A government takeover of one or both companies is among several options that have been considered by White House officials, according to a person familiar with the discussions who spoke on condition of anonymity. Senior Bush administration officials are considering placing either or both firms in a conservatorship if their problems get worse, the person said.

The companies, which own or guarantee about half of the $12 trillion of U.S. mortgages, can count on a federal lifeline, said Republican Senator John McCain, and Democratic Senator Charles Schumer. Fannie Mae and Freddie Mac would have to post pretax losses and writedowns of about $77 billion before the U.S. would be compelled to start a rescue, according to estimates by Fox-Pitt Kelton and Friedman, Billings, Ramsey & Co.

``They must not fail,'' McCain, of Arizona, said yesterday during a campaign stop in Belleville, Michigan. Fannie Mae and Freddie Mac ``are vital to Americans' ability to own their own homes,'' he said at an earlier stop in the state, one of the worst affected by the surge in foreclosures.

From today's WSJ:

"They need a lot more capital," said John Paulson, who heads the hedge-fund manager Paulson & Co. that has made billions betting the housing market would decline. He pointed to "growing worries" about the deterioration of securities backed by mortgages as more homeowners default and home prices fall. Meanwhile, some high-profile bond investors snapped up Fannie and Freddie debt, believing the government would never allow them to default.

.....

"Fannie Mae and Freddie Mac are too important to go under," said Democratic Sen. Charles Schumer of New York. "...If they need additional support, Congress will act quickly." But he added in an interview: "We're not at that stage. I hope and think it won't be needed."

A Treasury spokeswoman said: "As Secretary Paulson said today, we're not going to speculate about 'what ifs' on Fannie and Freddie. What we're focused on is legislative reform."

Marketwatch adds:

The Times said the administration also considered calling for legislation that provide an explicit government guarantee on the $5 trillion of debt owned or guaranteed by Fannie and Freddie. Such a move was seen as an unattractive option, however, because it would double the size of the public debt.

In addition, three options were suggested in the WSJ article:

In an email sent to clients Thursday morning, Beth Hammack, who heads trading in Fannie and Freddie debt at Goldman Sachs Group Inc., said she sees "many good options" falling short of the government taking over the companies. Among them, she said, would be a purchase by the Fed of some of their debt or mortgage-backed securities. A spokesman for Goldman, which is advising Freddie on possible ways to raise capital, said the views were Ms. Hammack's and not necessarily those of the firm.

If things get bad enough, said Bob Napoli, an analyst at the securities firm Piper Jaffray & Co., the Federal Reserve could make large, 10-year loans to the companies "to make it clear that they have enough capital."

.....

Other possibilities might include the Treasury buying stock in the companies. In an extreme situation, the government might have to take over the companies in a transaction that might leave little or nothing for existing shareholders.

Option 1 (from the Marketwatch article) is a bail-out, but one that is a bit sly. The government is saying "we'll provide funding if X happens". However, my guess is the possibility of X happening is pretty high.

Option 2 (from the WSJ) is a bail-out of the direct kind, meaning one company takes on the distressed assets of another company.

Option 3 is an indirect bail-out with the Federal Reserve guaranteeing a steady supply of capital until the housing market recovered.

Option 4 is a corporate reorganization, plain and simple where company 1 buys a percentage of the stock of the second company.

Either option is a bail-out, make no mistake about it.

Now a bit of history.

First -- what exactly do these companies do? Basically, they provide liquidity to the mortgage market. The best way to explain this is to compare the mortgage market of 100 years ago and today. 100 years ago, you would go to your local banker and get a loan. If the banker thought you were credit worthy, you'd get a 30 year home mortgage. However, back then the bank would most likely own the mortgage for the entire life of the mortgage.

Fast forward to today. Banks don't keep loans on their books. Instead they sell them to investment banks, who then pool the mortgages into bonds -- either pass-through bonds or collateralized mortgage obligations (or CMOs). These in turn are sold to large, institutional investors like insurance companies, mutual funds etc...

Freddie and Fannie are quasi-public entities, meaning they have government charters but also raise capital from the private sector. In fact, many people who participate in the mortgage market have often felt that Freddie and Fannie have an unfair advantage because of their implied government backing. For years both institutions have said "no, we're not backed by the government." Now we know that's not true. Actually, we've always know that, it's just that now we really know.

