- by New Deal democrat

1. Introduction

By 2008, just about every month Bonddad would write a post entitled "Housing is Nowhere Near Bottom". Eventually, wondering when housing sales if not prices, would hit bottom, I did some research and wrote a few posts back at the blog I used to be at entitled "Housing is Nowhere Near Bottom BUT ..." By early 2009 I concluded that once housing sales broke their trend (which had it continued would have taken new home sales to zero by this year!), that would be a marker of the end of the Great Recession. And so it was, as the series flattened out last spring, and the Great Recession ended last summer.

With the expiration of the $8000 housing tax credit which had stabilized sales and slowed price declines, we have seen a sudden decline in purchase mortgage applications, housing permits and starts. Prices look primed to resume a sharp decline, and there is talk of a double-dip recession as a result. With April and May housing permits plummeting over 100,000, from 681,000 to 576,000, we must wait at least one more month to see if that is the bottom.

At one level, the global Great Recession has been about the bursting of a tremendous housing bubble. So, this seems an appropriate time to step back and take an updated "big picture" look at the state of the housing bust.

2. Housing always leads

Three years ago I wrote about the very significant research paper entitled "Housing and the Business Cycle" (pdf) presented by Prof. Edward Leamer of UCLA at the Federal Reserve's annual summer retreat in Jackson Hole. What follows is a copy of the salient points I made in that post.

2. Housing always leads

Three years ago I wrote about the very significant research paper entitled "Housing and the Business Cycle" (pdf) presented by Prof. Edward Leamer of UCLA at the Federal Reserve's annual summer retreat in Jackson Hole. What follows is a copy of the salient points I made in that post.

Leamer demonstrated that almost every recession since the end of World War II was preceded by a slowdown in housing construction and secondarily in major consumer purchases like cars. According to Leamer, of the 10 recessions that have occurred since World War II:

We have experienced 8 recessions preceded by substantial problems in housing and consumer durables....In terms of timing, housing typically begins to decline 5 quarters before recession, with durables and nondurables hitting their peak 4 quarters before the recession, and gently declining until the recession hits. The only two times since World War II that a substantial housing decline did not presage a recession were in the midst of the Korean War and the Vietnam War.

....

Residential investment consistently and substantially contribute[d] to weakness [in GDP growth] before [ these 8 ] recessions....

....

After residential investment as a contributor to prior weakness come consumer durables, consumer services, and then consumer nondurables. Those are all consumer spending items -- it's weakness in consumer spending that is a symptom of an oncoming recession.... The timing is: homes, durables, nondurables, and services. Housing is the biggest problem in the year before a recession... durables is the biggest problem during the recession [although consumer durables declined even more than housing before 2 of the 10 post World War II recessions]

After a housing slump, the next part of the economy to turn negative before a recession is consumer durables, meaning big-ticket items that consumers purchase to last a long time. The biggest example of that is cars. As Leamer explained:

The same interest rate or other variables [mainly employment] drive both the housing cycle and the durables cycle.... It turns out that much of the ampitude inconsumer durables comes from vehicles not furnitureand he explained why this is so:

Both durable manufacturing and residential construction have four special features:In other words, the economy can only sustain X amount of cars and houses in any given period. Overbuilding in one period (a boom) means that in the next period, there will be underproduction (a bust). It is this absollute decline in activity that forms the basis for the recession.

Previous production of new homes and cars create a stock of existing assets that compete with current production....

The asset prices of both homes and new cars suffer from downward price rigidities

Leamer also pointed out that it appeared that the pattern also fit with the Great Depression. Subsequently I was able to track down the annual statistics kept by the Census Bureau at that time, and in Housing During the Roaring Twenties and Great Depression, confirmed that annual new housing sales did peak in 1925 (at a population-adjusted number very close to the top number in 2005) before declining to a bottom in 1933. No doubt to his everlasting chagrin, Leamer nevertheless predicted in 2007 that the accelarting downturn in housing would be an exception, and would not result in a recession. We know how that turned out!

