During the third quarter that just ended, the Standard & Poor's 500-stock index posted a gain of 10.7%, but it didn't get much help from some of the country's biggest banks. The Keefe, Bruyette & Woods Bank Index—which tracks 24 bank stocks, with the four heaviest weightings for Citigroup, J.P. Morgan Chase, Bank of America and Wells Fargo—was little changed.Bank of America tumbled 8.8% and Wells Fargo slipped 1.9%. Citigroup, J.P. Morgan Chase and Morgan Stanley saw their shares gain modestly, by between about 4% and 6%, clipped by uncertainty over new rules from U.S. and global banking regulators.

Financials, taken more broadly, have also been the worst performing sector on the S&P 500 since that index reached its 2010 peak on April 23.

The mortgage-foreclosure crisis spilled into the financial markets on Thursday, driving down bank stocks and weighing on mortgage bonds as investors took a grim view of the potential costs.Shares of U.S. banks fell, while the broader stock market was essentially flat. Bank of America Corp., potentially among the most affected, dropped more than 5%. Bank bonds also fell, and the cost of buying protection against a possible debt default by banks climbed.

"The level of uncertainty in the economy is at extraordinarily high levels to begin with," said Jack Scott, chief investment officer at BlackHawk Capital Management, a Charlotte, N.C., money manager that owns mortgage securities. "The foreclosure problem adds another layer of acute uncertainty."

So far, the foreclosure crisis hasn't affected consumer mortgage rates, which remain near record lows. They are closely linked to rates on U.S. Treasurys, which have tumbled in recent months.

The crisis has been escalating for several weeks, as banks suspend foreclosures across the country, citing flaws they have uncovered, including faulty or missing documentation. Tales of mismanagement within the foreclosure process—including so-called robo-signers, who were paid to rubber stamp documents without properly reviewing them—are emerging daily.

According to S&P, financial stocks account for 15.7% of the S&P 500 average, meaning they are really important. Every weekend I run an ETF performance chart on stockcharts.com. The last three weeks, this area of the market has distinctly underperformed other areas of the market.

Here is a chart that compares the two sectors

Notice that last month, the SPYs (the yellow line) rallied while the XLFs (the orange line) stood still. The sectors that are driving the rally are basic materials, energy, consumer discretionary and industrial stocks:

Oil prices are still in a tight range (A), although prices are right at the top of this trading range (B).

Oil prices are still in a tight range (A), although prices are right at the top of this trading range (B). Copper prices are still in a strong uptrend (A), with a very bullish EMA picture ((B) all moving higher and shorter about longer) with a rising MACD (C).

Copper prices are still in a strong uptrend (A), with a very bullish EMA picture ((B) all moving higher and shorter about longer) with a rising MACD (C). Lumber may have broken out of its trading base (A).

Lumber may have broken out of its trading base (A).

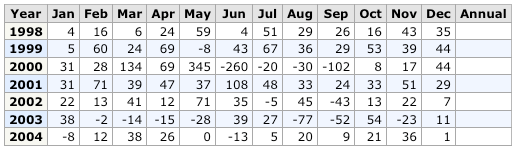

After improving five of the last six weeks, initial jobless claims rose 13,000 in the October 9 week to a higher-than-expected 462,000 (prior week revised 4,000 higher to 449,000). The Labor Department had to use estimates for five states due to administrative delays tied to this week's Columbus Day. The four-week average, up 2,250 to 459,000, ended six straight weeks of improvement.

Two-thirds of Tea Party supporters also would consider cutting spending on roads and bridges;

One-quarter of the 599,893 bridges in the United States have structural problems or outdated designs. The country can do more than rebuild these bridges—we can make them better, using high-performance concrete, steel and composites; automated monitoring systems to watch for deterioration; and smarter designs. Similar technologies can also be employed on highways, tunnels and other structures.

.....

About 28.9 million shipping containers passed through crowded U.S. ports last year, and gridlock is mounting. Containers entering the country languished on docks an average of seven days. Adopting the “agile port system” now being developed with help from federal agencies would boost efficiency. When the concept was tested at Washington’s Port of Tacoma, it cut cargo delays in half.

The projects are no[t] economically viable. They don't create any new wealth. When the old bridges are torn down (many still work just fine) and new ones are built, hundreds of billions of dollars would have been spent and all that will need to be paid back with interest, and the much of the spending would have drifted out of the US in the form of imports and higher commodity prices.

