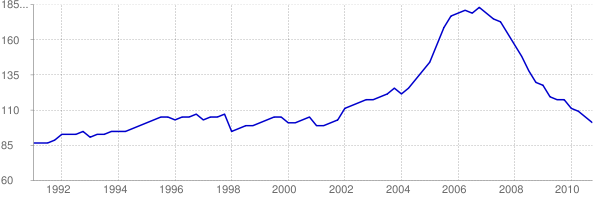

Just as in Phoenix, the number of listings has declined strongly since peaking in February 2008 at 22,335. As of March 2011 they are down to 12,646, the lowest in over 5 years:

And in this area, for the first time in five years, there is actually evidence that the bottom may already be in, as shown in this breakout of asking prices for the 25th, 50th, and 75th percentile listings:

Indeed, just yesterday Prof. Mark Perry noted that in February Las Vegas also recorded the highest number of home sales in over five years too.

As he summed up:

Indeed.

A few months ago I had the temerity to ask: Is it time to start looking for the end of the housing bust? That's because, in talking about the housing market, it is important to differentiate between housing sales and housing prices. Housing sales have been bouncing along the bottom for over two years. Housing prices, after being temporarily propped up by the housing credit in 2009 and early 2010, have resumed their downward trajectory.

Why does it matter? So long as houses are being built for people who will actually live in them (as opposed to being flipped in real estate deals), increasing new home sales in particular are an unalloyed good. More homes being built means more construction employment, and more employment in all of the sectors of the economy that have to do with furnishing, landscaping, adding to and maintaining the home.

The renewed fall in housing prices is a much more nuanced proposition. Is that good or bad? That, dear reader, depends on whether you are a buyer or a seller. The simple fact is, the more house prices fall, the more potential buyers - especially first time buyers - are able to afford them. The more affordable houses become, the more get sold, eventually working through the overhang of inventory. And the sooner the overhang of inventory is sopped up, the sooner the new home building market can start to recover. While the high rate of unemployment and underemployment means that process is taking longer and is more painful than it should be, the fact is, the process is still taking place. In fact, as we will see, in at least one hard-hit metropolitan area, the price bottom may also already be in.

First, let's look at sales. Below is a graph of housing permits (blue) and new single home sales (red)(this latter series from the NAR):

Both of these plummeted by 75% from their peak at the end of 2005 until early 2009. With a mild temporary assist from the $8000 housing credit, permits have bounced along that bottom for two full years - but the 2009 bottom has held. Single family homes have gradually declined 5% more in the last two years. February set a new low for this latter series.

But before you leap to the conclusion that yet another leg down in sales may be starting, consider the following data from each series from the last 6 months, including averages for each of the three month periods:

Housing permits:

2010-09-01 547

2010-10-01 552

2010-11-01 544 (average 547)

2010-12-01 627

2011-01-01 563

2011-02-01 534 (average 575)

New home sales:

2010-09-01 317

2010-10-01 280

2010-11-01 286 (average 294)

2010-12-01 333

2011-01-01 301

2011-02-01 250 (average 295)

Why average over the three month period? Because for now, February's poor number simply looks like payback for the sudden, big upward jump in December. As commentary at that time noted:

While building permits surprised on the upside (big time) their jump was in large part attributable to a push by builders to get approval for dwellings ahead of changes in the building codes for California, Pennsylvania and New York (these have been in force since the start of 2011).

If March continues February's downtrend, maybe there is something more. Otherwise, the good news is, the bottom in housing sales is still in. The bad news is, there's no upward push whatsoever.

Now let's turn to housing prices. In real, inflation adjusted terms, the 10 and 20 city Case Schiller index of house prices is as low as it has been for 10 years:

This decline in housing prices, along with the decline in mortgage rates in the last few years, has meant that typical mortgage payments are now smaller as a share of household income than they have been in several decades:

Let me focus in on a couple of hard-hit metropolitan areas that were epicenters of the bubble and then of the bust: Phoenix, AZ and Fort Myers, FL. As in the past, I will be relying on data from Housing Tracker.net - the same data that allowed me to call the top in the housing market in real time in 2006. In 2005 at the height of the bubble, the median asking price for a house in Phoenix was $380,000. As of this month it is $145,000, as shown in this graph of the 25th (blue), 50th (green), and 75th (gold)percentile asking prices of houses in the Phoenix metro area:

Anyone who bought a house in Phoenix in the last eight years who is selling it now, is probably taking a bath - the house is worth less than they paid for it. But for a first time home buyer in particular, paying $145,000 as opposed to $380,000 is a miracle. And the asking price on the type of house first time buyers would be looking at - one at about the 25th percentile, has fallen from $259,000 in early 2006 to $85,000 now -- a 2/3 decline. Indeed, house prices in Arizona generally are now more affordable compared with median income than they have been in over a decade:

As a result, in the Phoenix area in particular, the housing inventory for sale, which peaked at 48,340 in November 2007, is now back down to 29,656. This is the lowest inventory in 5 years.

