Retail sales decreased by 0.6%, the Commerce Department said Thursday. Sales went up a revised 0.4% in January. Sales that month were originally seen rising 0.3%. Sales in December dropped 0.7%.

Economists surveyed by Dow Jones Newswires estimated a 0.1% increase in February retail sales.

The sales report is a key indicator of U.S. consumer spending. Consumer spending makes up about 70% of gross domestic product, the broad measure of economic activity in the U.S.

High prices for gasoline, the credit crunch, falling home values and drops in other asset prices are seen as factors depressing spending. Another worrisome sign for spending -- and the economy -- is a soft job market. Non-farm payrolls declined by 63,000 jobs in February, the government reported last Friday, an omen that raised chatter about recession.

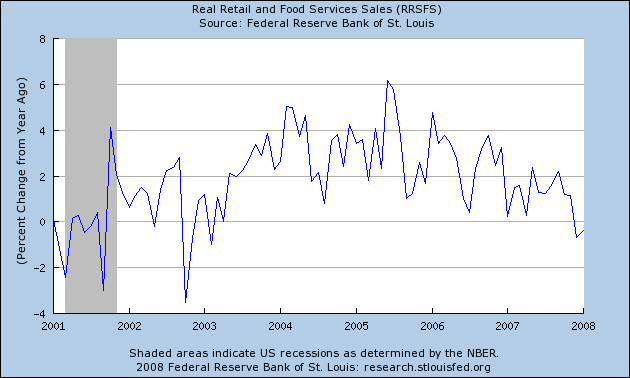

Above is a chart of real (inflation-adjusted) retail sales from the census bureau. Notice the clear downward sloping trend, indicating consumers have been backing away from the market for some time. Also note the year over year change moved into negative territory with yesterday's release.

Above is a chart of real personal consumption expenditures from the Bureau of Economic Analysis. This is a broader measure of spending -- it includes things like medical care, housing expenses etc.... This number was in a fairly constant range until roughly the end of last summer. Then it started dropping and has been dropping ever since.

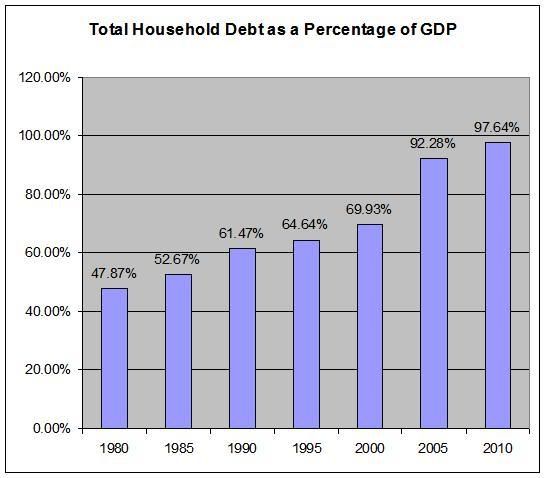

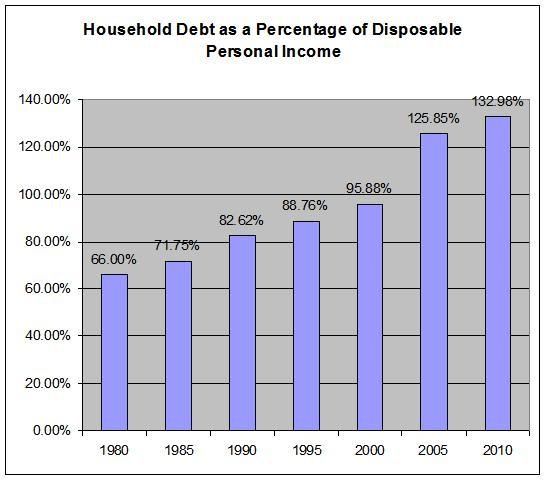

There are two charts that I use a great deal: consumer debt as a percentage of GDP and consumer debt as a percentage of disposable income. And here they are again:

Simply put, there is a ton of debt out there. And it appears it may be getting in the way.

I'm going to add two more charts to the mix. The first is from the blog Calculated Risk.

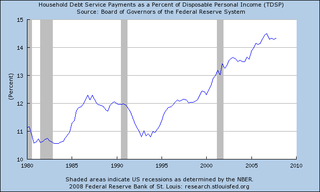

This is a calculation of the mortgage equity withdrawal using the Kennedy Greenspan method. It shows a clear drop in the amount of home equity consumers are pulling out of their homes. One reason may be the increasing percentage of debt payments as a percentage of disposable income:

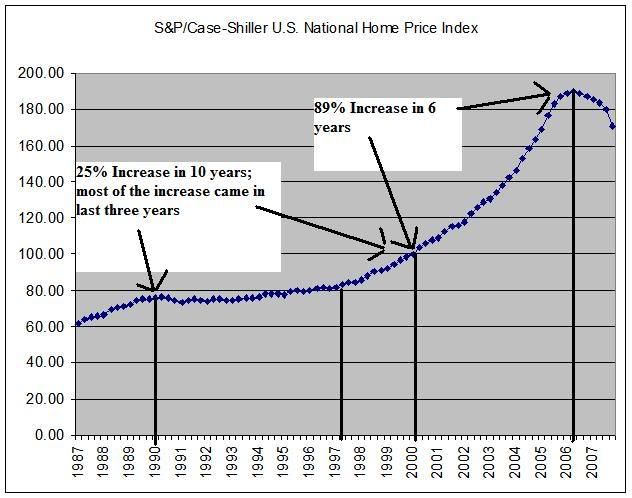

Another reason may be that home prices are dropping:

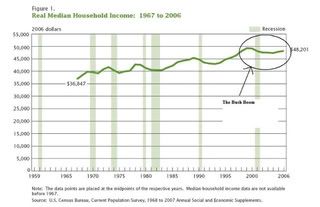

Regardless of the reason, the bottom line is people are clearly cutting back on thier debt acquisition. And considering incomes have been stagnant for quite some time:

People may simply be saying "I can't afford this" anymore.