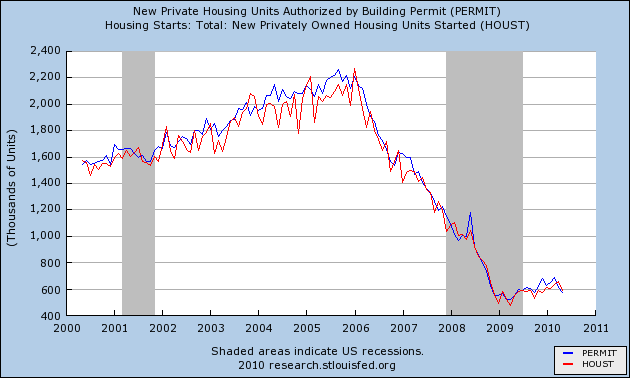

Nevertheless, just as predicted by Leamer's model, housing permits, starts, and sales did bottom before the end of the Great Recession, and increased thereafter -- albeit at a lackluster pace:

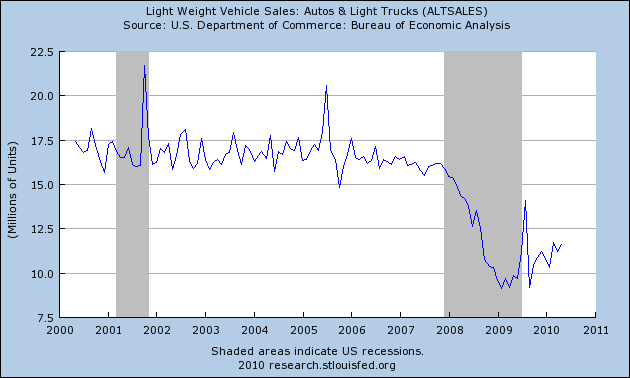

Similarly auto sales bottomed in the first half of 2009, and also increased since then:

The Great Recession was a deflationary bust that was more akin to the old-fashioned panics and deflationary busts last seen in the 1920s and of course the 1930s. Along with Bonddad, I saw signs of a bottom, but at the same time cautioned that there would be No Sustained Economic Growth without Real Wage Growth. The next couple of paragraphs are copied from that post over a year ago.

[In early 2009 I examined] Economic Indicators during the Roaring Twenties and Great Depression. I examined those indicators because our current situation more closely resembles those debt-deflationary downturns, as opposed to post-World War 2 inflationary recessions. That data from the Deflationary period of 1920-1950 showed that all of those deflationary recessions followed a pattern. The CPI declined from the beginning of the recession and its YoY rate of decline bottomed immediately before the recession's end. M1 money supply followed a similar pattern, sometimes coincidentally, sometimes leading slightly. In all 6 of those deflationary recessions, once M1 and CPI began to decline at a decreasing rate, the recession was about to end.

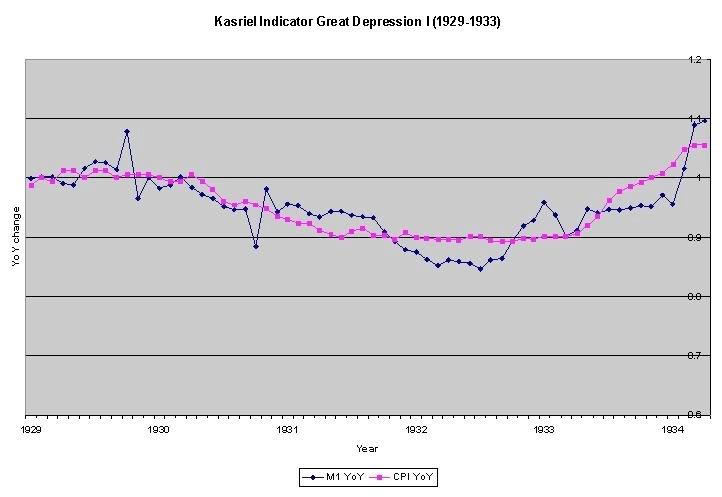

For example, looking at the Great Depression of 1929-32:

we see that in this, the biggest of all economic contractions of the last century, like all other deflationary recessions, there was a clear pattern of M1 and CPI on the graphs --both money supply and inflation contracted at an increasing rate, then at a constant rate, before simultaneously or with M1 leading the way before CPI, both turn back up (meaning, prices and money supply are still declining, but at a decreasing rate) near the end of the deflationary recession. In other words, these deflationary recessions began to end once demand picked up. As demand picked up (recall Econ 101) inflation reappeared.

