- by New Deal democratAll things considered, I'd rather have been wrong yesterday when

I said that the jobs consensus was wrong, and to expect only a +50,000 nonfarm payrolls report. With the exception of the ISM services report, virtually every other report this week - ISM manufacturing, concumser confidence, construction spending, factory orders - hit an air pocket. Vendor supplies in the ISM (a leading indicator) will subtract about -.3 from that report. The manufacturing workweek (another component of the LEI) remained flat, and the household survey showed +105,000 jobs, reversing most of last month's loss, which for this week counts as a silver lining.

Turning to the high-frequency weekly indicators:Oil remained stubbornly above $100 a barrel late Friday. It still remains slightly above 4% of GDP. Gas at the pump fell for the second week in a row, declining $.06 more to $3.79 a gallon. Gasoline usage at 9431 M gallons was 2.8% higher than last year's 9174. This is the first positive YoY comparison in almost three months.

The

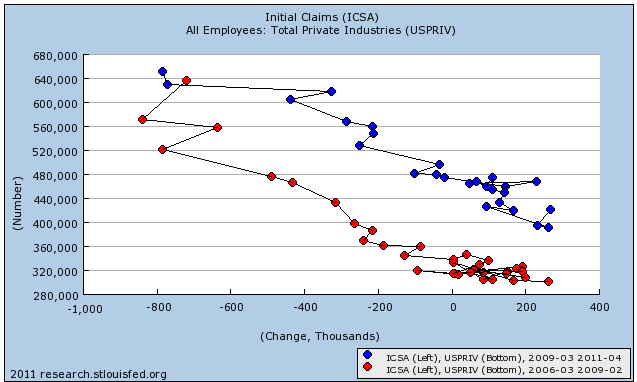

BLS reported that Initial jobless claims last week were 422,000. The four week average declined to 425,500. We are back at levels last seen late last autumn - but still significantly lower than the rest of last year - and likewise considerably higher from earlier this year.

Railfax was up 2.3% YoY for the week, or 17,600 carloads. The Baseline traffic 4 week moving average is virtually flat, up only 0.07% from a year ago. Cyclical traffic is up 4.25%. Intermodal traffic (a proxy for imports and exports) is 6.42% compared with a year ago.

The

Mortgage Bankers' Association reported that seasonally adjusted mortgage applications were flat last week. It was 7.6% higher than this week last year. The purchase series has now been generally flat for over a year, and this is the second week in a row that YoY comparisons in purchase mortgages were positive. Except for the rush at the two deadlines for the $8000 mortgage credit, these are the first YoY increases since 2007. Refinancing decreased 5.7% despite a continued decline in mortgage rates.

The

American Staffing Association Index remained at 94 for the third week. This advance continues to look very much like the first half of 2007 - slow growth, but not stalled.

The

ICSC reported that same store sales for the week of May 28 increased 2.8% YoY, and increased 0.4% week over week.

Shoppertrak reported a very strong 6.0% YoY increase for the week ending May 28 (the third strong week in a row) and a WoW increase of 3.0%. Weekly retail sales numbers have been a bright spot all year, generally showing the consumer not rolling over due to gas prices.

Weekly

BAA commercial bond rates decreased another .02% to 5.74%. This yields of 10 year treasury bond decreased .05% to 3.10%. The recent decline in treasury rates do show fear of deflation, and corporate rates have not declined so much, showing a slight increase in relative distress in the corporate market.

Adjusting +1.07% due to the 2011 tax compromise, the

Daily Treasury Statement showed that for May 2011, $140.1 B was collected vs. $126.8 B a year ago, for an increase of 11.7% YoY. For the last 20 days, $113.7 B was collected vs. $126.7 B a year ago, for an

decrease of $11.8 B, or -0.9%. Use this series with extra caution because the adjustment for the withholding tax compromise is only a best guess, and may be significantly incorrect. Last May was weak and had one fewer workday, so the monthly comparison isn't as great as it looks, and the last 20 days look abysmal.

M1 was up 0.9% w/w, up 1.5% m/m, and up 13.1% YoY, so

Real M1 was up 10.1%.

M2 was up 0.1% w/w, up 0.6% m/m, and up 5.1% YoY, so

Real M2 was up 2.0%.

Real M1 remains very bullish, while Real M2 remains stuck in the caution zone under 2.5%

Finally, since there is heightened scrutiny of the decline in housing prices recently, this week I am starting to report the weekly update of median asking house prices from over 50 metropolitan areas at

Housing Tracker. While a weighted mean would be the most accurate measure, the author of the site does not track that way. Thus I will report the YoY% median change for the areas, plus how many of the YoY% changes are positive, and how many show double-digit declines. I am very confident that when housing prices do bottom, this measure will be the first to show it, and in real time, just as it showed the peak in real time in 2006. This week the median YoY decline is -5.7%. Ten areas showed double-digit YoY% declines and 4 showed YoY% increases in price.

The slowdown is here, the stall is tapping on our shoulders, and the Doomers are close behind murmuring darkly about "green shoots" again. Their perfect record will probably remain intact. Please recuperate safely with the beverage or other vice of your choice this weekend!