Saturday, December 2, 2017

Weekly Indicators for November 27 - December 1 at XE.com

- by New Deal democrat

My Weekly Indicators post is up at XE.com.

The economy is firing on nearly all cylinders right now. Meanwhile there have been two changes among the long leading indicators.

Friday, December 1, 2017

Extreme measures?

- by New Deal democrat

Are stock prices at extreme levels? I take an updated look at the relationship between the long leading indicator of corporate profits, and stock prices.

This post is up at XE.com.

Where's Waldo, er, I Mean Inflation?

Just a quick note: according to the 3, 6 and 12 month moving average of Y/Y percentage change in total and core PCE price indexes, there is little to no inflation to worry about.

Thursday, November 30, 2017

What Bill McBride says

- by New Deal democrat

Bill McBride a/k/a Calculated Risk hits the nail on the head:

The current tax cut bill is a[ ] clear policy mistake.

First, if we look at the business cycle and the deficit, economic theory suggests that the government should increase the deficit during economic downturns, and work down the deficit during expansions. The economy is currently in the mid-to-late stage of a recovery, so decreasing the deficit makes sense now - not increasing the deficit.This is particularly so since after ten years, the economy has finally made it back to its long term trendline growth (via WaPo):

For the first time since the end of 2007, the economy, measured as gross domestic product (GDP), is at its (theoretical) potential.

There is simply no rational excuse for a producer-sided tax cut. The economy is not suffering from a lack of supply. It's one big problem is the lack of real long-term growth in middle, working, and lower class incomes, constraining demand.

Two points of my own:

1. One way I depart from progressive orthodoxy is that I favor a ***COUNTERCYCLICAL*** (have I made that emphatic enough?) balanced budget amendment, mandating surpluses in good economic times (like now), to pay for deficits in hard times like recessions.

2. The GOP's Johnny-one-note "tax cuts for the wealthy are always good!" orthodoxy -- which by the way means they have no longer believe in the 'Laffer Curve' since that theory agrees that there is a tipping point below which tax cuts do raise total revenues -- means that if a recession hits while they are in power between now and 2020, they will do nothing to alleviate the pain for the vast majority of Americans, If anything, if the "fiscal trigger" survives, mandating budget cuts or tax increases during a recession (when declining tax revenues mean bigger deficits), the pain will actually be intensified.

A Solid GDP Report

The BEA released their latest estimate of 3Q GDP, which had

a 2.3% Y/Y headline number percentage change.

The following table shows that gains were broad:

The pace of Y/Y growth is increasing:

The following charts highlight several important aspects of

the report:

Equipment investment (top chart) and, more specifically,

industrial equipment investment (bottom chart) have increased for four and six

quarters, respectively.

However, residential investment may be topping:

The top chart shows total residential investment while the

bottom chart is residential construction.

Both have recently stalled.

Consumers

continue to spend at a consistent pace:

The top chart shows total PCEs, which have printed between

2.5%-3% for some time. Durables goods

spending (middle chart) ticked higher while non-durable goods spending (bottom

chart) has improved solidly over the last few quarters.

There is very little to be concerned about in this report.

Wednesday, November 29, 2017

Mid-Week Bond Market Round-Up

Yellen's Congressional Testimony:

Even with a step-up in growth of economic activity and a stronger labor market, inflation has continued to run below the 2 percent rate that the Federal Open Market Committee (FOMC) judges most consistent with our congressional mandate to foster both maximum employment and price stability. Increases in gasoline prices in the aftermath of the hurricanes temporarily pushed up measures of overall consumer price inflation, but inflation for items other than food and energy has remained surprisingly subdued. The total price index for personal consumption expenditures increased 1.6 percent over the 12 months ending in September, while the core price index, which excludes energy and food prices, rose just 1.3 percent over the same period, about 1/2 percentage point slower than a year earlier. In my view, the recent lower readings on inflation likely reflect transitory factors. As these transitory factors fade, I anticipate that inflation will stabilize around 2 percent over the medium term. However, it is also possible that this year's low inflation could reflect something more persistent. Indeed, inflation has been below the Committee's 2 percent objective for most of the past five years. Against this backdrop, the FOMC has indicated that it intends to carefully monitor actual and expected progress toward our inflation goal.

