Lakshman Achuthan's loud reiteration of ECRI's recession call last week, especially in the face of recent positive economic surprises, certainly has commanded attention. ECRI has an impressive record, especially their incredibly gutsy call in the midst of economic freefall in March 2009 that the "great recession" would bottom that summer. It did.

But ECRI's forecasts are surrounded by suspicion because of its (understandable) lack of transparency. The elements of both the Long Leading Index and the Weekly Leading Index, which it apparently uses in tandem to make its forecasts, are understandably kept in the proverbial black box, otherwise how could it charge its subscribers?

While I claim no proprietary knowledge of any of ECRI's methods, its history, hints about what is and is not in the indexes that have been dropped over time, and some reverse engineering can give us a glimpse inside their black box. So, what is it that ECRI is seeing, that didn't just to make their recession call three months ago, but to stick with it despite signs of a recent rebound?

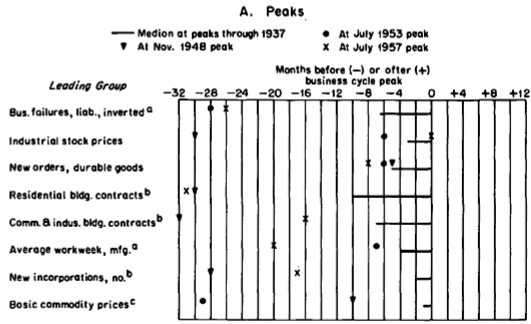

A good place to start is with the work of Prof. Geoffrey Moore. ECRI was founded by him, and is based on decades of work on economic indicators he performed while at Columbia University. While some of his indicators apparently did change over time, we do know that he believed that some persisted from well before World War 2. As a reminder, here is a chart he himself published in 1961 explaining a number of leading indicators that functioned equally well borth before and after the War:

The above graph and the information contained in Moore's article make it fairly clear that he leaned heavily towards manufacturing and commodity data in his index.

Since stock prices were one of the leading components of his work, let's start with those. Here is a graph of the S&P 500 for the last 12 months:

Stocks fell 20% in August, and have only regained about 1/2 of that loss since then. They are still below their level of 6 months ago. John Hussman apparently relies in part on this metric as well in making his recession call.

If our stock market is below where it was 6 months ago, those of two of our trading partners are even worse. Here's a one year graph of Europe:

And here's a three year graph of China:

Europe isn't even half the way back from its low to its 12 month high. It's down about 30% from that peak. China is even worse. The Shanghai stock market has generally been in a downtrend for the last 2+ years, and Shanghai appears to be the stock market that now leads the rest of the world. These suggest that our economy will continue to import weakness from both of these sources.

Based on Moore's graph above, and based on its proven long leading relationship, another component of ECRI's long leading index is likely to be housing. According to work done by Prof. Edward Leamer, housing appears to turn about 12 to 15 months before the top of the business cycle. While housing permits have recently turned up mildly (red below), here is what they looked like 12 months ago (blue):

The post housing credit nadir was in January of this year, meaning we can expect it to feed through into the first quarter or so of 2012 before abating.

Another item believed to be a part of ECRI's long leading index is corporate profits. Sure enough, when we take corporate profits, and adjust for inflation by using the PPI, corporate profits routinely top out about 1 year or so before the onset of recession, as shown in this graph:

While corporate profits rose in the 2nd and 3rd quarters, they are still below their 2010 post recession peak when adjusted for producer price inflation.