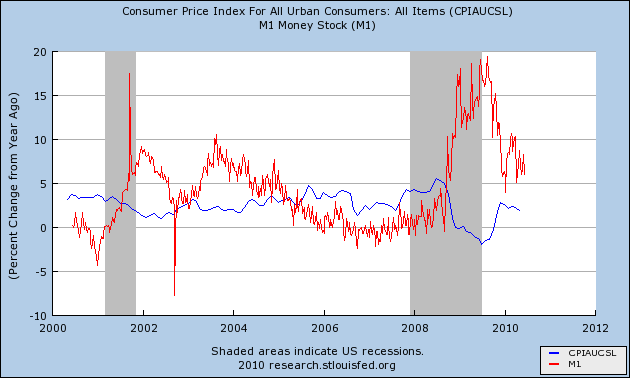

Finally, just as had happened in the aftermath of the old deflationary busts, inflation did reappear in the second part of 2009 and into the beginning of this year, as improving consumer demand, and with it higher energy prices, firmed up prices (CPI in blue, M1 in red):

3. New and Existing Home Sales

In the last few months, there has been another deflationary pulse, driven by steep declines in commodity prices, especially gasoline, and by the very slow decline in "owner's equivalent rent" (which is the controversial way in which the BLS measures housing prices). Coincidentally, because of the expiration of the $8000 housing credit, housing permits and starts, and home sales, have fallen again. Although we cannot say for sure that May marked the end of that decline, it does appear that new home sales will not fall all the way back to the early 2009 bottom. But a large and sustained decline is nevertheless a cause for concern.

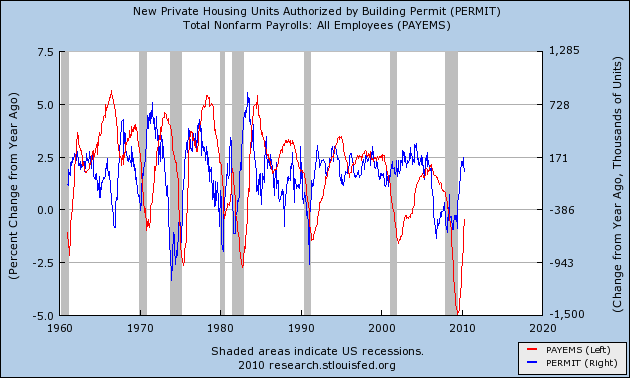

Housing is a "long" leading indicator for the economy in general, and jobs and unemployment in particular (as opposed to a "short" leading indicator like real M1. Here is a graph of the year-over-year increase or decrease in housing starts vs. year over year percent increase or decrease in jobs over the last 50 years. Notice that the peaks and troughs for housing construction (blue) generally occur well in advance of the growth and decline in jobs (red):

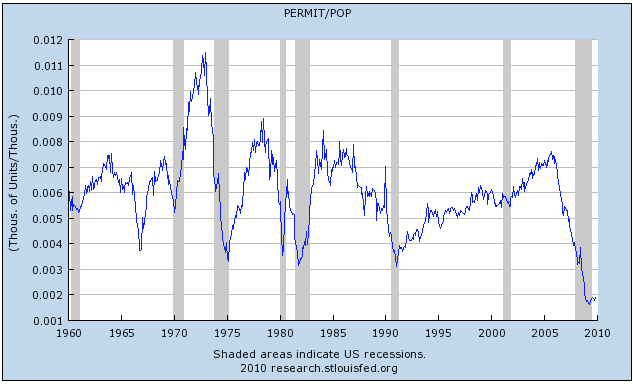

Eventually, however, housing will return to its long term norm. Here is a graph I ran a few months ago, showing housing starts as a fraction of population:

On a per capita basis, the housing boom of a few years ago doesn't look that outlandish at all! In fact, at least 3 prior booms in the last 40 years were bigger. On the negative side, the current housing bust is even more clearly the worst in the post WW2 era. For the last couple of years, housing starts have come nowhere near where they need to be to keep even with population growth. At some point, prices will fall enough and there will be enough pent-up demand, that the housing bust will end.

