As I've noted before, one thing I've learned from this recession is that it's not as easy to increase the money supply as I thought. It's easy to create additional bank reserves and increase the monetary base, but if the new reserves simply pile up in the banking system, then they don't have much of an effect on the supply of money:

More On Friedman/Japan, by Paul Krugman: ...So: David Wessel quoted what Milton Friedman said about Japan in 1998, and interpreted it as meaning that Friedman would favor quantitative easing now. I think that’s right. And just to be clear, I also favor QE — largely because it might help some, and seems to be just about the only policy lever still available in the face of political reality.But I think it’s also important to note that Friedman was all wrong about Japan — and that you can argue that he was also wrong about the Great Depression, for the same reason.

For what Friedman argued, both for Japan in the 1990s and America in the 1930s, was that all the central bank needed to do was more — push out those reserves into the banking system. This would raise the money supply, and a higher money supply would have the usual effects.

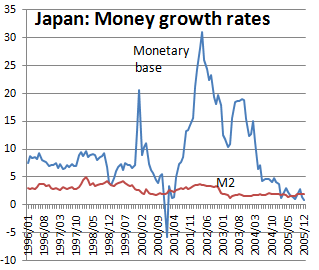

But the Bank of Japan tried that — and found that pushing more reserves into the banks didn’t even lead to rapid growth in the money supply, let alone end the problem of deflation. Here’s a chart of growth rates of the monetary base and of M2, Friedman’s preferred monetary aggregate:

Bank of JapanSo, after 2000 the Bank of Japan engineered a huge increase in the monetary base; this was the original quantitative easing. And it didn’t even translate into a surge in the money supply! This is why I’m so skeptical of people who say that all the Fed has to do is target higher nominal GDP growth — in liquidity trap conditions, the Fed doesn’t even control money, so how can you blithely assume that it controls GDP?

And this also calls very much into question Friedman’s famous claim that the Fed could easily have prevented the Depression, which gradually got transmuted into the claim that the Fed caused the Depression. Yes, M2 fell — but why should we believe that the Fed had any more control over M2 in the 30s than the BOJ had over M2 more recently?

Again, that doesn’t mean that I oppose having the Fed engage in unconventional asset purchases. I’m just trying to be realistic about the likely results. We really, really need expansionary fiscal policy along with Fed policy; and we’re not going to get it.

I have no problem with the policy idea or implementation. The bottom line is the economy needs some type of jump start. However, I don't think this will be a huge success, largely because people are de-leveraging right now and business can get a great deal from financing their debt on the open market.