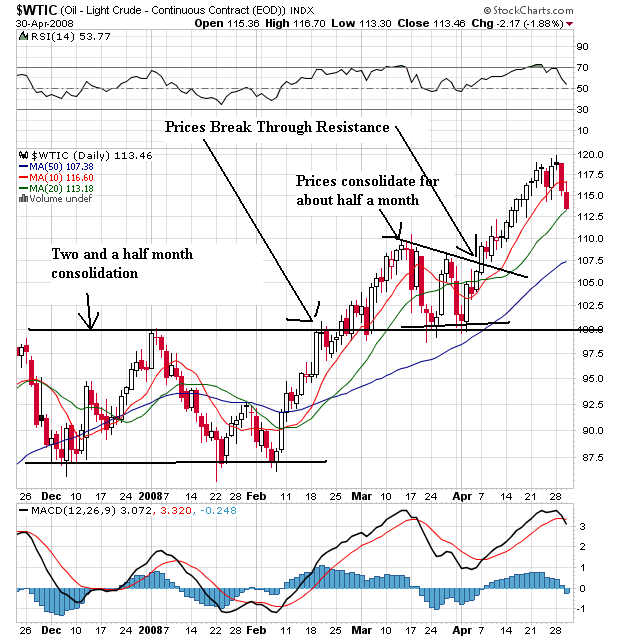

On the daily chart, notice the following:

-- Prices have twice broken through resistance to make new highs.

-- The shorter SMAs are above the longer SMAs

-- Prices are currently at the 20 day SMA. Prices have dropped through this number before and rallied again

-- Prices have consolidated their gains are each advance.

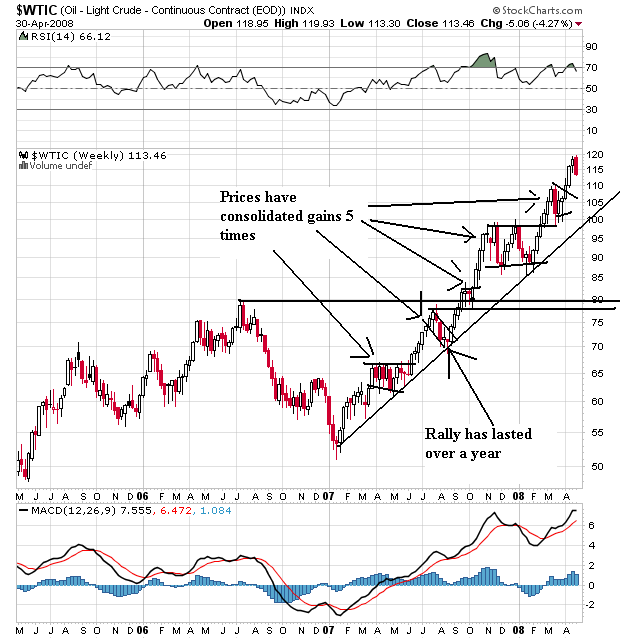

On the weekly chart, notice the following:

-- Prices have been advancing for over a year

-- After each advance prices have consolidated their gains

-- This is a very bullish chart

Although the oil market dropped last Wednesday, traders pointed to a weak dollar as a primary driver of the market:

``The weakness of the dollar is a great driver here,'' said Francisco Blanch, head of commodities research at Merrill Lynch & Co. in London. ``Oil has become a little bit of a monetary phenomenon, where low rates boost demand for oil in emerging markets.''

That theme continued intolast Thursday:

Crude oil fell more than $2 a barrel after the dollar rose the most against the euro since December, reducing the appeal of commodities to investors.

The dollar strengthened after a report showed German business confidence dropped more than expected in April. Commodity prices also fell because U.S. stocks rallied. Nigeria's white-collar oil workers union halted a partial strike that began earlier today at Exxon Mobil Corp.'s operations in the country, Reuters reported, citing a union official.

``You are seeing a move away from commodities because of the rally of the dollar and in equities,'' said John Kilduff, vice president of risk management at MF Global Ltd. in New York.

``The news from Nigeria is also helping a little bit but this is mostly about the dollar and equities.''

Crude oil for June delivery fell $2.24, or 1.9 percent, to settle at $116.06 a barrel at 2:47 p.m. on the New York Mercantile Exchange. Prices are up 80 percent from a year ago.

Oil reached a record $119.90 a barrel on April 22 after the dollar touched an all-time low against the euro. The euro fell 1.3 percent to $1.5676 per dollar at 3:14 p.m. in New York, from $1.5889 yesterday.

``The weak dollar has been the key driver of the reality in commodities,'' said Tom Bentz, a broker at BNP Paribas in New York. ``Lately there has been a direct correlation between the dollar and crude-oil prices, which hasn't always been the case.''

The dropping dollar has been a key reason for the spike in commodity prices. Commodities are denominated in dollars. Therefore, a dropping dollar is by definition a price decrease as well. Traders have to bid up the commodity just to tread water.

An oil strike on Monday helped to send the market higher.

BP PLC on Sunday shut down the Forties Pipeline System that carries more than 700,000 barrels of oil a day to the U.K. because of a 48-hour walkout by employees at a refinery in central Scotland. Workers walked out of the Grangemouth refinery vowing not to give ground in their dispute with refinery owner Ineos over plans to close a generous pension scheme to new employees. Ineos Chief Executive Tom Crotty said it could take a week for the plant to return to production once the strike ends on Tuesday. BP said its pipeline could be up and running within 24 hours. BP's Kinneil plant, the onshore processing center for the pipeline system, is powered from the Grangemouth site.