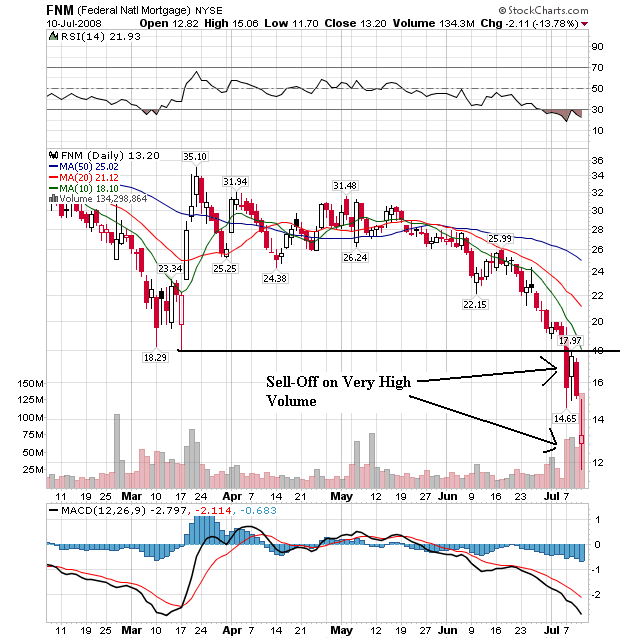

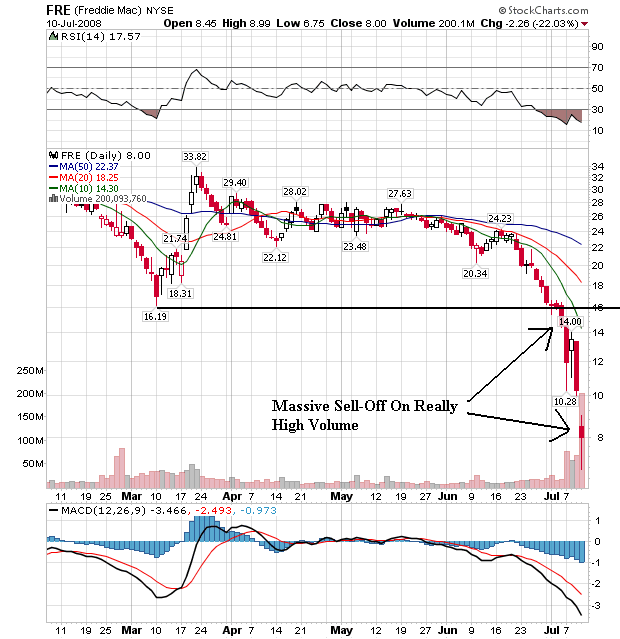

Let's take a look at the charts.

Both charts say the same thing:

-- Prices are below all the SMAs

-- The shorter SMAs are below the longer SMAs

-- All the SMAs are heading lower

-- Prices are below the 200 day SMA

In addition, over the last few days both charts have fallen through major support on extremely heavy volume. Traders are dumping the stock as fast as they can. That should tell you something.

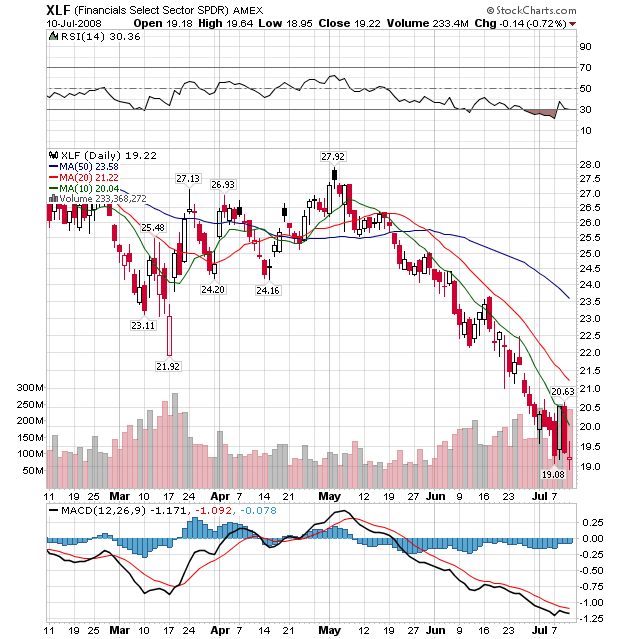

And this continues the downward saga of the financial sector in general:

Note the following:

-- Prices are below all the SMAs

-- The shorter SMAs are below the longer SMAs

-- All the SMAs are heading lower

-- Prices are below the 200 day SMA