Better policy options would be the elimination of the corporate tax for all domestic manufacturing operations and the elimination of the payroll tax altogether (social security will be paid for in the short term from the general fund).

The interstate highway system made less expensive land more accessible to the nation's transportation system and encouraged development.

The travel time reliability of shipment by interstate highway has made "just in time" delivery more feasible, reducing warehousing costs and adding to manufacturing efficiency.

By broadening the geographical range and options of shoppers, the interstate highway system has increased retail competition, resulting in larger selections and lower consumer prices.

By improving inter-regional access, the interstate highway system has helped to create a genuinely national domestic market with companies able to supply their products to much larger geographical areas, and less expensively.

Michael Shedlock has an awesome takedown of ECRI’s claim that its indicators (a) have successfully predicted turning points in the past (b) point to a sold recovery now. I’d add that this is a really, really bad time to be relying on conventional indicators.Lakshman Achuthan of ECRI responded with a very specific challenge:

Why? Basically, because in a zero-interest rate world — the three-month rate was .066% last I looked — especially one that’s suffered from a collapse of the shadow banking system, conventional indicators don’t mean what they usually mean. Increases in the monetary base aren’t especially expansionary. The yield curve more or less has to slope up, even if no recovery is expected. And so on.

So historical correlations, to the extent that they exist — and as Shedlock points out, ECRI is claiming a much better record than it really has — can’t be counted on to prevail. There’s really no alternative to making fundamental analyses of the macro situation.

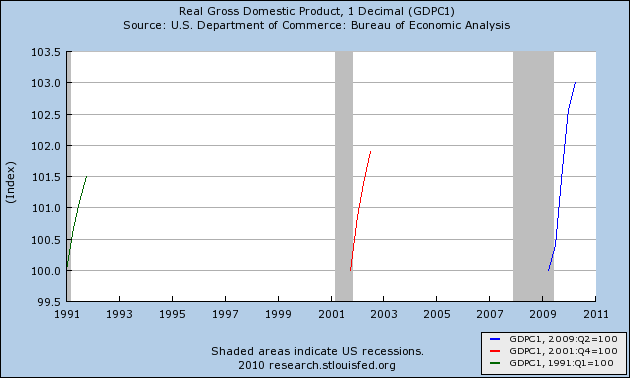

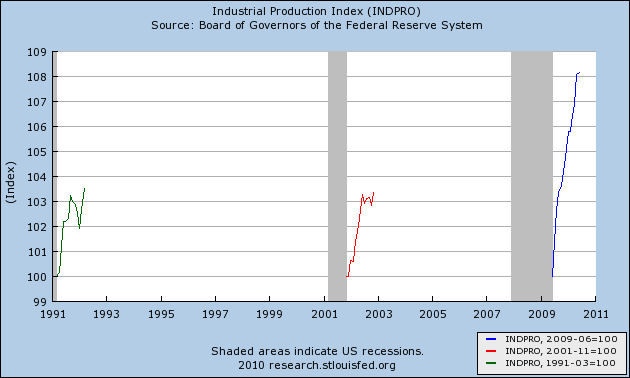

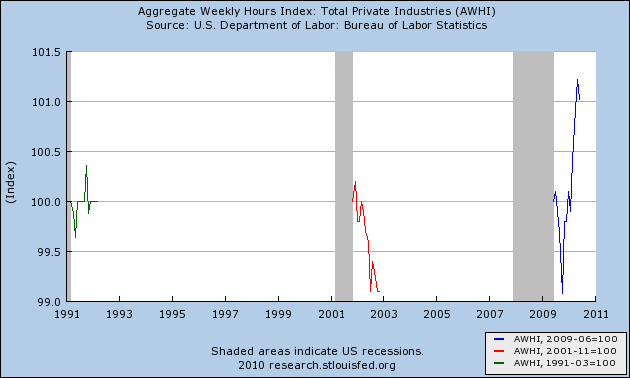

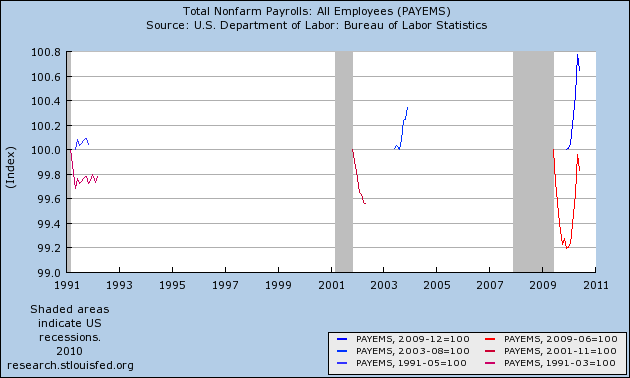

we fully expect the current economic recovery to prove to be stronger than the last two, at least through mid-2010....It is exactly one year later today. So, was "the current economic recovery stronger than the last two, at least through mid-2010?" The data is in, and we have an answer.

