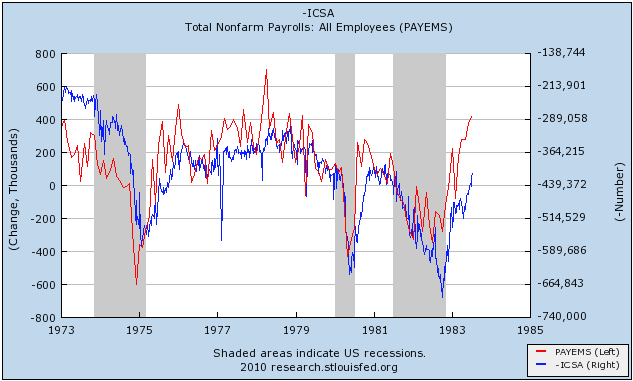

So, let's take a journey back to the early 80's when The Smith's were just getting started, the Weather Channel went live, Ripken had just began his streak, and the last decade in which the Yankees didn't win the World Series.

The recession that began in July 1981 (and followed on the heels of a recession that had just ended a year earlier) was the deepest (at the time) since the depression with unemployment topping out at 10.8% and GDP falling 2.6% over the recession. The recovery that followed this recession, however, was very robust (for several reasons) as we can see here looking at the decline in the unemployment rate (compared to GDP) and the change in payrolls (I adjusted this to compare to today's much higher population in rough terms):

As you can see here, the initial recovery was incredibly strong in terms of both employment and GDP, but as the decade languished, unemployment remained stuck around 7% even with consistent GDP growth above 2.5%. The reason I used an adjusted payroll growth number was to give a better illustration for purposes of comparing the positive job gains of the 80's recovery to what we may begin to see later this year (likely next month).

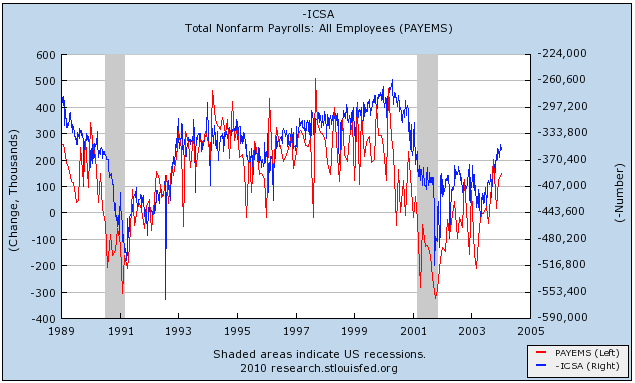

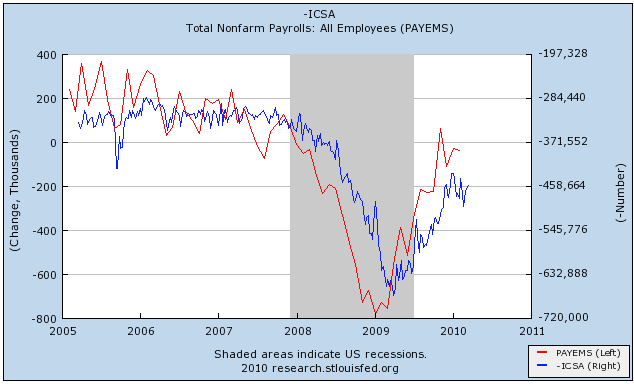

Now, let's look at some comparisons to where we are now versus then (pardon the hard to read nature of these):

This first graph shows (in percent change terms) payroll growth coming out of each recession. Not only do we start with a larger hole to dig out of, but the early 80's recovery was already positive by now and then exploded over the course of that first year or so (we can use this graph to compare later on this year).

Next, looking at GDP shows us that we are already behind the 80's recovery here and that it is looking highly unlikely that we are going to catch up

as the initial 80's recovery saw two quarters in excess of 7.5% to kick it off, while we are looking at two Q's just above 5%. That will come back to haunt us later.

Finally, let's look at some of the drivers of the 80's recovery and see why we are not set up nearly as well as back then. First up is the elephant in the room, interest rates:

While these look very high compared to today, they essentially fueled the recovery by allowing significant refinancing (and lower business costs) activity that continued for the next 25+ years to some extent. The level of these rates also kept the economy more honest, as everything had to be evaluated against a 10-year bond that was never below 7% for the decade (ie no need to chase yields and speculation). These interest rates also kept savings high

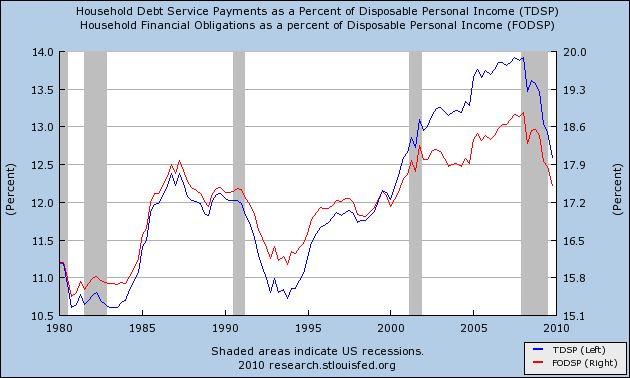

which help to provide an economic backstop and can fuel growth as the rate declines (not necessarily good in the long run, but can lead to larger growth over a shorter term). Finally, we need to look at debt levels, as expanding levels of debt (to a certain point) can have a huge impact on growth

and as we can see here, as the 80's progressed we saw debt service jump by nearly 20%, which helped to fuel the expansion.

So what does all of this say about the situation facing us today? Well, we do not have the catalysts that the 80's had to fuel a large economic expansion. Our savings rate is low and looks to be rising (good for long term, but bad in the short run). Our debt service rate high (and even after a spectacular decline is still higher than the 80's peak), which will limit our ability to use household debt (ie consumption) to jumpstart a recovery. Interest rates are already at historic lows, which will prevent significant refinancing activity from helping out families and will also create a huge ceiling on home prices going forward as rates rise. Finally, our initial burst out the gate simply wasn't fast enough to make up the ground we lost. In other words, we are likely going to be facing a recovery/expansion that has many more risks to the downside than it does catalysts to the upside and we will be doing it this time without the luxury of having a Keynesian backstop should we falter again.

For Bruce:

{kind=link}

{kind=link}