From Bonddad: This is, without a doubt, one of the best pieces NDD has ever written. I agree 100% with his conclusions on the topic. While I'll be posting on this topic something later this week, NDD has provided a far more thorough and well-researched article.

There has been a secular shift in the American economy going back at least 4 years. The self-congratulatory "great moderation" was really the reflection of wage stagnation for the majority of Americans being masked by increased household debt loads, and the ability to carry those increased debt loads due to the ability to refinance them at lower and lower interest rates.

This secular shift is a phenomenon I first wrote about at great length in 2007, asking Are Hard Times Near? That pessimistic prediction has been answered in a thunderclap-like affirmative ever since. I have returned to this issue several times during the last four years, writing last year under similar circumstances to our present slowdown that wage stagnation was the greatest threat to the recovery.

Simply put, when there is only 1-2% wage growth per year, any inflationary spike - even a 3% spike due to energy increases - is enough to cause the economy to stall. There can be no long-term, sustained recovery for the large majority of Americans unless there is real, long-term wage growth. Thus, while at one level the current slowdown or stall is the result of an energy price shock, on another level it was predictable (and predicted by others and me) due to prices faced by consumers rising faster than their disposable incomes.

In summary, American consumers:

* have not had an increase in household wealth

* have been unable to refinance at lower interest rates for more than 3 years

* have been unable to tap into increased wealth via stock or house price appreciation above previous levels

* and have chosen instead to cut back significantly on debt (more than 1/2%)

only three times in the last 31 years: during the recessions of 1981-2, 1990-1, and the "great recession" of 2008-09.

This result can be easily seen by showing real, inflation-adjusted YoY hourly wages, and also the effect of declining vs. stalling interest rates.

Before looking at the graphs showing those long-term trends up until now, first let me show you what I said back in August 2007 on the cusp of the "great recession":

With the exception of the late 1990's tech boom, and those times in the last 10 years when energy prices briefly reversed, real hourly income has made no progress at all. The 1981-82, 1990, and 2008-09 recessions have all been accompanied by declines in real hourly income.

Simply put, when there is only 1-2% wage growth per year, any inflationary spike - even a 3% spike due to energy increases - is enough to cause the economy to stall. There can be no long-term, sustained recovery for the large majority of Americans unless there is real, long-term wage growth. Thus, while at one level the current slowdown or stall is the result of an energy price shock, on another level it was predictable (and predicted by others and me) due to prices faced by consumers rising faster than their disposable incomes.

In summary, American consumers:

* have not had an increase in household wealth

* have been unable to refinance at lower interest rates for more than 3 years

* have been unable to tap into increased wealth via stock or house price appreciation above previous levels

* and have chosen instead to cut back significantly on debt (more than 1/2%)

only three times in the last 31 years: during the recessions of 1981-2, 1990-1, and the "great recession" of 2008-09.

This result can be easily seen by showing real, inflation-adjusted YoY hourly wages, and also the effect of declining vs. stalling interest rates.

Before looking at the graphs showing those long-term trends up until now, first let me show you what I said back in August 2007 on the cusp of the "great recession":

The American consumer has had largely stagnant wages since 1974.... [F]rom 1980 through 2006, the median income of an American household has risen only from $39,700 to $48,200 in real terms .... Consumers have responded generally by taking on more and more debt. Total household debt service has risen from 16% in 1980 to 19.4% in 2006.

Fortunately for consumers, there has been a generation-long decline in interest rates since they peaked at 15.21% for the 30 year US Treasury bond in October 1981. This has allowed consumers to refinance their debts at ever lower rates every few years. They have also been assisted by a bull market in stocks that took the S & P 500 from 102 in 1982 to 1553 in 2000, and the subsequent housing boom/bubble.

There are signs that this "Great Disinflation" of declining interest rates is coming to an end. Only twice in the last 27 years has the consumer been unable to refinance debt or tap into his or her stock or house ATM.... [T]he 3rd and final time is almost certainly near.

.... If consumers are unable to tap the value of assets, or to refinance, then without improvements in wages, they will pull back and cause a consumer-led recession. Since 1980, this has only happened twice: in the deep Reagan recession of 1981-82, and again briefly from July 1990 to March 1991.