But I've saved the best for last. Let's now look at southwestern Florida (Fort Myers):

Just as in Phoenix, the number of listings has declined strongly since peaking in February 2008 at 22,335. As of March 2011 they are down to 12,646, the lowest in over 5 years:

And in this area, for the first time in five years, there is actually evidence that the bottom may already be in, as shown in this breakout of asking prices for the 25th, 50th, and 75th percentile listings:

Indeed, just yesterday Prof. Mark Perry noted that in February Las Vegas also recorded the highest number of home sales in over five years too.

As he summed up:

Isn't this evidence that markets are working? At some point, home prices fall far enough to start bringing buyers back into the market, and sales increase.

Indeed.

Wednesday, March 30, 2011

State tax revenues for 4Q 2010 surprise to the upside

- by New Deal democrat

Calculated Risk tells us this morning that the Census Bureau reported quarterly state tax receipts for the 4th quarter of 2010 (fiscal 2Q 2011). As it turns out, they were a pleasant upside surprise compared with the preliminary Rockefeller Institute estimates.

I previously showed that only the April to June quarter (during which annual corporate and individual tax returns are most filed) shows a significant seasonal departure from the other quarters. A reasonable seasonal adjustment for this quarter to reduce it by 22.5%. Then all we have to do is adjust for inflation to create a record of "real" state revenues.

Below is an update trhough fiscal 2Q 2011 of quarterly state tax revenues. It records nominal state revenues and adjusts (in parentheses) *.775 for the April- June quarter beginning with the last fiscal year before the recession. In the second column I have further adjusted for inflation. The last quarter shows the relation of each quarter's revenues from the peak in revenue in the 4th quarter of fiscal 2008 (2nd calendar quarter of 2008) :

[apologies for the huge gap in the post - keep scrolling down. Every time I try to fix it, the html reverts to an older post]

(p)=preliminary, based on Rockefeller Institute report

When I originally posted this chart last month, I noted that "If the current trend ... continues, the Rockefeller Institute estimate of a shortfall of $60 Billion in FY 2011 compared with 2008 appears accurate."

With this revenue surprise, that estimate looks too pessimistic to me. Through the first two fiscal quarters, 2011's shortfall compared with 2008 is only $9.2B, and only $0.9B of that is from 2Q. While this quarter's GDP is likely to be only weakly positive, that is enough to believe that fiscal 3Q 2011 revenues will at least be in line with 2Q 2011 revenues. In other words, nominal FY 2011 state revenues may only have a shortfall of $10B-$20B, rather than $60B - and if we avoid another recession, nominal state revenue may have no shortfall at all compared with pre-recession revenues by the end of this summer.

While this is welcome good news, real state tax revenues will still lag pre-recession levels, and per-capita revenues still further (since to keep an even level, services must grow with population).

Calculated Risk tells us this morning that the Census Bureau reported quarterly state tax receipts for the 4th quarter of 2010 (fiscal 2Q 2011). As it turns out, they were a pleasant upside surprise compared with the preliminary Rockefeller Institute estimates.

I previously showed that only the April to June quarter (during which annual corporate and individual tax returns are most filed) shows a significant seasonal departure from the other quarters. A reasonable seasonal adjustment for this quarter to reduce it by 22.5%. Then all we have to do is adjust for inflation to create a record of "real" state revenues.