While we don’t necessarily expect our clarifications to change your views about the near-term course of the business cycle, we would hope that if, a year from now, ECRI’s leading indexes are proven to have been correct, you would publicly acknowledge the same. After all, the proof is in the pudding.

A number of participants noted that the current sluggish pace of employment growth was insufficient to reduce unemployment at a satisfactory pace. Several participants reported feedback from business contacts who were delaying hiring until the economic and regulatory outlook became more certain. Participants discussed the possible extent to which the unemployment rate was being boosted by structural factors such as mismatches between the skills of the workers who had lost their jobs and the skills needed in the sectors of the economy with vacancies, the inability of the unemployed to relocate because their homes were worth less than their mortgages, and the effects of extended unemployment benefits. Participants agreed that factors like these were pushing the unemployment rate up, but they differed in their assessments of the extent of such effects. Nevertheless, many participants saw evidence that the current unemployment rate was considerably above levels that could be explained by structural factors alone, pointing, for example, to declines in employment across a wide range of industries during the recession, job vacancy rates that were relatively low, and reports that weak demand for goods and services remained a key reason why firms were adding employees only slowly.A recent speech by the chair of the Minneapolis Federal Reserve sparked a debate about the nature of the unemployment in the US. Here are the key paragraphs:

If one digs deeper into the data, the situation seems even more troubling. Since December 2000, the Bureau of Labor Statistics has been keeping data on the job openings rate, which is defined as the number of job openings divided by the sum of job openings and employment. It has also been keeping track of the layoffs/discharges rate, which is the fraction of employed people who have been laid off or discharged in a given month. The job openings rate rose by around 30 percent between July 2009 and July 2010. The layoffs/discharges rate has fallen by over 10 percent over the same period.Nonetheless, despite this apparent increase in the demand for labor from employers, the unemployment rate actually went up slightly from July 2009 to July 2010, from 9.4 percent to 9.5 percent. And other measures of labor market performance actually tell an even bleaker story. From July 2009 to July 2010, the employment/population ratio fell from 59.3 percent to 58.4 percent. At the same time, the seasonally adjusted labor force participation rate fell from 65.4 percent to 64.6 percent. This was the biggest July-over-July fall in the 60-plus year history of that statistic.

What he is noting here is the number of job openings is increasing while the pace of job discharges is decreasing. This indicates that employers are increasing their hiring plans. This has led some to conclude that US unemployment is structural, meaning there is a mis-match between what employers want in an employee and the skills the employee brings to the table. The logic continues that this mis-match is the cause of the high unemployment rate.

The Boston Fed also did research into this issue and found the following:

Some hypothesize that a more robust recovery is impeded by dislocations in the labor market. Indeed, history shows that even with a relatively mild recession there can be significant dislocations. The 2001 recession provides a good example. As Figure 1 shows, information technology and manufacturing were two industries that saw significant declines in employment in that downturn. The end of the “dot-com” euphoria and structural shifts in the manufacturing sector caused those two industries to be disproportionately affected, while we had only modest declines in the cyclical construction industry, and increases in employment in several industries. Similarly, the 1990 recession had a decline in employment of more than 5 percent in only the construction industry, when overbuilding in several regions of the country led to a significant readjustment in construction-industry employment.

In fact, in each of the three previous recessions there was a decline of 5 percent or more in no more than two industry categories – as the figure shows – with many industries experiencing little or no net job loss over the course of the recession. Structural shifts across industries are not uncommon in recessions – and also, some structural dislocation seems inevitable as it will always take some time for capital and labor to flow to those industries with the greatest opportunities.

In rather stark contrast, the most recent recession is far less a reflection of dislocation in a few industries but rather reflects a general decline in almost all industries. As the chart on the far right shows, in this recession there has been a peak to trough loss of employment of 5 percent or greater in construction, manufacturing, retail trade, wholesale trade, transportation, information technology, financial activities, and professional and business services. To me, this does not suggest that the driver is structural change in the economy increasing job mismatches – although no doubt some of that exists – but instead I see here a widespread decline in demand across most industries.