"With the refinery being shut down, it will affect supplies from the North Sea and that has a potentially significant impact," said David Moore, a commodity strategist with the Commonwealth Bank of Australia in Sydney. "That comes at the same time that there's production disruptions from Nigeria. So the combined effect of those is the immediate factor that's put pressure on oil prices."

In Nigeria, the Movement for the Emancipation of the Niger Delta, or MEND, on Friday said its fighters hit an oil pipeline late Thursday, the fourth conduit the group has attacked in the past week. MEND said the pipeline belongs to a Royal Dutch Shell PLC joint venture. A Shell spokesman confirmed one of its pipelines had been hit, but provided no additional details.

Separately, workers at an ExxonMobil Corp. joint venture in Nigeria cut production by an unspecified amount to demand more pay.

The strike in the British Isles led to some of the highest prices of all time:

Crude-oil futures closed slightly higher Monday after hitting a new record near $120 a barrel, as a strike at Scottish refinery forced a pipeline closure, while rebel attacks in Nigeria and tension in Persian Gulf also fanned concerns about supply disruptions.

Crude oil for June delivery climbed more than $1 to a new high of $119.93 a barrel in overnight electronic trading, surpassing the previous high of $119.90 hit last week. It ended up 23 cents, or 0.2%, at $118.75 a barrel on the New York Mercantile Exchange.

The gains were driven by supply concerns after hundreds of oil workers at Ineos PLC's Grangemouth refinery started a two-day strike Sunday, forcing the closure of a BP -operated pipeline which transports 700,000 barrels of oil a day, or about 40% of the U.K.'s daily crude production.

The strike ended on Tuesday.

On Wednesday, Goldman Sachs said the window for oil dropping on Spring weakness was "closing fast"

Goldman Sachs Group Inc., the most profitable Wall Street bank, said the window for a decline in oil this spring is `closing fast,' as prices rise to records and the summer period of peak gasoline demand approaches.

U.S. crude imports are likely to rise because of lower inventories and the strength of local oil prices relative to the rest of the world, Goldman analysts led by Giovanni Serio said in their Energy Weekly report.

``Looking into the second half of this year, given the fundamental tightness, we believe the risks are substantially skewed to the upside,'' the report said.

The central issue here is there is a ton of money flowing into the oil market right now; it's the latest boom area of the market. And so long as that situation continues, we'll be experiencing high oil prices.

Goldman isn't the only grop that thinks oiloil will keep rallying for a long time:

Surging crude prices, which could surpass $200 a barrel in four years on tight supplies, could push gasoline prices to as high as $7 a gallon, CIBC World Markets analysts said Thursday.

Crude supplies are actually lower than some official estimates indicate, while demand is unlikely to fall anytime soon, according to a statement by analysts led by Jeff Rubin at CIBC, an investment bank. They forecast that these tighter supplies and continued strong demand will drive oil and gasoline prices to roughly double their current levels by 2012.

"It is increasingly clear that the outlook for oil supply signals a period of unprecedented scarcity," said Rubin. "Despite the recent record jump in oil prices, oil prices will continue to rise steadily over the next five years."

Oil's increase in price is the most important of the last 30 years:

Demand in China continues to fuel demand, along with flare-ups in oil-exporting nations and a weaker dollar. But U.S. demand, after rising for years, is not a key contributor, Alliance Bernstein economist Joseph Carson says today in a note to clients. Domestic oil demand has dropped 1.6% over the last year as the economy weakens. He calls a price increase due to non-domestic factors “an exogenous shock, similar to to the supply shortages of the mid-1970s, early 1980s and briefly in the early 1990s.”

With the price shock of 2007-08, spending on energy as a share of wage income has shot up above 6%, topping the 1974-75 and 1990-91 shocks to be the worst since the 1980-81 runup. Comparing the additional cost of energy to income growth (especially sluggish in recent years), the current shock is far worse than any of the three prior ones, Mr. Carson says.

The figures “suggest that energy costs will crowd out other spending components because income growth is being stifled by weakness in payroll employment,” he writes. “Moreover, relatively thin saving flows offer consumers little cushion against the rising oil prices.”

Finally, yesterday's This Week in Petroleum report showed retail prices are still spiking.

For the fifth consecutive week, the U.S. average retail price for regular gasoline moved higher, reaching yet another all-time high price of 360.3 cents per gallon. The average price has spiked 21.4 cents since April 14. On a regional basis, while prices increased throughout the country, they did so at a somewhat slower pace than was the case during the previous week. The largest increase occurred on the East Coast where the average price jumped by 11.7 cents to 360.1 cents per gallon. This was the only region of the country to experience an increase greater than 10 cents. The price in the Midwest increased by 9.8 cents to 356.8 cents per gallon, up by 64.3 cents from a year earlier. The average price in the Gulf Coast was up by 9.4 cents to 350.5 cents per gallon. The average price in the Rocky Mountains, the lowest of any region, rose to 347.8 cents per gallon, up 6.2 cents from the previous week. Once again, the West Coast average price increased the least of any region, moving up by 5.2 cents to 378.6 cents per gallon. Nonetheless, despite the relatively small increase, the average price was the highest of any region. The average price in California increased by 4.6 cents to hit 389.2 cents per gallon.

Short version: The only bearish news of the week was a possible pause in the Fed's interest rate policy of lowering rates. That should help the dollar rise in value which should lead to a drop in oil prices. Hopefully. However, there are plenty of fundamental drivers to the demand side of the oil market right now, starting with China and India.