Below is an update trhough fiscal 2Q 2011 of quarterly state tax revenues. It records nominal state revenues and adjusts (in parentheses) *.775 for the April- June quarter beginning with the last fiscal year before the recession. In the second column I have further adjusted for inflation. The last quarter shows the relation of each quarter's revenues from the peak in revenue in the 4th quarter of fiscal 2008 (2nd calendar quarter of 2008) :

[apologies for the huge gap in the post - keep scrolling down. Every time I try to fix it, the html reverts to an older post]

| Fiscal Quarter | Revenues* ($ billions) | Inflation- adjusted Revenues | % off of peak |

|---|---|---|---|

| 1Q 2008 | 176.4 | 183.8 | -1.5% |

| 2Q 2008 | 178.7 | 183.6 | -1.6% |

| 3Q 2008 | 181.4 | 184.6 | -1.1% |

| 4Q 2008 | 240.8 (186.6) | 186.6 | 0 |

| 1Q 2009 | 181.2 | 179.9 | -3.6% |

| 2Q 2009 | 171.4 | 176.2 | -5.6% |

| 3Q 2009 | 159.2 | 162.7 | -12.8% |

| 4Q 2009 | 200.4(155.3) | 157.3 | -15.7% |

| 1Q 2010 | 160.5 | 161.5 | -13.5% |

| 2Q 2010 | 164.6 | 164.7 | -11.7% |

| 3Q 2010 | 163.3 | 163.0 | -12.6% |

| 4Q 2010 | 204.5(158.5) | 158.8 | -14.9% |

| 1Q 2011 | 168.1 | 167.2 | -10.4% |

| 2Q 2011 | (170.6p)177.8 | 175.5 | -5.9% |

(p)=preliminary, based on Rockefeller Institute report

When I originally posted this chart last month, I noted that "If the current trend ... continues, the Rockefeller Institute estimate of a shortfall of $60 Billion in FY 2011 compared with 2008 appears accurate."

With this revenue surprise, that estimate looks too pessimistic to me. Through the first two fiscal quarters, 2011's shortfall compared with 2008 is only $9.2B, and only $0.9B of that is from 2Q. While this quarter's GDP is likely to be only weakly positive, that is enough to believe that fiscal 3Q 2011 revenues will at least be in line with 2Q 2011 revenues. In other words, nominal FY 2011 state revenues may only have a shortfall of $10B-$20B, rather than $60B - and if we avoid another recession, nominal state revenue may have no shortfall at all compared with pre-recession revenues by the end of this summer.

While this is welcome good news, real state tax revenues will still lag pre-recession levels, and per-capita revenues still further (since to keep an even level, services must grow with population).

The Reason There is No Pent-Up Consumer Demand

The following chart was printed on the Economists' Free Exchange Blog:

What the above statement does not explain is the reason for the upward sloping cure in consumer spending -- and, most importantly, whether it was sustainable -- which I would argue it wasn't. According to Census data, real median household income was stagnant for the first decade of the 2000's. Additionally, household debt continued to increase during that decade, eventually reaching over 130% of total DPI for U.S. households. That number (household debt/DPI) has been increasing for the last 30 years at a more or less constant pace. In other words, I believe the data indicates the pace of consumption was unsustainable, and was financed as much by debt financing as income growth. As such, the fall off caused by the recession was in fact a healthy and much needed correction in consumer behavior

My 2 cents (inflation adjusted).

While consumers are spending, as shown in the chart above, there has been no sign of pent up demand. Real consumer spending on goods fell off its pre-2008 trend line during the recession and has since resumed its former pace with no indications that a surge in spending to make up for lost time is imminent.(Mark Thoma also picked-up on this idea)

What the above statement does not explain is the reason for the upward sloping cure in consumer spending -- and, most importantly, whether it was sustainable -- which I would argue it wasn't. According to Census data, real median household income was stagnant for the first decade of the 2000's. Additionally, household debt continued to increase during that decade, eventually reaching over 130% of total DPI for U.S. households. That number (household debt/DPI) has been increasing for the last 30 years at a more or less constant pace. In other words, I believe the data indicates the pace of consumption was unsustainable, and was financed as much by debt financing as income growth. As such, the fall off caused by the recession was in fact a healthy and much needed correction in consumer behavior

My 2 cents (inflation adjusted).

Manufacturing -- Think Small

From the NY Times:

Think manufacturing, and most likely your brain defaults to abandoned factories, outsourcing and economically devastated regions like the Rust Belt. So strong is our tendency to focus on American manufacturing as something that’s been lost that a chorus has risen up to decry the prevalence of “ruin porn” — those aestheticized versions of the decidedly un-pretty, with a particular focus on the once-triumphant automotive center of the universe, Detroit.But there are many parts of this country where manufacturing is very much alive, albeit in a different form. The monolithic industry model — steel, oil, lumber, cars — has evolved into something more nimble and diversified. As this country continues to figure out how to crawl out of its economic despair, we could benefit from focusing on the shift.

