Saturday, January 27, 2018

Weekly Indicators for January 22 - 26 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com. Aside from more mixed long leading indicators, there has been this anomalous decline in rail and steel.

Friday, January 26, 2018

Leading components of Q4 GDP forecast continued growth in 2018

- by New Deal democrat

This morning's release of Q4 2017 GDP was in line with estimates, rising 2.7% on a preliminary basis. As usual, my attention is focused less on where we *are* than where we *will be* in the months and quarters ahead.

There are two leading components of the GDP report: real private residential investment and corporate profits. Because the latter will not be released until the second or third revision of the report, I make use of proprietors' income as a more timely if less reliable placeholder.

So let's take a look at each.

The news on real private residential fixed investment was mixed. Measured both by itself (blue), and by the more precise method of its share of the GDP as a whole (red), residential investment rose. But although it came close, it has not made a new high since three quarters ago:

Proprietors' income was clearer, breaking out to another new high:

Together these are pretty strong evidence that the economy will continue to expand through the rest of 2018.

One final note: although the GDP reports have been good for the last three quarters, I'm not expecting any big positive breakout. This goes back to the relative flatness or restrained growth in housing. The below two graphs show the leading relationship between housing permits (using the less volatile single family measure) and GDP broken up into two roughly 30 year periods:

The YoY% change in permits for the last 3 years has been roughly 10% (divided by 4 for purposes of scale in the above graphs shows a number of ~2.5%). While there is certainly not a 1:1 relationship in the numbers, continued roughly 2.5% YoY growth of GDP for the next few quarters is a reasonable projection.

Thursday, January 25, 2018

Housing: sales and prices accelerate in Q4 2017

- by New Deal democrat

With the exception of rental vacancies and pricing, which should be released next Tuesday, with the morning's release of new home sales we now have a good look at the very forward-looking housing market through the end of 2017.

Both sales and prices have started to accelerate. This post is up at XE.com.

Wednesday, January 24, 2018

A note on December existing home sales

- by New Deal democrat

First of all, sorry for the light posting this week. There's not much news until tomorrow and Friday, and yesterday was a travel day. So.....

While existing home sales are about 90% of the entire housing market, they are the least important economically, because of their much more limited impact since they do not involve any new construction.

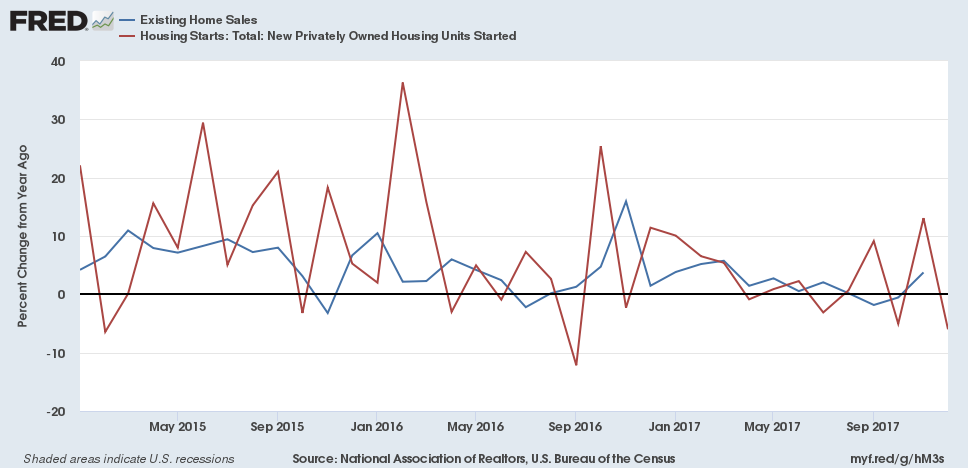

That being said, December's existing home sales, at 5.57 million annualized, were only 1% above last December's pace. First and foremost, that's a matter of higher mortgage rates this year. In fact, mortgage rates haven't made a meaningful new low since 2013 -- although they briefly neared that low in late 2016 -- and that has shown up in a gradual deceleration of the pace of sales since that time, as show by Bill McBride's graph below:

Here is a close-up of the last three years from FRED, excluding today's report, which hasn't been posted yet:

Here's the same data YoY, compared with housing starts in red, averaged quarterly to cut down on the volatility:

The same pattern of decelerating growth is shown in both series.

Although sales turn before either prices or inventory, the consistent price increases and lack of inventory are playing a role in this deceleration, contra which is the demographic tailwind.

Tomorrow the more important, and leading (but very volatile) new home sales report will be released. I am expected a significant downward revision in November's blowout number.

Tuesday, January 23, 2018

Recent increased interest rates probably won't derail housing

- by New Deal democrat

In the last couple of weeks, long term interest rates have moved significantly higher. As of yesterday, the 10 year bond closed at roughly 2.66%, its highest yield in 3 1/2 years. If this move is sustained for a few months, I expect it to have an effect on the housing market, but how much?

Here is an updated variation on a graph I have run many times over the last 5 years: the YoY change in the 10 year treasury bond, inverted (blue), versus the YoY% change in housing permits for single family homes (green). I'll explain the red line below:

In general, the housing market responds first and foremost to interest rates. So when interest rates rise (shown as a negative YoY in the graph), permits historically have fallen.

But in this expansion, permits have responded by decelerating increases rather than by actual declines. A decent estimate is that the demographic tailwind of the large Millennial generation arriving at home-buying age is that it has added 7.5% growth YoY vs. what we would otherwise expect. That is what is shown by the red line in the graph above.

I still expect a few months of restrained *YoY* growth (not m/m, which has already increased to new highs) before improvement in that metric.

But the above graph does not show the uptick in rates this month, so the below is the same graph, limited to the last year, but with daily values in treasury rates:

The bottom line is that the recent increase in rates isn't enough to derail the housing market. I suspect that rates would have to go above their 2013 high of 3.03% for that to happen.

Finally, there is another factor to consider, which is monthly mortgage payments. As I pointed out several months ago, monthly mortgage payments got downright cheap at the bottom of the housing market, and still are quite reasonable compared with their 2005 highs. Here's an update graph of real, inflation-adjusted mortgage payments from Core Logic:

This is probably also a factor in why housing has responded relatively tepidly to changes in interest rates. Especially with soaring rents and constrained supply, owning is -- relative to renting -- still a bargain. It will probably take another 10% increase in real monthly carrying costs for that to become at all comparable to its surge during the housing bubble.

Subscribe to:

Posts (Atom)