Kashkari: no reason to raise rates right now:

“Because inflation is low, I am seeing no reason to tap the brakes on the economy,” Kashkari said in a Town Hall event at Winona State University in Minnesota and broadcast via the Minneapolis Fed’s website. A rate hike would be expected to slow the economy by reducing incentives for borrowing, investing and hiring.

Dudley thinks inflation will rebound and is therefore in the rate hiking camp:

Dudley, a close ally of Fed Chair Janet Yellen who is set to step down in mid-2018, said that with unemployment having fallen to 4.1% the U.S. central bank thinks the economy has reached “full employment.” Theoretically, that is that unemployment can get without prompting inflation; the Fed’s preferred price measure has drifted down to 1.4% this year, below a 2-% target.

Thus “we have been gradually raising interest rates,” he said, repeating that he expects inflation to rebound along with wage gains.

Are there different reasons for the yield curve flattening?

When the Federal Reserve raises short-term interest rates, the rates on longer-term Treasuries are generally expected to rise. However, even though the Fed has raised short-term interest rates three times since December 2016 and started reducing its asset holdings, Treasury yields have dropped instead. This decoupling of short-term and long-term rates is reminiscent of the “Greenspan conundrum” of 2004–05. This time, however, evidence suggests compelling explanations—a lower “normal” interest rate, the risk of persistently low inflation, and fiscal and geopolitical uncertainty—may account for the yield curve flattening.

Flattening yield curve faces test of its predictive powers (FT)

Even with a step-up in growth of economic activity and a stronger labor market, inflation has continued to run below the 2 percent rate that the Federal Open Market Committee (FOMC) judges most consistent with our congressional mandate to foster both maximum employment and price stability. Increases in gasoline prices in the aftermath of the hurricanes temporarily pushed up measures of overall consumer price inflation, but inflation for items other than food and energy has remained surprisingly subdued. The total price index for personal consumption expenditures increased 1.6 percent over the 12 months ending in September, while the core price index, which excludes energy and food prices, rose just 1.3 percent over the same period, about 1/2 percentage point slower than a year earlier. In my view, the recent lower readings on inflation likely reflect transitory factors. As these transitory factors fade, I anticipate that inflation will stabilize around 2 percent over the medium term. However, it is also possible that this year's low inflation could reflect something more persistent. Indeed, inflation has been below the Committee's 2 percent objective for most of the past five years. Against this backdrop, the FOMC has indicated that it intends to carefully monitor actual and expected progress toward our inflation goal.

Kashkari: no reason to raise rates right now:

“Because inflation is low, I am seeing no reason to tap the brakes on the economy,” Kashkari said in a Town Hall event at Winona State University in Minnesota and broadcast via the Minneapolis Fed’s website. A rate hike would be expected to slow the economy by reducing incentives for borrowing, investing and hiring.

Dudley thinks inflation will rebound and is therefore in the rate hiking camp:

Dudley, a close ally of Fed Chair Janet Yellen who is set to step down in mid-2018, said that with unemployment having fallen to 4.1% the U.S. central bank thinks the economy has reached “full employment.” Theoretically, that is that unemployment can get without prompting inflation; the Fed’s preferred price measure has drifted down to 1.4% this year, below a 2-% target.

Thus “we have been gradually raising interest rates,” he said, repeating that he expects inflation to rebound along with wage gains.

Are there different reasons for the yield curve flattening?

When the Federal Reserve raises short-term interest rates, the rates on longer-term Treasuries are generally expected to rise. However, even though the Fed has raised short-term interest rates three times since December 2016 and started reducing its asset holdings, Treasury yields have dropped instead. This decoupling of short-term and long-term rates is reminiscent of the “Greenspan conundrum” of 2004–05. This time, however, evidence suggests compelling explanations—a lower “normal” interest rate, the risk of persistently low inflation, and fiscal and geopolitical uncertainty—may account for the yield curve flattening.