.....

Industries like the record business, publishing and technology are constantly evolving in order to survive. Both SFMade and its New York cousin, Made in N.Y.C., are increasingly able to share success stories of how manufacturing has developed new models for doing business in the 21st century. The monolithic single-industry model has evolved as manufacturers see the benefits of being smaller and paying attention to how patterns of consumption, ownership and use are shifting.

An example of this might be a company like Anchor Steam Brewery, which started as a saloon in San Francisco’s North Beach neighborhood in 1896. The scent of hops tells you you’re in the Potrero neighborhood, where they’re still brewing beer and producing small-batch bourbon. Today’s consumer, says Anchor’s Keith Greggor, “is much more likely to back the local guy.” Or there’s recent arrival Jamieson Leadbetter, a fourth-generation baker whose grandfather gave him this advice when he decided to continue the Portland, Me.-based family business in San Francisco: “Pick your community well. You’re not there solely to make money; you’re there to play a larger role.”

I realize it's internet chic to bemoan the loss of U.S. manufacturing. But the facts are that is just not the case.

Tuesday, March 29, 2011

Gold Still Hitting Resistance

From Bloomberg:

From Bloomberg:“The more positive signs from the U.S. economy mean that the expectations of rate rises are starting to come back to people’s attention,” Darren Heathcote, head of trading at Investec Bank (Australia) Ltd. in Sydney, said today by phone. Higher rates “will inevitably take some of the shine off gold, decreasing its attractiveness to investors,” he said.

Four Important Positive Changes in the U.S. Economy

There are three underlying trends occurring in the U.S. Economy that are flying below the radar.

1.) The increased savings rate: for the last 10-15 years, the cry of "we don't save enough" has been been heard throughout the economic world. It was argued (and I believe correctly so) that the lack of savings was a sign the U.S. consumer was borrowing too much (see number 2 below) and spending too much, essentially living beyond his means (which he was). However, that has clearly changed, as the U.S savings rate has now increased during the first part of the latest recovery:

This is an important fundamental change. It will help us to finance the trade deficit and keep interest rates lower by increasing the supply of loanable funds.

2.) The decrease in household leverage. This is tied in with point number one. US households are still heavily indebted. Before the recession started, the household debt/disposable personal income ratio was over 130%. That number has now dropped to 114%. As a result, the financial obligations ration has been dropping sharply:

3.) The rebirth of US manufacturing: According to the national manufacturing readings, US manufacturing is literally on fire. Consider this chart of the ISM manufacturing index:

The ISM number is printing some of the strongest readings in over 20 years. Kash over at the Streetlight Blog has written some great articles on this (see links at the bottom of the page on this link).

4.) The rise of US exports: the US is no longer the primary driving force of the the world economy; developing economies (especially the BRIC) players are exerting a strong influence over international economics. The US is selling exported goods into this strength, which is clealry helped by a cheaper dollar. This has led to the rise of U.S. exports as an important part of the economic recovery:

And an oldie but a goodie -- I dug up this you tube video of me about two years ago talking about savings (I even mention Mish positively -- this was before he went off the reservation and into the great beyond):

1.) The increased savings rate: for the last 10-15 years, the cry of "we don't save enough" has been been heard throughout the economic world. It was argued (and I believe correctly so) that the lack of savings was a sign the U.S. consumer was borrowing too much (see number 2 below) and spending too much, essentially living beyond his means (which he was). However, that has clearly changed, as the U.S savings rate has now increased during the first part of the latest recovery:

This is an important fundamental change. It will help us to finance the trade deficit and keep interest rates lower by increasing the supply of loanable funds.

2.) The decrease in household leverage. This is tied in with point number one. US households are still heavily indebted. Before the recession started, the household debt/disposable personal income ratio was over 130%. That number has now dropped to 114%. As a result, the financial obligations ration has been dropping sharply:

3.) The rebirth of US manufacturing: According to the national manufacturing readings, US manufacturing is literally on fire. Consider this chart of the ISM manufacturing index:

The ISM number is printing some of the strongest readings in over 20 years. Kash over at the Streetlight Blog has written some great articles on this (see links at the bottom of the page on this link).

