"Main Street has just entered the act. The peak of the pain is not visible yet," said Asha Bangalore, an economist with Northern Trust in Chicago.

The consumer strains are well-documented. Aside from the credit contraction, gasoline and grocery prices are on the rise, the housing market remains distressed, and consumer confidence is at recessionary levels. Tax rebate checks are in the mail, but that alone cannot compensate for the credit clamp-down and inflation pressure.

"Given that households are strapped financially, it is far-fetched even with the stimulus checks to expect a sharp increase in consumer spending," Bangalore said. "You have seen auto sales numbers for April, they posted a sharp drop."

.....

To say that Wall Street is expecting a second-half recovery would be an understatement. According to Thomson Reuters research, analysts are expecting fourth-quarter earnings growth of 62 percent for the S&P 500. Granted, that is a comparison with a disastrous fourth quarter of 2007, when earnings were down some 25 percent. In the current quarter, S&P 500 earnings are expected to be down 6 percent.

Not only is the market anticipating a swift recovery, but the earnings forecasts suggest that they think it will be lasting. For next year, analysts think earnings will be up 18 percent, twice the growth they are predicting for 2008.

They see particularly strong growth for consumer discretionary companies, beginning with the next quarter. Earnings for that sector are expected to jump by 41 percent in the fourth quarter, and 24 percent next year.

The article focuses on the tightening credit situation in the market (which I dealt with here.) But I want to focus on a basic problem of the market rallying in the current economic environment.

Here's the fundamental question: will the economy rebound in the 2H 2008, proving the market right?" I have doubts for the following reasons.

First, let's start with the following charts:

Job growth is still dropping from a year over year perspective, and

The unemployment rate is still increasing

Real disposable income is decreasing, which is

Lowering sentiment and

Confidence

Year over year spending did increase in the latest report. However, note the following regarding that upturn.

-- in the latest GDP report, both durable and nondurable goods purchases decreased. The reason for the increase was an unseasonably high increase in service purchases.

-- One month does not a trend make especially in light of the preceding trend.

Also remember that inflation is high right now:

High inflation crimps consumer spending.

This is not to say that people won't increase their spending. But in light of declining job prospects, record oil and food prices and a slowing economy, it just doesn't seem like the consumer spending will increase in a big way anytime soon.

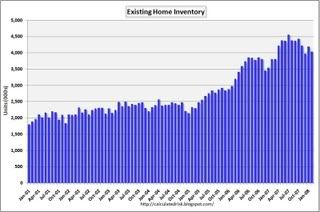

Then there is housing which started this mess. The inventory/demand situation is still horribly out-of-whack. From Calculated Risk, here is a chart of total existing homes on the market:

So -- we're at 4 million. And that number will increase because foreclosures are increasing in a big way -- they more than doubled in the first quarter. And it's not like we need all those homes -- not by a long shot. Home vacancies are now at a record.

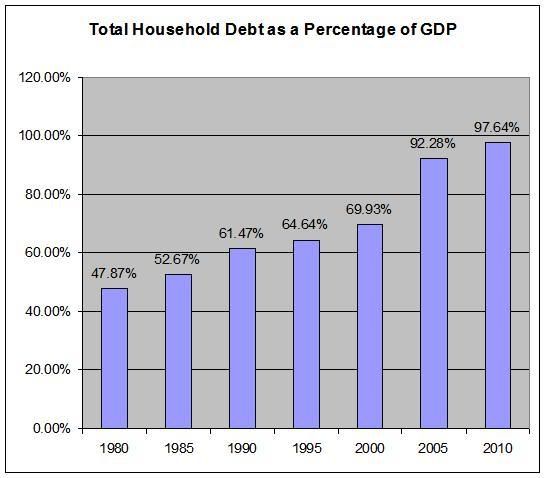

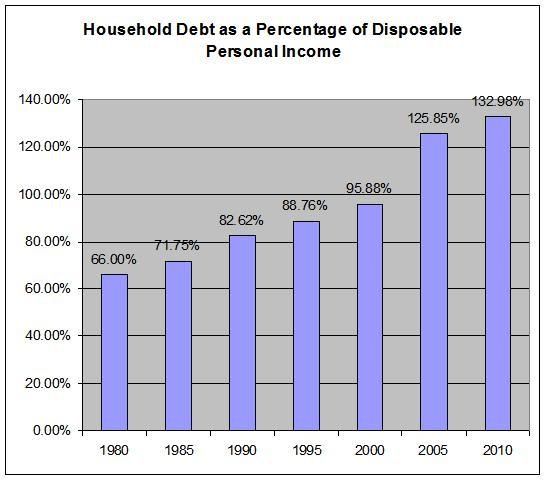

And who is going to buy these homes when credit conditions are tightening and consumers already have a record amount of debt?

So, according to the facts we have the following situation:

-- job growth is slowing

-- as is real income, which is

-- lowering consumer confidence and sentiment. In addition,

-- inflation is high, lowering spending.

-- Housing inventory is still high, and

-- rising foreclosures will increase that number.

-- Record levels of household debt and tightening lending standard will prevent a housing rebound.

Simply put, this is not a pretty picture for the second half of the year.