Flattening yield curve faces test of its predictive powers (FT)

Tuesday, November 28, 2017

New Home Sales Were Broadly Higher

When I first saw that new home sales increased, I naturally thought that a post-hurricane bump occurred. But the increase was far broader:

The South region -- which includes Texas and Florida -- did increase; it rose 1.3%. But notice the incredibly large increases in the NE -- which rose 30.2% -- and the Midwest -- which was up 17.9%.

The top chart shows the NE region, which has increased 2 consecutive months and currently stands at a 5-year high. The Midwest number is still within recently reported numbers.

While homes are expensive, mortgage rates are still fairly low:

This was a very encouraging report.

Monday, November 27, 2017

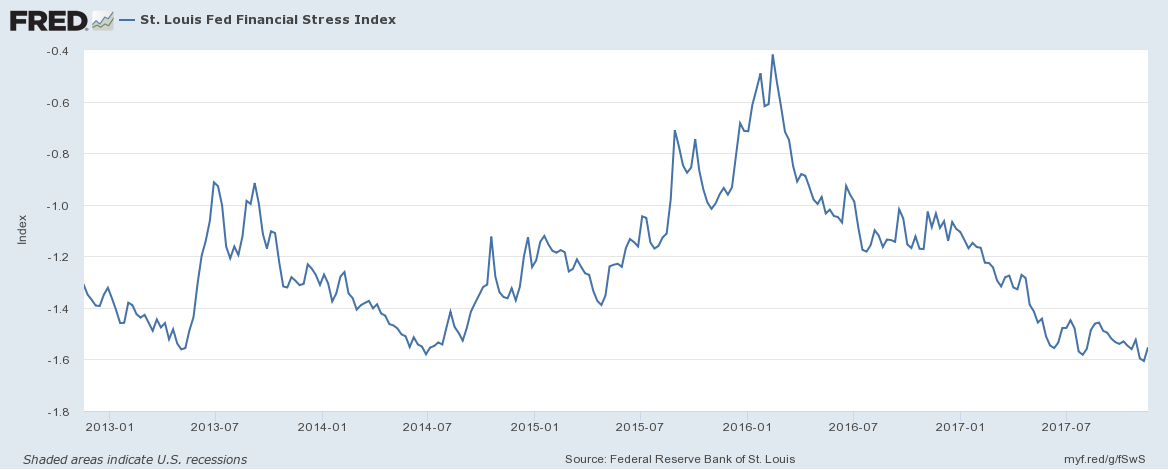

Monday Morning Credit Market Round Up

From October 23 to November 15, the CCC yields widened out nearly 100 basis points, rising from 10.19% to 11.09%. The BBBs also increased, but not by the same magnitude. They rose 11 basis points between October 23 and mid-November. The Baa's saw no increase, meaning the problems in the junk bond market were contained.

The St. Louis Financial Stress Index -- which is similar to the Kansas City number but is issued weekly instead of monthly -- is showing very little stress

The 90-day commercial paper treasury bill spread has widened a bit, rising o 19 basis points. But it was higher a year ago. This bears watching but is not concerning yet.

In contrast, the short-term asset-backed market has maintained its current short-term spread (top chart) or has come in a bit (bottom chart).

Finally, the 10-year FF spread has widened about 30 basis points since the beginning of September while the 30 year FF rate has been stable.

Sunday, November 26, 2017

I am so thankful that I am an economic blogger

- by New Deal democrat

A few days late for Thanksgiving, but ... like a lot of people, I woke up to a real nightmare one year ago. One decision I made for mental health purposes was to focus like a laser beam on the economy rather than have my blood boil over each day by each new atrocity.

In the last few months it has occurred to me over and over to be extremely thankful that I am writing about the one aspect of America that isn't going straight to hell.

Subscribe to:

Posts (Atom)