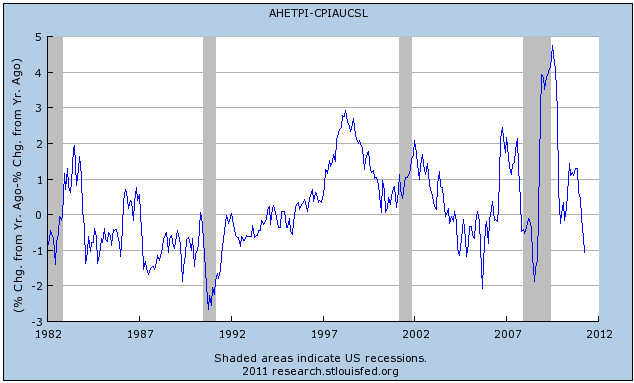

.... [T]he failure of interest rates to make new lows signifies that any continued deterioration in house prices, or significant and sustained decrease in stock prices, will likely give rise to an imminent recession danger sign.The YoY% change in real, inflation adjusted hourly earnings for the last 30 years is shown in this graph:

With the exception of the late 1990's tech boom, and those times in the last 10 years when energy prices briefly reversed, real hourly income has made no progress at all. The 1981-82, 1990, and 2008-09 recessions have all been accompanied by declines in real hourly income.

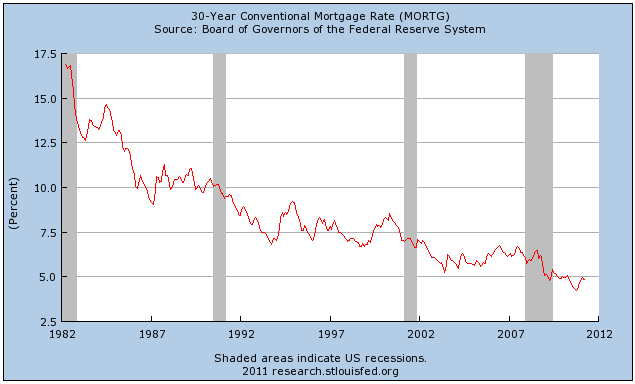

Now, let's show how mortgage rates have behaved since peaking in the early 1980's:

Notice that there has been a general 30 year long decline in rates, punctuated by stagnant rates in the late 1980s, most of the 1990s, and the housing bubble era.

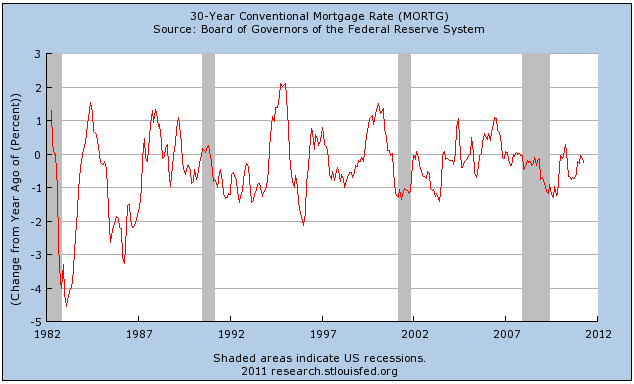

Here is a slighly different look, showing the year-over-year change in mortgage rates:

Now, let's put the two series together, showing real YoY% wage changes in blue, and YoY changes in mortgage rates in red:

This graph shows that stagnant or rising mortgage rates occurred at the same time as stagnant or declining real incomes (generally, when the red line is higher than the blue line in the graph above) during mid-cycle slowdowns at on the eve of or start of the post-1980 recessions. This was true by the end of 2007, it was true in last summer, and it has been true for the last few months.

Thus, only one month after the story quoted above, in September 2007, with new data showing that households were beginning to shun debt, it seemed clear that under the above criteria, consumers were signalling recession:

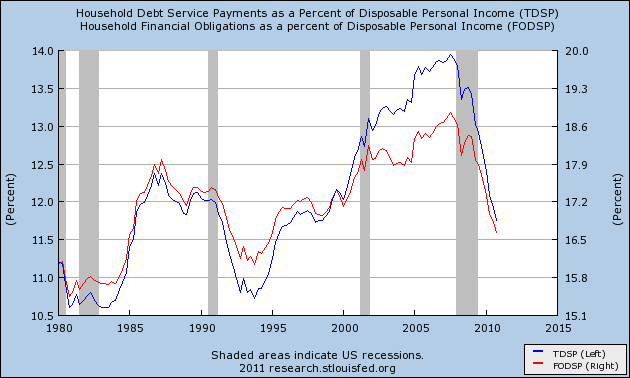

This was the final shoe to drop. Household debt deleveraging in the face of stagnant wages and the inability to refinance has been the harbinger of all post-1980 recessions. Here is how household deleveraging stands as of the last report (4Q 2010):

I revisited the issue of real wage growth as a necessity for sustained economic growth in May 2009 even as I foresaw the bottoming of the recession:

Notice that there has been a general 30 year long decline in rates, punctuated by stagnant rates in the late 1980s, most of the 1990s, and the housing bubble era.

