It's also important to remember the Fed is as much a political player as it is an economic player. While a completely honest Fed would be great it is not going to happen. The Fed has to help manage the public's economic expectations. As such, it has to ease the public into a certain economic frame of reference. This is why yesterday was the first time we heard the Fed use the word "recession". The Fed has been aware of the economic situation for some time. But if they had come out and said "we're in a recession and it's really going to suck" they would have induced panic.

Here are the relevant portions of his testimony along with commentary.

Although our recent actions appear to have helped stabilize the situation somewhat, financial markets remain under considerable stress. Pressures in short-term bank funding markets, which had abated somewhat beginning late last year, have increased once again. Many lenders have been reluctant to provide credit to counterparties, especially leveraged investors, and have increased the amount of collateral they require to back short-term security financing agreements. To meet those demands, investors have reduced their leverage and liquidated holdings of securities, putting further downward pressure on security prices.

Credit availability has also been restricted because some large financial institutions, including some commercial and investment banks and the government-sponsored enterprises (GSEs), have reported substantial losses and writedowns, reducing their available capital. Several of these firms have been able to raise fresh capital to offset at least some of those losses, and others are in the process of doing so. However, financial institutions’ balance sheets have also expanded, as banks and other institutions have taken on their balance sheets various assets that can no longer be financed on a standalone basis. Thus, the capacity and willingness of some large institutions to extend new credit remains limited.

The effects of the financial strains on credit cost and availability have become increasingly evident, with some portions of the system that had previously escaped the worst of the turmoil--such as the markets for municipal bonds and student loans--having been affected. Another market that had previously been largely exempt from disruptions was that for mortgage-backed securities (MBS) issued by government agencies. However, beginning in mid-February, worsening liquidity conditions and reports of losses at the GSEs, Fannie Mae and Freddie Mac, caused the spread of agency MBS yields over the yields on comparable Treasury securities to rise sharply. Together with the increased fees imposed by the GSEs, the rise in this spread resulted in higher interest rates on conforming mortgages. More recently, agency MBS spreads and conforming mortgage rates have retraced part of this increase, and conforming mortgages continue to be readily available to households. However, for the most part, the nonconforming segment of the mortgage market continues to function poorly.

In corporate debt markets, yields and spreads on both investment-grade and speculative-grade corporate bonds rose through mid-March before falling more recently. Issuance of investment-grade bonds by both financial and nonfinancial corporations has been quite robust so far this year, but issuance of new high-yield debt has stalled. Strains continue to be evident in the commercial paper market as well, where risk spreads remain elevated and the quantity of commercial paper outstanding, particularly asset-backed paper, has decreased. Commercial and industrial loans at banks grew in January and February, but at a considerably slower pace than in previous months.

This set of paragraphs outlines the central problem faced by the markets, so let's take it slowly to see what is happening.

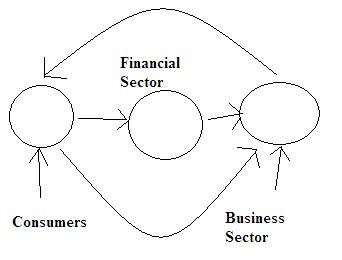

Let's start with this basic picture of the US economy.

The financial system stands at the center of the US economy; it takes savings from the public, pools it, and then lends it to business. It also stands between businesses because the financial system provides credit to buy literally everything in the economy. In other words, without a ready source of rapidly available credit the US economy drags to a halt.

And that's where the real rub comes in. For the last 9 months we have heard a continuing drum beat of news from the financial sector that banks are "writing down" the value of assets. The reason why this is so detrimental is the US financial system uses a "fractional reserve" banking system. All this means is a bank can loan out a certain percentage of its assets. For example -- and purely hypothetically -- if a bank has $1 million dollars in assets it could make loans of say $5 million. But as the bank's total assets decrease from a bunch of writedowns the bank's ability to make loans decreases. And that's where the bug problem comes in.

All of these writedwons we've been hearing about have the following negative impact.

-- Because of the just discussed fractional reserve system, the ability of banks to make loans is seriously compromised. As a result, there are fewer loans available.

-- Because of the breadth of the writedown news (literally everyone and their brother has announced problems) banks are unwilling to lend to each other. Why? Because even in the short-term market of commercial paper (which has a maximum maturity of 270 days) the possibility of the borrower announcing they have to writedown the value of their assets is high. This means the possibility of a borrower saying "we can't repay the loan" is much higher, leading to a drop in the total amount of loans being made. It also means the cost of short-term funding is increasing. Here is a chart of the commercial paper spreads from the Federal Reserve

Those spikes indicate risk is increasing. Here is a chart of total commercial paper outstanding. Pay attention to the yellow line

There's been a huge drop in the amount of commercial paper outstanding.