4.) The rise of US exports: the US is no longer the primary driving force of the the world economy; developing economies (especially the BRIC) players are exerting a strong influence over international economics. The US is selling exported goods into this strength, which is clealry helped by a cheaper dollar. This has led to the rise of U.S. exports as an important part of the economic recovery:

With housing and construction in the dumps and consumer spending pinched by thrift and tight credit, exports have powered nearly half of U.S. economic expansion since the recession ended in mid-2009There are still plenty of problems for us to deal with: a lackluster housing market and a high unemployment rate being at the top of the list. However, not all is bad; there have been some important fundamental changes for the better underneath the headlines.

(The article goes on to note the U.S economy is now more vulnerable to international economic swings because of this development.)

And an oldie but a goodie -- I dug up this you tube video of me about two years ago talking about savings (I even mention Mish positively -- this was before he went off the reservation and into the great beyond):

New Congresspeople Now Members of the Washington Lobotomy Factory

From the Washingtonpost:

This is just idiotic. Government spending accounts for about 20% of US GDP. In addition, it is a facilitator of many important transactions. Shutting it down would be a huge shock to the economy --- at a time when we can ill afford it (as if there is a time when we can afford this lunacy). Here's something that people in Washington seem to forget on a regular basis: C+I+X+G = GDP. It's called the GDP equation. The "G" stands for government. Since the equation uses addition, taking out one of the primary variables will probably lower the total (unless one of the other variables increases sufficiently to make-up for the loss).

Let's look at some of the primary areas effected by such blatant stupidity:

A breakdown late last week in closed-door negotiations between congressional leaders and the White House on funding the federal government makes it increasingly possible that Congress will not agree on a long-term funding resolution or another temporary measure by an April 8 deadline, aides from both parties said.Just when you thought the idiots in Washington couldn't get any dumber, they rise to the occasion, as if to say, "we can actually do something that much dumber than what we have previously accomplished. No -- really. We can. Just watch us."That means that the threat of a government shutdown — which had receded in recent weeks because of congressional approval of several stopgap funding measures — appears to be back on the table.

Problems with the negotiations became public late Friday, as revealed in comments from Sen. Charles E. Schumer (D-N.Y.) and the top three House Republican leaders. The apparent breakdown followed a Tuesday meeting among staff members for House Speaker John A. Boehner (R-Ohio) and Senate Majority Leader Harry M. Reid (D-Nev.) and representatives of the White House budget office on a possible deal for funding the government through the end of the fiscal year in September.

Democratic aides said talks had been underway for nearly two weeks between Boehner’s staff and the White House budget office, with steady progress leading to an agreement that the two sides would meet halfway between the $61 billion in cuts approved by the House and Democrats’ preference for maintaining current spending levels.

This is just idiotic. Government spending accounts for about 20% of US GDP. In addition, it is a facilitator of many important transactions. Shutting it down would be a huge shock to the economy --- at a time when we can ill afford it (as if there is a time when we can afford this lunacy). Here's something that people in Washington seem to forget on a regular basis: C+I+X+G = GDP. It's called the GDP equation. The "G" stands for government. Since the equation uses addition, taking out one of the primary variables will probably lower the total (unless one of the other variables increases sufficiently to make-up for the loss).

Let's look at some of the primary areas effected by such blatant stupidity:

The best guide for what consumers of government services can expect came in the last shutdown—the longest in U.S. history. After President Bill Clinton and a Republican Congress couldn't agree on spending, the government twice ran out of funding: from Nov. 14-19, 1995, and from Dec. 16, 1995 to Jan. 6, 1996.About 285,000 federal employees were sent home without pay and a further 476,000 were forced to work without pay. Clinton said on Jan. 20, 1996, that the shutdowns had cost the federal government a total of $1.5 billion, or $2.1 billion in today's dollars—a number that does not include indirect costs. (The total nonmilitary federal workforce has fallen from 2.92 million at the end of 1995 to 2.84 million at the end of 2009, according to the U.S. Office of Personnel Management.) When the shutdowns ended, all employees had back salaries paid.

.....

• A shortage of federal funds eventually led 11 states and the District of Columbia to stop providing unemployment benefits when they couldn't or wouldn't fill the gap with their own funds. Other benefits were slowed or stopped entirely: Veterans stopped receiving some payments, including insurance death claims and checks for education provided by the GI Bill. Delays hit recipients of federal welfare programs and adoption-assistance services, along with children in foster care and in the Head Start early childhood program. The Bureau of Indian Affairs closed, cutting off assistance payments to 53,000 people, while about 25,000 American Indians also stopped receiving checks for oil and gas royalties.

.....