In the last few months, there has been another deflationary pulse, driven by steep declines in commodity prices, especially gasoline, and by the very slow decline in "owner's equivalent rent" (which is the controversial way in which the BLS measures housing prices). Coincidentally, because of the expiration of the $8000 housing credit, housing permits and starts, and home sales, have fallen again. Although we cannot say for sure that May marked the end of that decline, it does appear that new home sales will not fall all the way back to the early 2009 bottom. But a large and sustained decline is nevertheless a cause for concern.

Housing is a "long" leading indicator for the economy in general, and jobs and unemployment in particular (as opposed to a "short" leading indicator like real M1. Here is a graph of the year-over-year increase or decrease in housing starts vs. year over year percent increase or decrease in jobs over the last 50 years. Notice that the peaks and troughs for housing construction (blue) generally occur well in advance of the growth and decline in jobs (red):

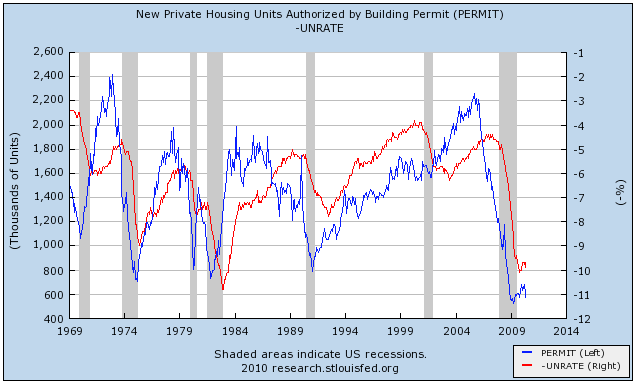

The same can be seen in the following graph of the number of housing starts (blue) and the unemployment rate (inverted, so lower values mean a higher percent of unemployed)(red):

Thus the housing component of the recent improvements to the economy have been very weak, correlating with a persistently high unemployment rate and a sub-par recovery in jobs (500,000 non-census jobs added since the bottom last December).

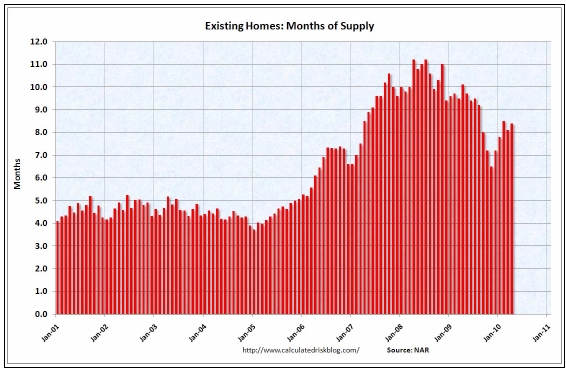

The bottom line is, for there to be a sustained and strong Recovery, we would need sustained and strong growth in housing construction. BUT, there will not be a sustained and strong rebound in housing construction so long as there are many 100,000s of houses for sale or in foreclosure, hanging over the market. One benchmark is that this overhang will not revert to norm until there is no more than 6 months of inventory on the market. As of the last few month, there was more than 8, as depicted in this graph:

The bottom line is, for there to be a sustained and strong Recovery, we would need sustained and strong growth in housing construction. BUT, there will not be a sustained and strong rebound in housing construction so long as there are many 100,000s of houses for sale or in foreclosure, hanging over the market. One benchmark is that this overhang will not revert to norm until there is no more than 6 months of inventory on the market. As of the last few month, there was more than 8, as depicted in this graph:

(h/t Calculated Risk). So long as this overhang persists, it is going to suppress residential construction, and so jobs and the economy. So the question becomes, when do housing prices become low enough so that demand increases to the point where the overhang of vacant or foreclosed houses dissipates?

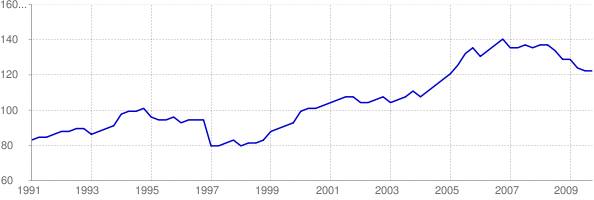

4. House Prices

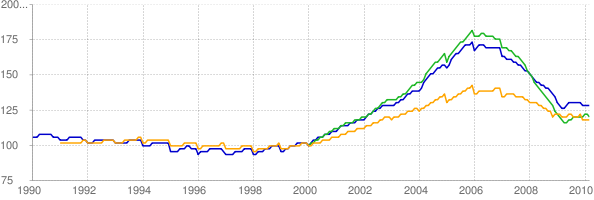

Here is where the continuing data from Housing Tracker, the web site that was so instrumental 4 and 5 years ago in showing the turn of the housing market, is so essential. The following graph, from that site, shows the relationship between median household income and housing prices, normed to 100 in the year 2000. The three lines make use of the Case-Schiller, FHFA, and First American Indexes:

4. House Prices

Here is where the continuing data from Housing Tracker, the web site that was so instrumental 4 and 5 years ago in showing the turn of the housing market, is so essential. The following graph, from that site, shows the relationship between median household income and housing prices, normed to 100 in the year 2000. The three lines make use of the Case-Schiller, FHFA, and First American Indexes:

The simple fact is, even after 4 years of a bursting bubble, housing prices are still expensive, compared with their long-term norm. As you can see from the above graph, by no measurehave house prices returned to their long term norm. They are still about 20% higher in real terms compared with the income of the people who must after all buy them, than they were 10 years ago. And there is no guarantee they won't overshoot the mark. Notice also that they generally went sideways in 2009 as people took advantage of the $8000 home buying tax credit. With that credit gone, the slide in house prices is resuming. If prices decline at the same rate, compared with median income, as they did between 2006-2008, it will probably take at least 2 more years for prices to revert to their long term norm, and approach a bottom.

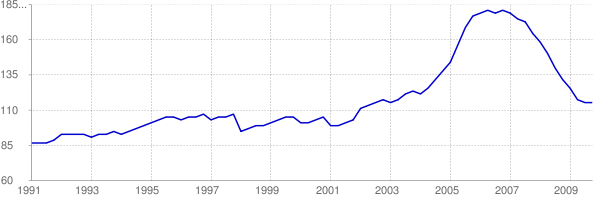

Variances is metropolitan areas help show us the relationship between prices and clearing out the overhang of houses on the market from the bubble. On the one hand, prices in Seattle Washington peaked late -- about 2008, and have not declined nearly as much as the norm, in terms of income, as the national average:

Variances is metropolitan areas help show us the relationship between prices and clearing out the overhang of houses on the market from the bubble. On the one hand, prices in Seattle Washington peaked late -- about 2008, and have not declined nearly as much as the norm, in terms of income, as the national average:

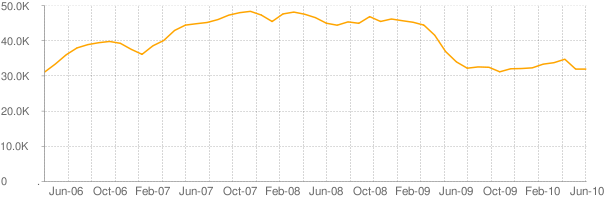

As a result, the number of houses for sale in the area has continued to increase up to the present. There is still a huge overhand, and so we can expect a lot of further declines in home prices in Seattle:

On the other hand, prices in Phoenix Arizona, one of the epicenteres of the housing bubble, peaked early, and prices as a multiple of median income have declined almost all the the way to their prior norm in 2000:

As a result, the number of houses for sale has declined dramatically, and prices may stabilize very soon if they aren't doing so already:

Eventually, however, housing will return to its long term norm. Here is a graph I ran a few months ago, showing housing starts as a fraction of population:

On a per capita basis, the housing boom of a few years ago doesn't look that outlandish at all! In fact, at least 3 prior booms in the last 40 years were bigger. On the negative side, the current housing bust is even more clearly the worst in the post WW2 era. For the last couple of years, housing starts have come nowhere near where they need to be to keep even with population growth. At some point, prices will fall enough and there will be enough pent-up demand, that the housing bust will end.

In Conclusion

When will that happen? House Prices must - and will - fall at least another 15%-20% to revert to their long term norm as a multiple of wages. Simply put, the more the prices of housing decline, the more existing homes will be bought, and the sooner the backlog of unsold homes will be absorbed. Then and only then can we expect a substantial and sustained improvement in housing construction, and thereby a substantial and sustained improvement in the economy. Based on the above, that date appears to be at least 2 years away.