Putting all of these factors together we get a very disturbing picture. Because of all the writedowns in the financial sector the ability of financial players to make loans is seriously hampered. In addition, because of the increased fear of borrowers announcing they have writedowns to make, there are fewer short-term loans being written. As a result, the amount of short-term credit is decreasing and the cost of making these loans is increasing. This slows the US economy.

Notably, in the housing market, sales of both new and existing homes have generally continued weak, partly as a result of the reduced availability of mortgage credit, and home prices have continued to fall.1 Starts of new single-family homes declined an additional 7 percent in February, bringing the cumulative decline since the early 2006 peak in single-family starts to more than 60 percent. Residential construction is likely to contract somewhat further in coming quarters as builders try to reduce their high inventories of unsold new homes.

I've written about why the housing market is nowhere near bottom. Short version: there's a ton of supply combined with an already massively indebted US consumer decreasing demand. Let's not forget tightening credit markets limiting credit. The only way for this imbalance to be cured is for prices to drop hard.

Private payroll employment fell 101,000 in February, after two months of smaller job losses, with job cuts in construction and closely related industries accounting for a significant share of the decline. But the demand for labor has also moderated recently in other industries, such as business services and retail trade, and manufacturing employment has continued on its downward trend. Meanwhile, claims for unemployment insurance have risen somewhat on balance, and surveys indicate that employers have scaled back hiring plans and that jobseekers are experiencing greater difficulties finding work. The unemployment rate edged down in February and remains at a relatively low level; however, in light of the sluggishness of economic activity and other indicators of a softer labor market, I expect it to move somewhat higher in coming months

Here are the relevant charts:

The year-over-year change in payroll growth has been slowing substantially and is now in negative territory.

The unemployment rate is ticking up.

Short version: the job market is in terrible shape.

This is leading to declining consumer confidence and sentiment:

Which will further lower spending.

After rising at an annual rate of about 3 percent over the first three quarters of last year, real disposable income has since increased at only about a 1 percent annual rate, reflecting weaker employment conditions and higher prices for energy and food. Concerns about employment and income prospects, together with declining home values and tighter credit conditions, have caused consumer spending to decelerate considerably from the solid pace seen during the first three quarters of last year. I expect the tax rebates associated with the fiscal stimulus package recently passed by the Congress to provide some support to consumer spending in coming quarters.

Here are the relevant charts:

Remember the decreasing employment from above? That is leading to

Dropping income. When consumer's have less money to spend

Real (inflation-adjusted) personal consumption expenditures are decreasing.

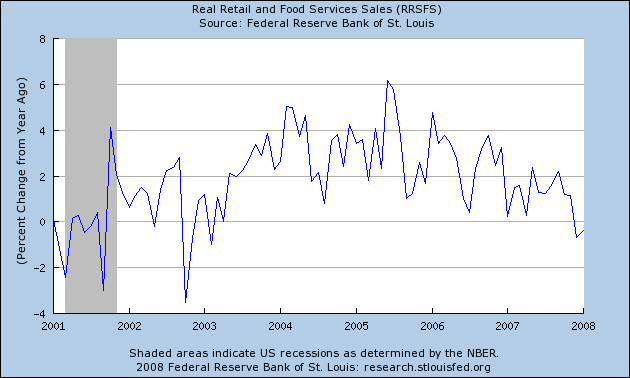

It also means that real (inflation-adjusted) retail sales are decreasing on a year-over-year basis.

In the business sector, the pullback in hiring that I noted earlier has been accompanied by some reduction in capital spending plans, as weaker sales prospects, tighter credit, and heightened uncertainty have made business leaders more cautious. On a more positive note, the nonfinancial business sector remains financially sound, with liquid balance sheets and low leverage ratios, and most firms have been able to avoid unwanted buildups in inventories. In addition, many businesses are enjoying strong demand from abroad. Although the prospects for foreign economic growth have diminished somewhat in recent months, net exports should continue to provide considerable support to U.S. economic activity in coming quarters.

Because consumers are cutting back on spending, businesses are cutting back on investment.

Durable goods year-over-year change has been negative for some time.

But the Philadelphia Fed survey is clearly weaker.

As is the empire state (New York) index.

Let's review:

-- There are big problems in the credit markets that aren't going away anytime soon.

-- Housing is still a mess.

-- Employment growth is decreasing

-- Real Disposable income is decreasing, leading to

-- Decreasing consumer spending, leading to

-- Lower business investment.