- by New Deal democratThe big monthly number was yesterday's employment report, showing 120,000 jobs added to the economy in November. September and October were also revised up by a total of 72,000, conintuing the string of upward revisions. The household survey was even more impressive, up 278,000 jobs. The last 4 months in this survey have shown gains averaging 321,000 a month. Unemployment declined to 8.6%, the lowest since March 2009. Only half of the 0.4 decline was due to participants leaving the workforce, as to which the phrase "retiring baby boomers" assumes ever-increasing importance. Two important internals were weak: manufacturing hours, one of the 10 LEI, declined by .2. Wages actually decreased by $.02 continuing the ominous real wage deflation of this year.

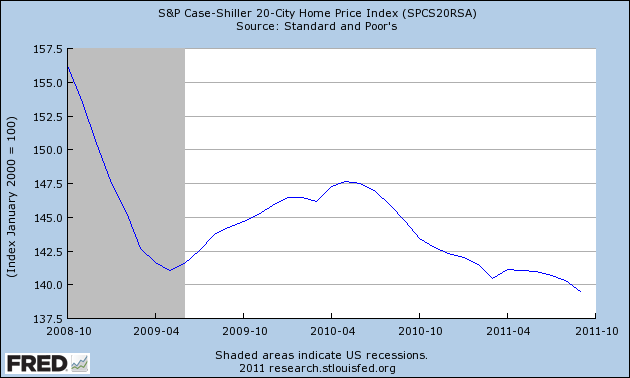

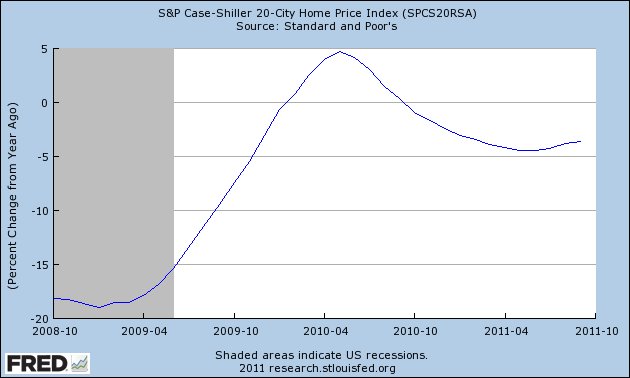

In other monthly news, manufacturing improved (although vendor deliveries, another of the LEI, decreased). Auto sales were up, and at their strongest level ex cash for clunkers since August 2008. Consumer confidence rebounded strongly, taking back over half of its decline since the end of June. New home sales were flat, and the Case-Shiller index of home prices declined more than expected, althought its YoY% decline continues to lessen.

Before turning to the high frequency weakly data, let me remind new readers that this post is not designed to be a "big picture" look at the economy. Quite the reverse: if we think of the economy like a motion picture with 24 frames per second, this post compares the most recent frame with the frame just preceding. In other words, it is a snapshot of as close as we can get to the present moment. Before any change in direction in monthly data is confirmed by two successive reports, there will be at least 8 weekly datapoints, which will show the change first.

Let's start with the small sea-change in housing. For the first time since the inception of the series over 4 1/2 years ago, YoY weekly median asking house prices from 54 metropolitan areas at

Housing Tracker were positive, up +0.1% YoY for the last full week of November. The areas with YoY% increases in price decreased by 1 to 20. Only Chicago continued to have a double-digit YoY% decline. The monthly number for all of November was still down -0.7% YoY, which is still the smallest monthly YoY decline since the series began. Housing Tracker's asking prices have generally led sales prices at turning points and in the second derivative by 4 to 6 months over the history of the series, so this suggests that the Case-Shiller index YoY decrease will continue to lessen in coming months, and may turn positive nominally by next summer.

Meanwhile, the

Mortgage Bankers' Association reported that seasonally adjusted purchase mortgage applications decreased -0.5% last week. On a YoY basis, purchase applications were down -8.2%. This primarily reflects a multi-week spike last year vs. flatness this year. The actual reading remains firmly within the range that purchase mortgage applications have been in since May 2010. Refinancing fell -15.3% w/w. Refinancing continues to be extremely volatile.

Turning to jobs, the

BLS reported that Initial jobless claims rose 9000 to 402,000. This is 14,000 above the 388,000 low of 2 weeks ago. The four week average rose 1500 to 395,750.

The

American Staffing Association Index remained at 92 last week. This series continues its slight upward trajectory, but remains slightly below last year's levels.

Tax withholding for the 20 reporting days of November was significantly down from last year's levels. Adjusting +1.07% due to the 2011 tax compromise, the

Daily Treasury Statement showed that for this November, $135.5 B was collected vs. $138.9 B a year ago, a decline of -2.4 B. Before concluding that the economy has suddenly weakened, however, note that this November began on a Tuesday whereas November 2010 began on a Monday. That means that this November only had 4 Mondays vs. last November's 5. Tax collections are typically stronger on Mondays and much stronger on the first of the month. Usually the 20 day moving average takes care of that issue (4 x each weekday), but because of holidays in November, that didn't apply. When I correct for this by measuring 20 days beginning Monday October 31, 2011 or Tuesday November 2, 2010, the anomaly disappears, and tax collections for the 20 day period are up $1.8 B or $1.7 B respectively, or about +1.3% YoY.

Retail same store sales remained positive as they have been all year. The

ICSC reported that same store sales for the week of November 26 increased 4.0% YoY, and 1.7% week over week.

Shoppertrak reported that YoY sales rose 4.4% YoY.

The

American Association of Railroads reported that total carloads increased 3.9% YoY, up about 17,000 carloads YoY to 456,200. Intermodal traffic (a proxy for imports and exports) was up 6700 carloads, or 3.7% YoY. The remaining baseline plus cyclical traffic increased 10,200 carloads or 4.0% YoY. Total rail traffic has staged an impressive rebound in the last couple of months.

Money supply continues to stabilize after its Euro crisis induced tsunami. M1 decreased -0.5% last week, and is up a slight 0.2% month over month. It remains up 18.7% YoY, so

Real M1 remains up 15.1%. This is about 5% under its peak YoY gain several months ago. M2 also decreased -0.4% w/w. It remained up 0.3% m/m, and 9.4% YoY, so

Real M2 was up 5.8%.

Weekly

BAA commercial bond rates declined .05% to 5.11%. Yields on 10 year treasury bonds fell even more, down .08% to 1.94%. In the last couple of weeks, spreads have started to widen again, representing increasing weakness.

Finally, the Oil choke collar is tightening, as

Oil closed just below $101 a barrel on Friday. This about $6 above the recession-trigger level calculated by analyst Steve Kopits. Gas at the pump, however, decreased $.06 to $3.31 a gallon. Measured this way, we probably are only about $.05 to $.10 above the 2008 recession trigger level. Gasoline usage was off YoY, but by considerably less, at 8769 M gallons vs. 8867 M a year ago, or -1.1%. The 4 week moving average is off -2.9%, which is also less of a decline compared with recent weeks.

With the vital exception of real wage deflation, the picture now is very similar to that of a year ago. Having dodged a double-dip recession, the economy then showed signs of becoming a self-sustaining recovery, only to be strangled by the Oil choke collar (with an assist by the tsunami in Japan) in March. It looks like we've dodged another bullet, but the Oil choke collar is tightening again.

Have a nice weekend.