About 200,000 Americans were left waiting for new passports after the State Dept. stopped processing applications. Visa applications by foreigners were left unprocessed, stacking up at a rate of 20,000 to 30,000 per day.

• Government economic reports that investors watch closely were stopped. Reports that might be blacked out this time include the January trade balance on Mar. 10 and data on February housing starts and building permits, due out on Mar. 16.

• Work on 3,500 bankruptcy cases was suspended. About half the employees of the Small Business Administration were placed on furlough, leading to 260 small businesses not receiving loans each day, according to a White House summary written in January 1996.

• National parks, national forests, and other federal monuments and museums were shut. In January 1996, Bloomberg News reported that kayakers and rafters were cut off from the Colorado River because they couldn't get permits.

• While federally funded health care such as Medicare continued, the National Institutes of Health stopped accepting new patients in clinical research programs. The Centers for Disease Control halted surveillance of diseases such as HIV/AIDS and influenza.

• The government temporarily closed the Federal Parent Locator Service, which helps find parents who are delinquent in making child support payments.

And there's much more in this detailed report.

At a time when the phrase "self-sustaining recovery" is gaining traction and credence, the yahoos in Washington want to completely derail the recovery. Great.

Monday, March 28, 2011

Are Durable Goods Orders Showing an Upcoming Slowdown?

This chart is bothering me. Notice that a large number of data points in the last year are concentrated in the 192,000-196,000 area. There have been some strong moves above that area, but only three times. Now let's look at a longer time series.

On the longer scale, notice that durable goods orders are still far below their peaks from the end of the last expansion. In addition, note their rate of ascent appears to have stalled, which is revealed in more detail on the following chart:

Above is a chart of durable goods orders on a scale of 100. Notice that orders have stalled in the 75-80 range for the last 10 months -- which is below previous levels.

Durable goods orders are a very volatile series. However, their current lack of movement is beginning to concern me regarding the big picture.

The Week Ahead

Stocks: The rally over the last week or so has been very weak. Volume has been down and half of the upward moves occurred at the open with no intra-day follow through. The SPYs are still contained by a downward sloping trend line. However, the IWMs (which have led the market higher) have broken through their trend line but also have a declining MACD. While the underlying technical are still OK (for example, the MACD is about to give a buy signal on the SPY) the underlying economic situation (weakening durable goods orders, high gasoline prices, increasing agricultural prices) are concerning.

Bonds: The IEFs are in a clear downward trend for the last eight days. Prices are currently right at the 200 day EMA. The 10 and 20 day EMA are both moving lower, but the EMAs are in a tight bunch right around the 200 day EMA. Prices are right below a short-term trend line. Additionally, before the latest rally, prices were moving lower in a move that looked like a flight from safety to risk, which is a standard move at this point in the market cycle. The real question is has the negative fundamental news which rallied the bond market over the last few weeks ameliorated to the point where bond traders are comfortable selling bonds into the risk markets again?

The dollar: the UUP ETF is still in a confirmed downtrend and has been since the beginning of the year. All the "rallies" have been upward sloping pennant patterns that hit resistance at an EMA and then moved lower. The ETF has moved through the 22 price area, which was an area of major technical support and is now moving higher, probably to retest the 22 price area. In addition, the market widely expects the EU to raise interest rates before the Fed, making the Euro a more attractive bullish play.

Oil: Oil is consolidating in a triangle pattern. Right now, the primary question is which direction will prices break in.

Bonds: The IEFs are in a clear downward trend for the last eight days. Prices are currently right at the 200 day EMA. The 10 and 20 day EMA are both moving lower, but the EMAs are in a tight bunch right around the 200 day EMA. Prices are right below a short-term trend line. Additionally, before the latest rally, prices were moving lower in a move that looked like a flight from safety to risk, which is a standard move at this point in the market cycle. The real question is has the negative fundamental news which rallied the bond market over the last few weeks ameliorated to the point where bond traders are comfortable selling bonds into the risk markets again?

The dollar: the UUP ETF is still in a confirmed downtrend and has been since the beginning of the year. All the "rallies" have been upward sloping pennant patterns that hit resistance at an EMA and then moved lower. The ETF has moved through the 22 price area, which was an area of major technical support and is now moving higher, probably to retest the 22 price area. In addition, the market widely expects the EU to raise interest rates before the Fed, making the Euro a more attractive bullish play.

Oil: Oil is consolidating in a triangle pattern. Right now, the primary question is which direction will prices break in.

{kind=link}

Subscribe to:

Posts (Atom)