Here is a slighly different look, showing the year-over-year change in mortgage rates:

Now, let's put the two series together, showing real YoY% wage changes in blue, and YoY changes in mortgage rates in red:

This graph shows that stagnant or rising mortgage rates occurred at the same time as stagnant or declining real incomes (generally, when the red line is higher than the blue line in the graph above) during mid-cycle slowdowns at on the eve of or start of the post-1980 recessions. This was true by the end of 2007, it was true in last summer, and it has been true for the last few months.

Thus, only one month after the story quoted above, in September 2007, with new data showing that households were beginning to shun debt, it seemed clear that under the above criteria, consumers were signalling recession:

In order to avoid a recession, house price declines must stop, stock market gains must accelerate, or household income must increase significantly. Failing at least one these three things, if households have continued to cut back on debt, as appears likely, America will probably enter (or may already have entered) only its 3rd consumer recession since 1980.

the indicators studied from the Deflationary period of 1920-1950 suggest that the GDP might stop contracting in about Q3 2009, and start to actually grow.Luckily, as shown in the first graph of 30 year mortgages shown above, consumers did indeed get yet one more chance to refinance in 2010. But the problem with stagnating real wages surfaced again during the summer slowdown last year:

But then what?

Whether the bottom of the trough of this decline in economic activity is in a few months, or if it is a year or two or more away, the fact remains that, with anemic wage growth to say the least, any incipient recovery ... would be short lived, strangled by the inflation caused by its own increase in demand. If the inflation rate agains exceeds wage growth, consumers will simply cut back again, plunging the economy into another leg down of a "W"-shaped recession.

.... In summary, from here on ... we're not going to see any sustained recovery in the American economy until average Americans see a real and sustained increase in their compensation for labor -- for the first time in over 35 years.

But there is still one more chance ... [i]f long term interest rates do decline again, consumers may yet have one more chance to refinance their spending for the next few years.

.... While if lower mortgage rates persist, there will be space for an economic breather, the paradigm of my 2007 piece remains true. So long as real wages remain stagnant, any recovery which might start will be vulnerable to every uptick in inflation and interest rates, and will be shallow, weak, and probably short-lived. The Great Disinflation of Interest Rates is Ending, the long-term structural problems of our economy have become immediate problems as well, and no long-term recovery is going to take root without real wage growth.

[T]he economic recovery is in a very tight spot -- precisely because average American consumers also remain in a very tight spot. [There has been] wage growth of about 1.5% for the last year. Under those circumstances, even 2% inflation is too much for them to withstand -- without the ability to refinance debt, their disposable income simply isn't keeping up....I have quoted my earlier material at length to show you that this isn't some new theory. I've been writing about it since before the "great recession" and indeed predicted both the beginning and bottom of the recession in large part based on this paradigm. It has proven itself empirically in the real world.

So with paltry income increases of about 1.5%, there are only two ways to sustain the recovery for very long: (1) the inflation rate remains in a very narrow window of 0-1.5%; (2) some asset held widely by average consumers appreciates in value. or (3) another opportunity arises to refinance mortgage debt.

I thik we can all agree that number (2) doesn't look like it's going to happen. That leaves either number (1) or number (3).

....The price of Oil in particular will determine if inflation can remain in the "sweet spot" necessary given low wage growth

.... [O]nly a very narrow window of inflation is helpful to the recovery, and if the unlikely event of decent wage increases doesn't happen, that kind of extremely tame inflation is dependent most of all on energy prices....

This is a very small needle to thread - so the biggest danger to sustaining the recovery.

Aside from the need to prevent repeated energy price shocks throwing the country into recessions, among the most pressing priorities is the need to replace "supply side" economics with "demand side" economics that tilt the scales in favor of real, sustained wage increases for average Americans. Without that, there can be no long-term strong recovery or expansion.