A comparison of commodity prices (red) vs. consumer price inflation (blue) is consistent with the idea that when companies are unable on a sustained basis to pass on increased costs to consumers, then companies cut back, commodity prices fall, and more than consumer prices which also fall as demand temporarily decreases. Once companies are able to profit again, the recession abates:

In past work I have found that in the case of deflationary busts (with at least 3 consecutive months of decreasing prices), the recession typically bottoms at the point where the YoY deflation rate reaches its nadir, as for example happened in June 2009:

Here is a bar graph showing GDP over the same period of time as the graph above. You can see that deflation typically occurs during or just after the slowdown as measured by GDP:

As the gasoline price spike of November 2010 through April 2011 is gradually replaced in YoY inflation statistics (as to which recall that Prof. James Hamilton of UCSD has found that increases in gas prices have their biggest effect on the economy 12 months later), we may be starting a brief period of monthly deflation in line with the deflationary periods shown above. This is consistent with the paradigm of corporate cutbacks in the face of declining profit margins. In this regard, Jeff Miller of A Dash of Insight worryingly tells us that forward corporate earning estimates have indeed stalled.

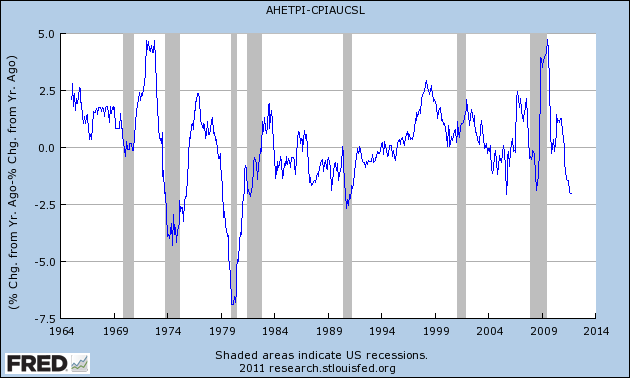

Further to this point, recently I have also noted that when real wages fail to keep up with consumer price inflation, in the absence of the ability to borrow or to refinance, consumers have little choice but to cut back. And real wages have indeed failed to keep up with consumer inflation in 2011:

The above discussion of corporate and consumer slowdowns brings us to commodity prices, another indicator cited by Prof. Moore as a short leading indicator. Here is Bloomberg's graph of commodity prices using various indexes for the last 12 months:

Measured by any index these peaked in about April and have generally been in decline since. Unlike other indexes which also plummeted this past summer, such as consumer confidence, commodity prices have continued to fall, again probably influenced by the deteriorating conditions in Europe and China. They made new 6 month lows shortly before ECRI made its official recession pronouncement, and have generally continued to fall since.

Another leading indicator cited by Prof. Moore that is somewhere between a short and long leading indicator is new orders for durable goods. A perfect example of this is auto sales. Again, while these have recently improved considerably (red), 6 months ago they were undergoing a temporary slump:

Finally, let's look at one last short leading indicator believed to form part of ECRI's index, credit spreads. As shown in this graph starting in 2000, credit spreads between BAA corporate bonds (blue) and 10 year treasury bonds (red) tend to widen just before and during recessions. Indeed, at least during the beginning part of a recession, business weakness may cause corporate bond yields to spike, while treasury yields decline given their status as a safe haven:

Here is a close up of the same data for the last 12 months:

As you can see, credit spreads began to widen in spring, and opened up much wider in August. Like commodity prices, they have not rebounded much at all since then.

To summarize: all of the above information grows out of the work of Prof. Geoffrey Moore, and/or interviews or statements that Lakshman Achuthan has made at one point or another. It represents a best guess as to what at least some of the data in their black box is showing ECRI. You can see that, taken together, it makes a very powerful bearish case for the onset of recession at some point probably no later than Q2 2012.

Am I persuaded? Not yet. Housing permits have indeed been in a small uptrend for the last 10 months, and car sales in a strong one for the last five. The Dow Jones Corporate Bond Index also continues to be in a small but definite uptrend. Consumer confidence is improving. Initial jobless claims are decreasing. YoY money supply, both M1 and M2, are also strongly positive. Manufacturing employment remains slightly positive.

Even more importantly, the decline in commodity prices, particularly oil, while showing weakness in Europe and Asia, is a boon to American consumers.

In short, three months after ECRI's recession call, I don't yet see weakness crossing either the Atlantic or the Pacific sufficiently to create a recession here.