Here is the accompanying chart

What the Boston Fed is arguing is the breadth of job losses indicates this is not a structural realignment, but instead a far more in-depth recession. Structural realignment means there is a significant issues/problem hitting a few industries and not the economy as a whole. The Boston Fed's research indicates that in several of the earlier recession, a limited number of industries lost jobs. For example, the .com bust lowered the demand for technology workers, while the real estate bust of the early 1990s lowered the demand for construction workers.

Personally, I believe the Boston Fed's research is more compelling, as does the Federal Reserve, which noted:

Nevertheless, many participants saw evidence that the current unemployment rate was considerably above levels that could be explained by structural factors alone, pointing, for example, to declines in employment across a wide range of industries during the recession, job vacancy rates that were relatively low, and reports that weak demand for goods and services remained a key reason why firms were adding employees only slowly.

However, this does not mean the structural argument is completely wrong. For example, I think it is highly doubtful we'll see a big upswing in construction anytime soon, largely because of the huge overhang in existing home inventories. As such, there is a structural component to the construction industry's unemployment situation. But I also think the breadth of the job losses indicates the structural reasons for unemployment are in the minority.

The World Bank has become the latest to join the chorus of policy-makers praising Latin America’s recovery from the global financial crisis, but warned further reforms are needed to ensure that recent successes were extended into durable growth.The World Bank Recently Reported:In an ebullient report entitled “The New Face of Latin America”, the World Bank said past crises had immunised the region, so that during this financial crisis while advanced economies caught pneumonia, Latin America “only got a cold”.

By next year, Latin America will have regained all ground lost during the crisis, the World Bank said, with Brazil’s economy leading the way. This better-than-expected result, with forecast regional growth of 6 per cent this year and 4 per cent in 2011, was due to a decade of improved monetary policy, better fiscal management, and the hemisphere’s growing trade links with Asia.

Furthermore, Latin America had made greater use of equity finance and direct investment rather than debt to bridge local saving gaps. This had left the region a net creditor to the rest of the world. As a result, free-floating currencies could devalue during the global crisis without increasing the local cost of servicing hard currency debt – a hard won lesson from the region’s debt crises of the past.

Latin America’s new face following the global financial crisis is tough and almost impervious to shocks but also soft and kind to the most vulnerable.

A World Bank report argues that the region’s economic demeanor is resilient, globalized, and dynamic as it zips towards 5-6 percent growth for 2010 and shows that its investments in social protection managed to shield the most vulnerable from the worst effects of the downturn.Presented as part of the World Bank Annual Meetings, Latin America’s semiannual economic report also reveals that the region’s recovery is ahead of the rich nation’s and compares well with the Asian Tigers’ expected growth of over 7 percent. All in all, the crisis in Latin America & Caribbean (LAC) was short lived, as compared to other parts of the globe, thanks in part to solid macroeconomic and fiscal frameworks set in place well before the crisis struck.

.....

Here are the primary reasons for the resurgence:

1) Improved macroeconomic and financial policy frameworks that have become shock absorbers or cushions rather than conduits to amplify crises. These improvements include strong currencies –which in the past were shock transmitters - and countercyclical fiscal policies that have allowed for potent fiscal stimulus during the crisis. Banking systems have also been strengthened and currently there are enough buffers in place –such as liquidity and capital provisions- to endure a shock without infecting the rest of the economy.

“That’s a very importance factor that explains LAC’s resilience and why it’s recovering very nicely in this phase,” said de la Torre.

2) Integrating better into global financial markets has allowed the region to become a net creditor to the world rather than a debtor -a move that provided a cash cushion against downturns. In the past, Latin America used to hold an excess of debt contracts that exposed it to rollover risks, interest rates hikes, and sentiment changes, that could wreak havoc in its finances. These days the region is a large debtor on the equity side, including Foreign Direct Investments (FDI), and a creditor on the debt side, which forms a more robust debt mix. FDI surpassed the $60 billion mark in 2010 almost reaching 2007 levels.

3) Diversification of its trade structures has placed Latin America in a unique position to profit from China’s voracious appetite for the region’s commodities while desensitizing it from economic activities in rich areas such as Europe, the United States and Japan. Much of the region’s growth can be credited to the ‘China Connection’, which saw the country’s share of commodity exports grow tenfold since 1990 (from 0.8 percent in 1990 to 10 percent of total commodity exports in 2008).

The World Bank article has a link to a very interest PDF on the region: highly recommended.

{kind=link}