- by New Deal democrat

April monthly data reported this past week included Case Shiller house prices up over 10% YoY, consumer confidence up sharply to five year highs, the Chicago manufacturing index up strongly to a six month plus high, personal income flat, the savings rate flat, and personal spending down slightly, but real income minus transfer payments up slightly. In the rear view mirror, Q1 GDP was revised down slightly.

Let's start this week's look at the high frequency weekly indicators by focusing on employment metrics, which are now decidedly mixed:

Employment metrics

American Staffing Association Index

- 94 up 1 w/w, down -0.5% YoY

- 354,000 up 14,000

- 4 week average 347,250 up 7,750

- $154.2 B 20 days into May vs. $135.6 B last year, up $18.6 B or +13.7%

Transport

Railroad transport from the AAR

- -9300 or -3.3% carloads YoY

- -4100 or -2.3% carloads ex-coal

- +3400 or +1.4% intermodal units

- -5900 or -1.1% YoY total loads

- Harpex unchanged at 398

- Baltic Dry Index down 17 to 809

Consumer spending

- ICSC -0.9% w/w +2.8% YoY

- Johnson Redbook +2.7% YoY

- Gallup daily consumer spending 14 day average at $89 up $15 YoY

Housing metrics

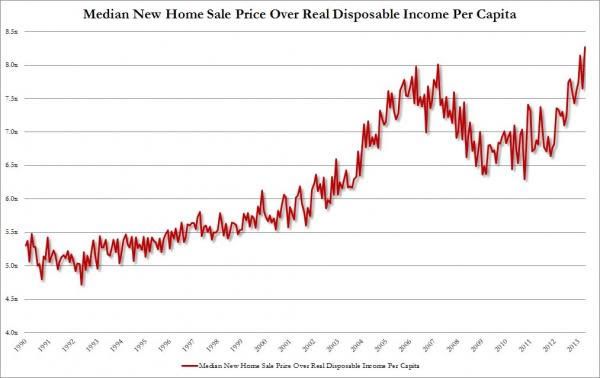

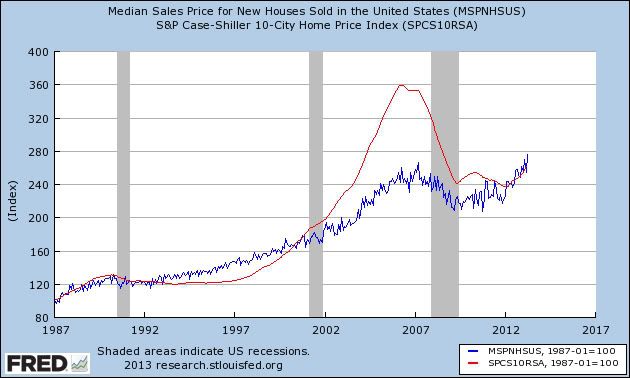

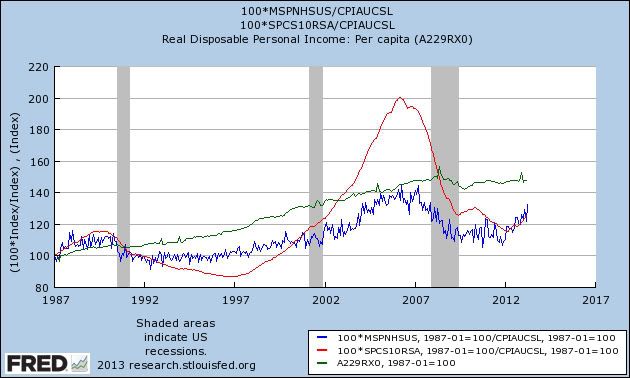

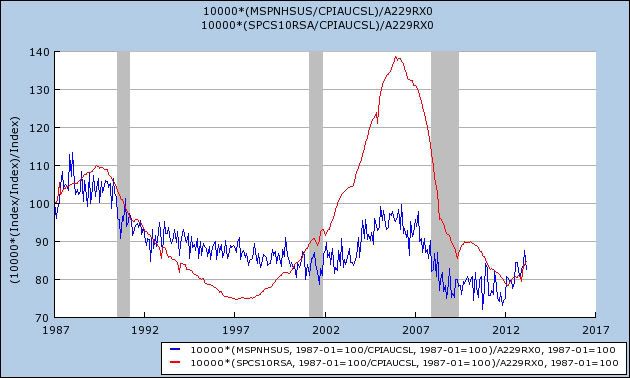

Housing prices

- YoY this week +6.8%

Real estate loans, from the FRB H8 report:

- up 0.1% w/w

- up +0.5% YoY

- +2.2% from its bottom

Mortgage applications from the Mortgage Bankers Association:

- +3% w/w purchase applications

- +14% YoY purchase applications

- -12% w/w refinance applications

Interest rates and credit spreads

- 4.78% BAA corporate bonds up +0.04%

- 1.99% 10 year treasury bonds up +0.06%

- 2.79% credit spread between corporates and treasuries down -.02%

Money supply

M1

- +0.2% w/w

- -0.5% m/m

- +10.0% YoY Real M1

M2

- -0.1% w/w

- +0.2% m/m

- +5.7% YoY Real M2

Oil prices and usage

- Oil $91.97 down -$1.86 w/w

- Gas $3.64 down -$0.03 w/w

- Usage 4 week average YoY -2.5%

Bank lending rates

- 0.25 TED spread up +.02 w/w

- 0.1940 LIBOR down +0.001% w/w

JoC ECRI Commodity prices

- down -0.32 to 124.84 w/w

- +6.03 YoY

The most important negatives are the actual decline in temporary staffing and in railroad traffic. Also negative this week were mortgage refinancing and treasury bonds, reflecting the bond selloff. Jobless claims were negative for the week, but more neutral compared with the last several months, and real estate loans, just barely positive YoY. Shipping was also neutral, and gas uage is negative but may continue to reflect increased efficiency.

Positives included house prices, YoY purchase mortgage applications, commodities, money supply, and overnight bank rates. Consumer spending was strong again. The spread between corporate and treasury bonds contracted. Gas prices moved lower. Withholding taxes had their best 20 day period since January.

For me to be sold that the data is actually rolling over, I would want to see a sustained increase in jobless claims and a sustained deterioration in consumer spending. That isn't happening now.

Have a nice weekend.

{kind=link}

{kind=link}